Happy new year all! New year, new banner, courtesy of my brilliant daughter who presented me with a plausible 3-D model of my very primitive cartoon of a reverse-centaur over Christmas. And I thought I would kick off with a relatively uncontentious subject: examinations!

“Back to normal!” That was the cry throughout education when the pandemic had finally ended enough for us to start cramming students into rooms again. The universities had all leveraged themselves to the maximum, and perhaps beyond, to add to the built estate, so as to entice students in both the overseas and the uncapped domestic market to their campuses, and one by-product of this was they had plenty of potential examination halls. So let’s get away from all of that electronic remote nonsense and get everyone in a room together where you can keep an eye on them and stop them cheating. This united the purists who yearned for the days of 10% of the cohort turning up for elite education via chalk and talk rather than the 50% we have today, senior management needing to justify the size of the built estate and politicians who kept referring to traditional exams in an exam hall as the “gold standard”.

So, in a time when students have access to information, tools, how to videos of everything imaginable, the entire output of the greatest minds of thousands of years of human history, as well as many of the less than great minds, in short anything which has ever caught anyone’s attention and been committed to some form of media: in this of all times, we want to sort the students into categories for the existing job market based on how they answer academic questions about what they can remember unaided about the content of their lecture courses and reading lists with a biro on a pad of paper perched precariously on a tiny wooden table surrounded by hundreds of other similar scribblers, for a set period of time as minders wander the floors like Victorian factory owners.

And for institutions that thought the technology we fast-tracked for education delivery and assessment in the pandemic would surely be part of education’s future? Or perhaps they just can’t afford to borrow half a billion or have the the land available to construct more cathedrals of glass and brick to house more examination halls? Simple! We just create the conditions for that gold standard examination right there in the student’s own bedroom or the company they work for!

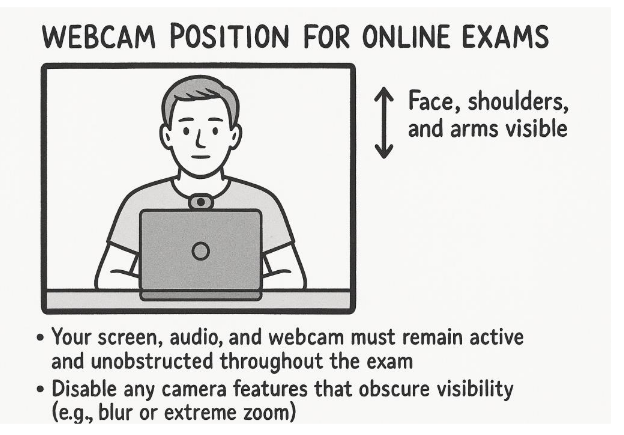

There are 54 pages to the Institute and Faculty of Actuaries’ (IFoA’s) guidance for remotely invigilated candidates. It covers everything from the minimum specification of equipment you need, including the video camera to watch your every movement and the microphone to pick up every sound you make, to the proprietary spying software (called “Guardian Browser”) you will need to download onto your own computer, how to prove who you are to the system, what you are allowed to have in your bedroom with you and even how you need to sit for the duration of the exam (with a maximum of two 5 minute breaks) to ensure the system has sufficient visibility of you at all times:

These closed book remote arrangements replaced the previous open book online exams which most institutions operated during the pandemic. The reason given was that the exam results shot up so much that widespread cheating was suspected and the integrity of the qualifications was at risk. The IFoA’s latest assessment regulations can be found here.

The belief in examinations is very widespread. A couple of months ago I was discussing the teacher assessments which replaced them briefly during the pandemic with a secondary business studies teacher. He took great pride in the fact that he based his assessments solely on mock results, ie an assessment carried out before all of the syllabus had been covered and when students were unaware it would be the final assessment. But still in his mind more “objective” than any opinion he might have of his own students.

If a large language model can perform enormously better in an examination than your students can without it, what it actually demonstrates is that the traditional examination is woefully unprepared for the future. As Carlo Iacono puts it:

The machines learned from us.

They learned what we actually valued and it turned out to be different from what we said we valued.

We said we valued originality. We rewarded conformity to genre. We said we valued depth. We measured surface features. We said we valued critical thinking. We gave higher marks to confident assertion than to honest uncertainty.

So now the machines produce what the world trained them to produce: fluent, confident, passable output that fits the shapes we reward.

And we’re horrified. Not because they stole something from us. Because they showed us what the systems were selecting for all along.

The scandal isn’t that a model can imitate student writing. The scandal is that we built an educational and professional culture where imitation passes as competence, and then acted shocked when a machine learned to imitate faster.

We trained the incentives. We trained the rubrics. We trained the career ladders.

The pattern recognition which gets you through most formal examinations is just too cheap and easy to automate now. It is no longer a useful skill, even by proxy. It might as well be Hogwarts’ sorting hat for all the use it is in a post scarcity education world. If the machines have worked out how to unlock the elaborate captcha system we have placed around our gold standard assessments, an arms race of security measures protecting a range of tests which look increasingly narrow compared to the capabilities which matter does not seem like the way to go.

What instead we are doing is identifying which students are prepared to put themselves through literally anything to get the qualification. Companies like students like that. They will make ideal reverse-centaurs. The description of life as a reverse-centaur even sounds like the experience of a proctored exam:

Like an Amazon delivery driver, who sits in a cabin surrounded by AI cameras, that monitor the driver’s eyes and take points off if the driver looks in a proscribed direction, and monitors the driver’s mouth because singing isn’t allowed on the job, and rats the driver out to the boss if they don’t make quota.

The driver is in that van because the van can’t drive itself and can’t get a parcel from the curb to your porch. The driver is a peripheral for a van, and the van drives the driver, at superhuman speed, demanding superhuman endurance. But the driver is human, so the van doesn’t just use the driver. The van uses the driver up.

Source: Cory Doctorow, Enshittification

And, even if you are OK with all of that, all of these privacy intrusions don’t even work to prevent cheating! The ACCA, the world’s largest accounting professional body, has just announced it is stopping all remote exams after giving up the arms race against the cheats, facilitated in some cases seemingly by their Big Four employers lying about what had gone on.

Actuarial exams started in 1850, only 2 years after the Institute of Actuaries was established (Dermot Grenham wrote about them recently here). This pre-dated the establishment of the first examination boards by a few years (1856 Society of Arts, the Society for the encouragement of Arts, Manufactures and Commerce, later the Royal Society for the encouragement of Arts, Manufactures and Commerce (Royal Society of Arts); 1857: University of Oxford Delegacy of Local Examinations (founded by the University of Oxford); and 1858: University of Cambridge Local Examinations Syndicate (UCLES, founded by the University of Cambridge)), so keen were actuaries to institute examinations. However it was the massive expansion of the middle classes as the Industrial Revolution disrupted society in so many ways that led to the need for a new sorting hat beyond the capacity of the oral examinations that had previously been the norm.

Now people seem to be lining up to drag everyone back into the examination hall. Any suggestion of a retreat from traditional exams is met by howls of outrage from people like Sam Leith at The Spectator about lack of “rigour”. However, in my view, they are wrong.

Yes of course you can isolate students from every intellectual aid they would normally use, as a centaur, to augment their performance, limit the sources they can access, force them to rely on their own memories entirely, and put them under significant time pressure. You will definitely reduce marks by doing that. So that has made it harder and therefore more rigorous and more objective, right?

Well according to the Merriam-Webster dictionary, rigorous is a synonym of rigid, strict or stringent. However, while all these words mean extremely severe or stern, rigorous implies the imposition of hardship and difficulty. So promoting exams above all as an exercise in rigour reveals their true nature as a kind of punishment beating in written form, for which the prize for undergoing it is whatever it qualifies you for. Suddenly the sorting hat looks relatively less arbitrary.

The problems of traditional exams are well known, but the most important ones in my view are that they measure a limited range of abilities and therefore are unlikely to show what students can really achieve. Harder does not mean more objective. It is like deciding who can act by throwing students out, one at a time, in front of a baying mob of, let’s say for argument, readers of The Spectator. Sure, some of the students might be able to calm the crowd, some may even be able to redirect their anger towards a different target. But are the people who can play Mark Antony for real necessarily the best all-round actors? And has someone who can only stand frozen on the spot under those circumstances really proved that they could never act well?

It also means that education ends a month or more before the exams, to allow the appropriate cramming, followed by engaging all of the teaching staff in the extended exercise of marking, checking and moderating what has been written in answer to academic questions about what the students can remember unaided about the content of their lecture courses and reading lists with a biro on a pad of paper perched precariously on a tiny wooden table surrounded by hundreds of other similar scribblers, for a set period of time as minders wander the floors like Victorian factory owners. But what if instead the assessment was part of the teaching process? What if students felt that their assessment had been a meaningful part of their educational experience? What if, instead of arguing the toss over whether they scored 68% or 70% on an assessment, students could see for themselves whether they had demonstrated mastery of their subject.

One model of assessment which is getting a lot of attention at the moment, one I am a big fan of having used it at the University of Leicester on some modules, is something called interactive oral assessment, where students meet with a lecturer or tutor, individually or in a small group, and answer questions about work they have already submitted. It is a highly demanding form of assessment, for both the students and the assessors, but it means the final assessment is done with the student present and, with careful probing from the assessors, who will obviously need to have done a close reading of the project work beforehand, you can be highly confident of the degree to which the student understands the work they have submitted. It also allows the student to submit a piece of work of more complexity and ambition than can be accommodated by a traditional exam. And it needn’t take any more time if the interviews are carried out online when set against the exam marking time of the traditional exam. Something which all the technology we developed through the pandemic allows us to do, without the need for spyware.

There are other models which also assess the technological centaurs we wish our students to become rather than the reverse-centaurs we are currently dooming too many to become. It is looking like it may be time to start telling students to stop writing and to put down their pens on the traditional exam. And perhaps the actuarial profession, who led us into the era of professional written examinations so enthusiastically 175 years ago, might now want to take the lead in navigating our way out of them?