My favourite bit of Scrooged is when Bill Murray is told that the people working in a homeless shelter cannot be fired because they are volunteers. It appears that the Institute and Faculty of Actuaries (IFoA) is instead in danger of morphing into such a sleek, streamlined, efficient, simplified and clarified organisation that noone would want to volunteer for it any more.

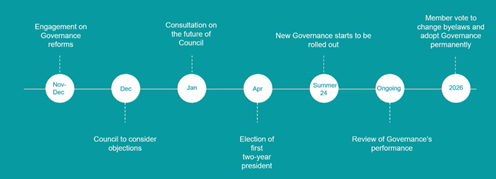

The long-running argument about the future governance of the IFoA grinds on. Four months after a small number of members alerted the rest of us to what was going on, and 194 members then objected in writing, the IFoA have now concluded a series of webinars explaining the proposals. I attended the final one on 28 November.

In a nutshell, the proposals are unchanged from those objected to, they are now being considered alongside the objections by the newly elected Council this month, which will be followed by a full consultation in January. The new governance structure will then be rolled out in the summer of 2024 and a member vote only allowed on the new structure two years later in 2026. Yes that’s right, not a typo: 2026!

The session I attended was all about how we needed to be more streamlined, more efficient, more credible in our governance. We needed to simplify our governance, clarify it. The recent embarrassments about outgoing CEOs was cited as an example of our poor governance without explanation. The independent report which they quoted from throughout to justify the proposals will not be provided to members as it includes contributions from people who only did so on the basis of anonymity.

There was a discussion about how the IFoA was both a business and a member organisation. But, in mentioning more than once how the proposals were only what any of the organisations members worked for would expect from their governance, the weighting given to these two roles was very clear. These were senior business leaders attempting to make the IFoA look more like the businesses they are more used to.

If you’re a senior business leader, then an organisation where any member can have some influence on its direction of travel must be incomprehensible. They are used to leading and being followed. Much was made of the waste of time that much Council business involved, and I am sure that is right. But that is just a motivation for change, as indeed was the entire presentation on 28 November. It was decidedly not a motivation for this change in particular.

We were told that other options had been considered, although bundling everything up into one board that did everything was the only one mentioned.

One of the other reasons given for the changes proposed was how much bigger the IFoA was now. Coincidentally, on 27 November, the Economic Affairs Committee of the House of Lords published its report ‘Making an independent Bank of England work better’. In it they made the following point:

The growth in the Bank’s remit has not been met with a commensurate increase in accountability and Parliamentary scrutiny. While an independent central bank reassures markets, critically important economic decisions are delegated to unelected officials. The Committee is concerned that a democratic deficit has emerged, which risks undermining confidence in the Bank and its operational independence.

We are being asked to quietly acquiesce to the creation of precisely this kind of democratic deficit in our own member organisation. Because, despite suggestions to the contrary in the webinar, we are primarily a member organisation and not like the organisations we all work for, something we have just been reminded of by being charged £750 for the privilege.

If we agree to this timetable, then by the time we get to 2026 I predict we will be assured that it would not be cost effective or a good use of the new unitary board’s time to uproot what will by then be the incumbent system. This would be giving these proposals an unfair advantage in deciding on the long-term governance of the IFoA.

My requests would be:

Some summarised form of the independent report which protects people’s anonymity but allows us members to judge for ourselves the relative strengths and weaknesses of the analysis of our current governance and the options so far considered for change.

An opportunity for a member vote on the structure adopted in 2024 alongside the consultation, rather than 2 years post adoption.

It is precisely at the stage of deciding that structure that all of the range of experience, talent and wisdom of the membership needs to be deployed, not at the point of rubber stamping a decision already made. If you agree with me that members are being sidelined in the decision-making process about the very nature of the IFoA’s future, then please send your feedback to governance@actuaries.org.uk.

In my previous post, I talked about out how dependent the bottom half of the income scale was on the state pension of £10,600 pa, and how an increase of at least 40% to the state pension was needed to reset the balance between a guaranteed income and that based on the markets to European levels.

However there was another aspect of the state pension which I did not mention last time and which also needs to be addressed.

Who gets it?

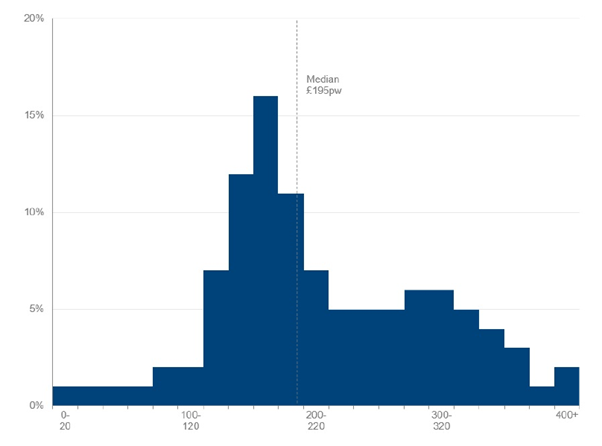

Source: ONS – Almost all pensioners (97%) received income from State Pension, with an average amount of £195 per week. Some peaks in the distribution may be explained by the basic State Pension rate, which was £137.50 per week in FYE 2022, as well as the new State Pension full rate, which was £179.60.

As the graph above shows, by no means does everyone get the full state pension (although legacy state benefits mean that some get considerably more).

To qualify for this full state pension, an individual needs to have made 35 years of National Insurance contributions or have equivalent credits. To qualify for any fraction of the state pension, an individual must have made at least ten years of contributions or have equivalent credits. Thus, even the UK’s first pillar, the state pension, is to a degree contribution based. This stands in contrast with countries such as Canada, Mexico, the Netherlands and New Zealand, which have adopted a residence-based, non-contributory basic pension. Residency-based pensions increase coverage and seem to be effective in reducing poverty rates in old age.

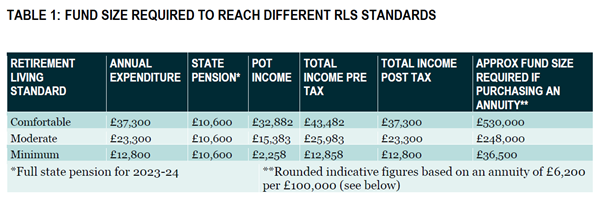

Source: PLSA – these are single retirement living standards outside London

You will note that the retirement living standards assume:

income tax is payable;

people are mortgage and rent free; and

it also does not cover care costs.

The minimum level would then require a 21% uplift to the basic state pension, assuming no meaningful private or occupational pension assets (which we saw last time was a reasonable assumption for most of the bottom half of the income scale).

According to the Government’s figures, in 2020-21, 5% of all older households (ie where the household “reference” person was 65 or older) were mortgagors, 6% were private renters and 15% were social renters (down from 19% in 2010-2011). The remaining 75% of older households were outright owners (up from 71%). So we are going to need more for our minimum level to meet the needs of the 25% who are still paying rent or mortgages. The average household income spent on rent amongst older renters is 38% for private renters and 27% for social renters.

Assuming this household income is the basic state pension and the average housing costs of the group we are concerned about (ie totally or almost totally dependent upon the state pension) are in line with social housing rent, we would need an additional 37% uplift to the state pension (to mean that taking 27% of it would get you back to where you started) to 66% of state pension, ie a total of £17,600 pa before the latest state pension increase. If you are aiming for the moderate retirement living standard you would need over twice as big an overall state pension at £35,600 pa.

Means-tested benefits

At this point, if you are shouting at your phone or computer “but you are ignoring means-tested benefits!” you would be correct. Age UK give a handy guide to means tested benefits, but in a nutshell we have:

Cold Weather Payment – £25 a week for each 7-day period of cold weather. This only applies between 1 November and 31 March each year.

Council Tax Support – there is no set amount of Council Tax Support. What you get depends on your circumstances and where you live. Each local council is responsible for operating its own Council Tax Support scheme so the amounts of support given across the country may vary.

Housing Benefit – Housing Benefit is money to help you cover your rent if you’re living on a low income.

Income Support – this is going to be fully replaced by universal credit by the end of 2024. Universal Credit has come in for a lot of criticism – this is the Trussell Trust’s take on it.

Pension Credit – the bit of this that we are interested in is the Guarantee Credit, which tops up your weekly income to a guaranteed minimum level. In 2023-24, this level is: £201.05 if you’re single and £306.85 if you’re a couple (note that these are still below the levels of the basic state pension).

Universal Credit – for a single person over 25 this is currently £368.74 per month but there are many circumstances which can lead to deductions to this amount and the Trussell Trust (see above) has this to say about it:

These are at the lowest levels in 30 years and aren’t protecting people from destitution, meaning they are unable to afford the essentials we all need to eat, stay warm and dry and keep clean.

The trouble with means-tested benefits are:

Not everyone claims them. An FT article from April 2022 claimed that there were £15 billion of unclaimed means-tested benefits – for a variety of reasons, but with lack of internet access (18% of older households) being a major one. This compares with £5 billion currently spent on Pension Credit and £6 billion spent on Housing Benefit for over 65s, so you can see the size of the problem here;

They create, in some cases, high effective marginal tax rates for people who want to earn a little extra income, by removing benefit as income increases;

If a benefit is not universal, there is a danger that the recipients will become so marginalised that their voice is no longer strong enough to defend it, and people might not feel like full citizens of the society they live in. Applying for benefits requires admitting poverty which can be humiliating;

Means-tested benefits are often poorly targeted. The Report of the UN’s Special Rapporteur from 2019 on extreme poverty and human rights, whose recent comments gave me the title for this post, included the following amongst its 11 recommendations: Initiate an independent review of the efficacy of changes to welfare conditionality and sanctions introduced since 2012 by the Department of Work and Pensions;

There are good reasons for people not to want to claim means tested benefits, as the UN report says: The basic message, delivered in the language of managerial efficiency and automation, is that almost any alternative will be more tolerable than seeking to obtain government benefits.

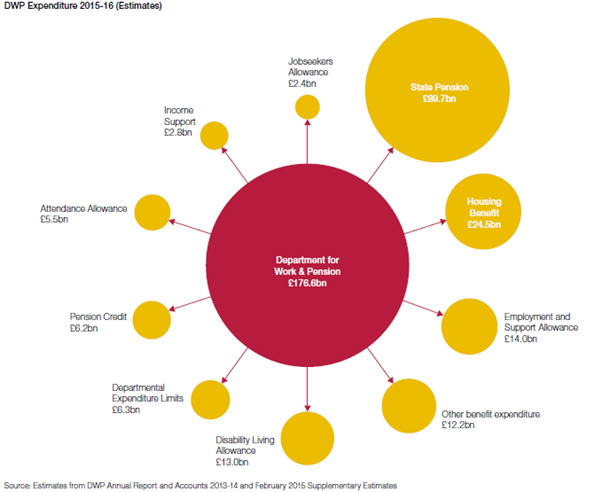

Means-tested benefits cost a lot to administer. The latest National Audit Office guide to the Department of Work and Pensions (DWP) for instance (from 2015-16) indicates the following split:

Of a total budget of £176.6 billion, departmental expenditure in addition to benefit expenditure was £6.3 billion. Attempts to reduce this figure since 2016 appear to have resulted in big increases to under and over payments. Simon Duffy of Citizen Network, who has looked at this extensively and attempted to compare the net benefit to recipients to the total administrative costs including those of the tax system, estimates that, to make people £1 better off, the DWP spends £0.22.

It therefore seems to me that, in order to provide a guaranteed minimum level of living standards in retirement, not dependent upon pensioners being invested in the right way, or filling in the right forms or their employment history, and not vulnerable to the punitive sanctions currently applied to conditional benefits like Universal Credit, we are going to need a state pension somewhere north of 66% above its current level. So how do we pay for it?

How do we pay for it?

My very rough estimate of the amount required to top up everyone below the full state pension in the graph at the top of this post is around an additional 23%.

The current state pension cost around £110 billion pa in 2022-23 or 4.4% of GDP. Allowing for the Pension Credit, Housing Credit and Winter Fuel Allowance at half their current levels following the increase to state pension proposed (a very conservative estimate I believe, which also does not include the smaller increase that those on legacy benefits will need) brings it up to 4.75% of GDP. So what I am proposing would cost up to an additional £73 billion pa in state pension or an additional 2.9% of GDP, or a total of 7.65% of GDP plus the 23% uplift required to top everyone up to the full state pension bringing it to 9.4%, which would put us above the current OECD average of 8% of GDP, although still less than is currently paid by Italy, Greece, France, Austria, Portugal, Finland, Spain, Poland, Belgium, Slovenia and Germany. It is therefore something that we can afford to do in the world’s 5th largest economy if we make this a priority.

These additional payments of around £125 billion would result in immediate increased income tax payments (assuming all at the 20% rate) of £25 billion plus the ONS estimate between 18% and 28% of the poorest 40% of households’ income is spent on indirect taxation, averaging 23% or £29 billion. However, as Richard Murphy has pointed out, there is currently a risk that millions of pensioners will have to complete tax returns (in many cases for the first time) next year due to the triple lock bringing pension levels above the frozen personal allowance. HMRC will therefore need to be reformed so as to be able to collect tax on pensions via PAYE and allow pensioners to receive net pensions in future.

My view is that raising the guaranteed state pension to a level which will be sufficient post tax is preferable to just lifting the personal allowance above the new state pension level. Why? Because:

Everyone would get the new personal allowance, reducing taxation of the wealthiest as well as the poorest, with no particular benefit to the poorest; and

One of my problems with means tested benefits is that they marginalise people so that they do not feel like full members of society. The same applies to not paying tax. If you pay tax, you are more likely to want a say in how that society is organised.

Some options for funding more than the remaining balance of £71 billion, picked out from Richard Murphy’s very conservative estimates here, are as follows:

Ending higher rates of tax relief on pension contributions. This would raise £14.5 billion in tax a year;

Abolishing the VAT exemption for financial services within the UK might raise £8.7 billion of additional tax revenue pa;

Reforming national insurance charges on higher levels of earned income in the UK might raise an additional £12.5 billion of tax revenue pa;

Aligning capital gains tax and income tax rates in the UK might raise more than £12 billion in additional tax a year;

Reforming the administration of corporation tax in the UK might raise at least £6 billion of tax a year;

Abolishing the inheritance tax exemption on some funds retained in pension arrangements at the time of a person’s death might raise £1.3 billion a year;

Reforming inheritance tax business property relief might raise £3.2 billion of tax a year;

Reforming inheritance tax agricultural property relief might raise £1.0 billion of tax a year;

Reforming Companies House might raise £6 billion of tax a year;

Reintroducing close company rules for income and corporation tax could raise at least £3 billion of tax a year; and

Abolishing the domicile rule for tax purposes might raise £3.2 billion of tax revenue a year.

I am sure you would have your own list. And you may not agree with the size of guaranteed state pension increase I have suggested. And I fully admit that these are very approximate figures made to illustrate what might be possible. However I hope I have made a reasonable case for what would be required as a guaranteed income for all pensioners if it were a political priority.

Next month, I will be attempting to tackle the question of why it should be a priority or, in other words, what would be gained by increasing the state pension for all?