The latest publication from the Institute and Faculty of Actuaries (IFoA) is called Beyond the next Parliament: The case for long-term policymaking. It refers to a number of previous reports, such as the Great Risk Transfer report from April 2021 and the two more recent climate papers (here and here), all of which contained much thoughtful analysis even if I did not always agree with all of the recommendations.

The case for long-term policymaking is certainly something that needs to be made loudly and often, although I was perhaps expecting some discussion of concepts like cathedral thinking, ie a capacity to plan and implement projects over multiple generations, or intergenerational justice, an issue of particular importance when discussing responses to climate change, in tying these various reports together within a long-term narrative. The Good Ancestor by Roman Krzanic is a great starting point for considering such questions.

Instead the IFoA have chosen to go in a different direction entirely in linking this previous work together, displaying imprisonment by current short-term political thinking in a paper supposedly focused on the long-term to such an extent that I am now left feeling that I disagree with them about nearly everything.

Take pensions, for instance (bold type is mine):

With the decline of defined benefit (DB) pension schemes, the responsibility for investment and longevity risk is increasingly being placed on the individual.

In a world where responsibility for funding retirement is increasingly being placed on the individual, there is remarkably little consistent consumer information about how much someone should save into their pension, or what a ‘good’ pension pot constitutes.

The IFoA remains concerned that many UK households are not saving enough for later life, are not accessing free guidance or paid-for financial advice, and remain ill-equipped to deal with the risk of running out of money in retirement.

It is almost as if the transfer of risk to individuals is something inevitable, or beyond the ability of mere humans to control. In the words of the late great John Sullivan, in the theme song from Only Fools and Horses:

Cause where it all comes from is a mystery. It’s like the changing of the seasons and the tides of the sea.

Why Only Fools and Horses you ask? Well have you ever heard a better description of defined contribution pensions than:

No income tax, no VAT. No money back, no guarantee

The IFoA’s main concern is that UK households are not doing enough about this new “responsibility” to provide for their own retirement. And the state? The state pension is mentioned only once here:

Naturally, the next UK Government will need to address the adequacy question as part of a wider pensions strategy for the UK that also considers big questions such as the sustainability of the State Pension and the triple lock.

This of course is so-called “positive economics” in action, which makes much of only relying on objective data analysis, but within a policy framework which is not up for discussion. Increased state provision, which one would have thought would at least need to be considered in the mix in this case, is reduced to obsessive focus on tiny questions like the triple lock while being kept generally outside this policy framework. Instead we get this:

We recommend that the government should reinvigorate its public messaging around minimum pension saving levels – particularly through workplace auto-enrolment pension schemes – to ensure that consumers are not lulled into a false sense of security as to whether their pension saving will be adequate to achieve their retirement income goals.

In doing so, government should use expertise and evidence on testing behavioural responses to different messages and channels, to identify those that are most effective in impacting saving behaviour.

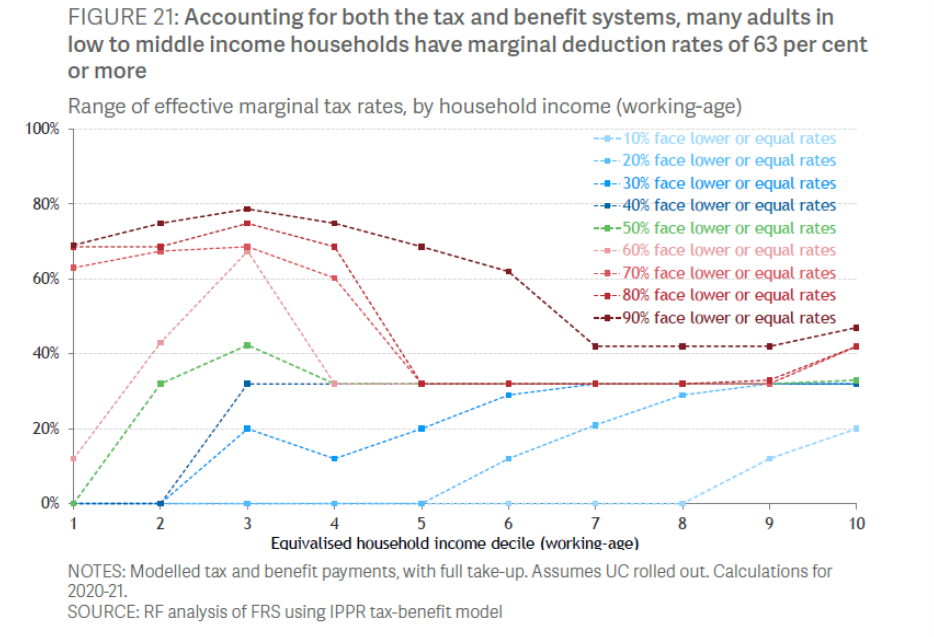

So at a time when, according to the Resolution Foundation, the marginal rate for low to middle income households have an effective marginal rate of tax of 63%, the IFoA apparently think it is acceptable to push the cost onto them even more in order to achieve a sufficient pension at retirement. A certain cost and uncertain benefit. It is not a basis for a minimum income guarantee.

The second section sets out the problems associated with long-term care, again asking for a greater contribution by individuals via an expansion of insurance and savings-based financial products.

We are back to the changing of the seasons and the tides of the sea in the next section on keeping pace with rapid digital transformation, which states that:

there has been a trend away from broad risk pools and toward more granular pricing based on an individual’s specific rating factors (i.e. their risk characteristics)

Note the use of the passive tense there – it implies that noone is responsible and there is no way we can swim against this current back up to those old broad risk pools however hard we try. And so we shouldn’t try. The only option is to instead try and lower the premiums at the bottom end a bit – which is explained in their other report, The hidden risks of being poor: the poverty premium in insurance. The model for this is Flood Re, which is explained here. Of course this probably won’t work if you are underinsured as, it seems, 80% of us are.

Section 3 remains one I can cheer about, laying out more clearly than I have seen before to the financial community the risks of climate change, with the work on biodiversity at a somewhat earlier stage. However a framework is immediately assembled in the next section, Going for growth to build a better Britain (a slogan which I am sure Liz Truss would have been quite happy with), to limit the options for tackling these risks. An example:

Even though there is evidence that infrastructure development can promote growth and job creation, governments may be forced to defer such funding until the national balance sheet looks healthier. Although governments may be partially able to finance infrastructure projects, given their capital constraints they also need to attract investment from the private sector.

Unbelievably, the rest of this section then focuses almost entirely on what can be done to lure the private sector into investing in preventing their own doom (not framed in those terms of course, but in terms of boosting growth rather than curbing emissions) along with everybody else’s. As long as private investors are looked after, everything else seems to be a secondary consideration. John Sullivan again:

C’est magnifique, Hooky Street.

Of course I am just having a bit of fun here with the Only Fools and Horses references and I am certainly not suggesting that everyone involved in financial markets is a Del Boy looking to take advantage of every punter or government that comes their way. That would be a caricature as gross as referring to the “dead hand of the state” or talking about public servants as “The Blob”. What I am saying is that the jostle of the market place cannot be the primary solution to many of the problems so accurately analysed here.

I realise I have been very slow to fully appreciate the IFoA’s general direction of travel, but by putting all of these reports together in one place they have clarified this for me. I believe that the overall programme of recommendations here would condemn the poor to further immiseration and uncertainty while letting government largely off the hook for solutions and companies largely off the hook in terms of further regulation. It would further accelerate the financialisation of our economy with the promise of additional financial markets to be exploited by the already wealthy.

This is not acting in the public interest but as a cheerleader for protecting the long-term profits of fund managers. And I despair that, three years on from the IFoA’s Economics Member Interest Group coming into existence, there should still be so little pluralism on display here in economic thinking that this is regarded as a balanced narrative.

It is clear to me that views outside the IFoA’s current policy framework will need to come from elsewhere. I am currently researching a paper on alternative approaches to pensions provision with Alan Swallow which I hope we will be able to publish something about soon.