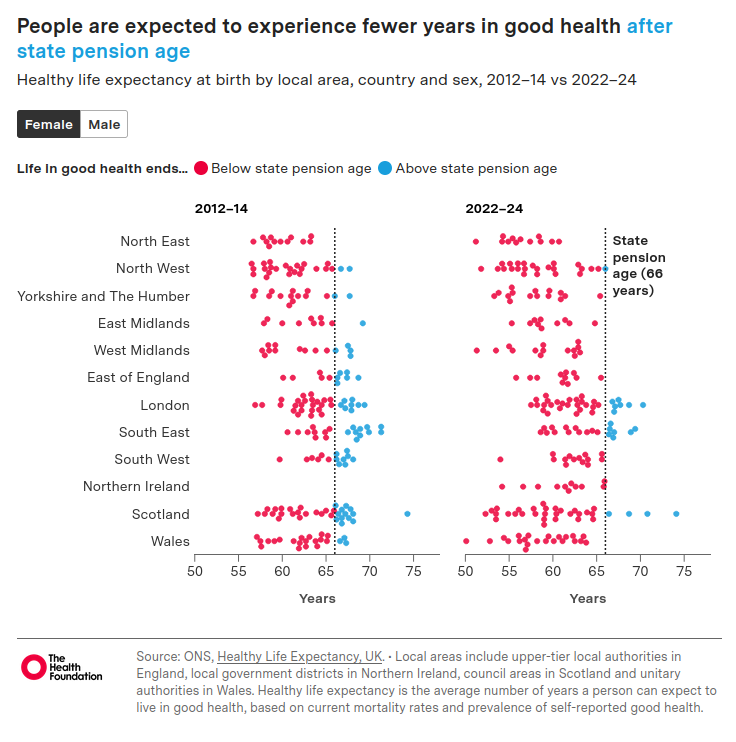

Yesterday an extraordinary thing happened: the news story about the UK’s falling healthy life expectancy led the BBC News for a while, ahead of the King’s visit to the US in the wake of the assassination attempt on Trump’s team and the latest twists in the Mandelson affair. And so it should: over the decade 2012–14 to 2022–24, healthy life expectancy in the UK fell by about 2 years, to 60.7 years for males and 60.9 years for females.

And that is just the average. As we can see from what I felt was the most informative graphic from the Health Foundation’s report, some of the local authority areas have seen precipitous falls over the same period. Merthyr Tydfil has fallen from 57.6 years to 50.1 years. North Lanarkshire has fallen from 58.3 years to 52.3 years. And in England, Sandwell has fallen from 57.7 years to 51.3 years. In the 2012-14 data, only one region had no local authorities with a healthy life expectancy below the state pension age. By 2022-24, most regions have a healthy life expectancy below 66 years.

Healthy Life Expectancy (HLE) is defined as the number of remaining years that an individual can expect to live in “very good” or “good” general health. Rates of “very good” and “good” general health by sex and five-year age band are captured from the following survey general health question on the Annual Population Survey (APS) and in the Census 2011 and Census 2021:

How is your health in general; would you say it was…

Very good?

Good?

Fair?

Bad?

Very bad?

I last wrote about HLE in 2017 in response to John Cridland’s review of the State Pension Age. My view at that time, when healthy life expectancy was plateauing rather than falling like a stone, was that it was time to consider a universal basic income model. Then only the poorest decile was going to be condemned to 18 years of working in poor health until they could claim a state pension. Now the overall averages in some local authorities have moved down to join them, this consideration appears rather more urgent.

In 2014, I was concerned about what happens if the healthy life expectancy doesn’t increase in line with the planned increases to the State Pension Age and, towed along 10 years behind it, Normal Minimum Pension Age (NMPA). Well here we are: 26 of the little local authority blobs are at or below the current NMPA of 55. This nearly doubles to 49 local authorities (assuming the fall in HLE doesn’t continue, which feels like a heroic assumption at the moment) when the NMPA is due to rise to 57 in April 2028.

As the Health Foundation report says:

While healthy life expectancy has declined, life expectancy has remained broadly stable for the UK overall, indicating that the deterioration is not primarily driven by changes in mortality. However, in more deprived areas, life expectancy remains below pre-pandemic levels, suggesting mortality plays a greater role in reducing healthy life expectancy in these areas. Worsening self-reported health remains a key factor throughout the UK, highlighted by a falling proportion of life spent in good health and by wider evidence of declining health among the working-age population.

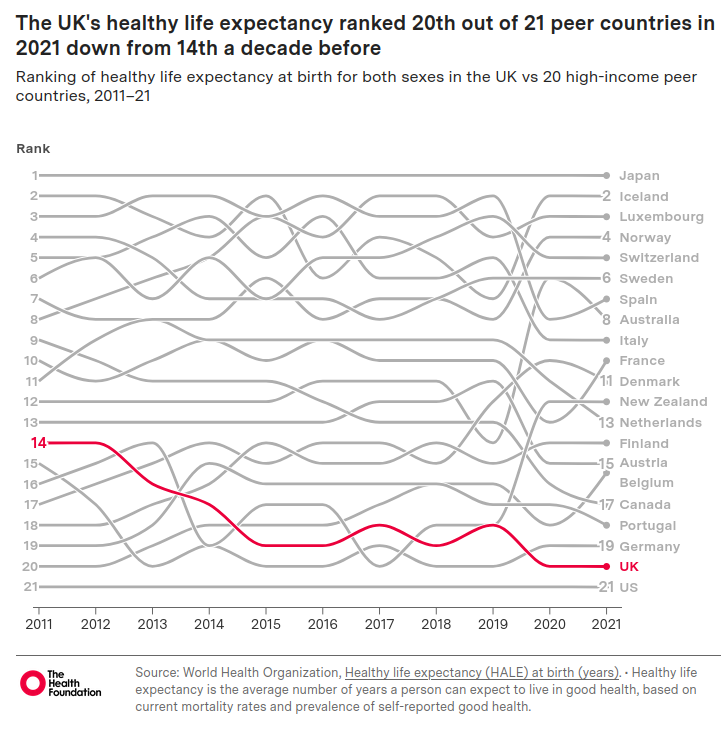

Other countries have not experienced this, illustrated by the UK sliding down the international comparison tables:

In the complete table the UK is sandwiched between Puerto Rico and China, with (from World Bank data) GDP per capita respectively of $39,344 and $13,303, compared to the UK’s GDP per capita of $53,246 (all from 2024).

Andrew Mooney, The Health Foundation’s principal data analyst, said: “The UK has the highest levels of obesity in western Europe and there has been a surge in mental ill health, especially among young people.”

Perhaps, instead of obsessing over GDP growth, we should be focusing on what countries like Iceland, Norway, Australia and New Zealand have been doing in recent years to tackle population health. I think it would make us all feel better.

In my last post I referred to Dan Wang’s excellent new book, Breakneck, which I have now read at (for me) breakneck speed, finishing it in a week. It has made me realise how very little I knew about China.

Wang makes the point that China today is reminiscent of the US of a century ago. However he also makes the point that parts of the US were terrible to live in then: from racist segregation and lack of representation, to massive industrial pollution and insensitive planning decisions. As he says of the US:

The public soured on the idea of broad deference to US technocrats and engineers: urban planners (who were uprooting whole neighborhoods), defense officials (who were prosecuting the war in Vietnam), and industry regulators (who were cozying up to companies).

China meanwhile has a Politburo stuffed with engineers and is capable of making snap decisions without much regard to what people want. There is a sense of precarity about life there, with people treated as aggregates rather than as individuals. The country can take off in different directions very quickly and often does – there is a telling passage about the totally different life experiences of someone born in 1959 compared to someone born in 1949 (the worst year to be born in China according to Wang) – and even the elites can be dealt with brutally if they fall out of line with the current direction of travel. But they have created some impressive infrastructure, something which has become problematic for the US. Only around 10% of its GDP goes towards social spending, compared to 20% in the US and 30% amongst some European states, so there is no effective safety net. Think of the US portrayed in (as Christmas is fast approaching) “It’s a Wonderful Life” – a life that is hard to the point of brutality with destitution only one mistake away. And there is a level of social control alien to the west, controlling where people can live and work and very repressive of ethnoreligious minorities. And yet there is a feeling of progress and forward momentum which appears to be popular with most people in China.

As Wang notes at the end of his introduction:

“Breakneck” is the story of the Chinese state that yanked its people into modernity – an action rightfully envied by much of the world – using means that ran roughshod over many – an approach rightfully disdained by much of the world. It is also a reminder that the United States once knew the virtues of speed and ambitious construction.

The chapter on the one child policy, which ran for 35 years, is particularly chilling (China announced its first population fall in 2023 and its population is projected to halve to 700 million by 2100), and now the pressure is on women to have more children again. There is also a chapter on how China dealt with Covid – Wang experienced this first hand from Shanghai for 3 years – which made me understand perhaps why we wasted so much money in the UK on Track and Trace. You would need to be an engineering state to see it through successfully, and China ended up taking it too far in the end.

The economics of China is really interesting. As Wang notes:

China’s overbuilding has produced deep social, financial and environmental costs. The United States has no need to emulate it uncritically. But the Chinese experience does offer political lessons for America. China has shown that financial constraints are less binding than they are cracked up to be. As John Maynard Keynes said, “Anything we can actually do we can afford.” For an infrastructure-starved place like the United States, construction can generate long-run gains from higher economic activity that eventually surpass the immediate construction costs. And the experience of building big in underserved places is a means of redistribution that makes locals happy while satisfying fiscal conservatives who are normally skeptical of welfare payments.

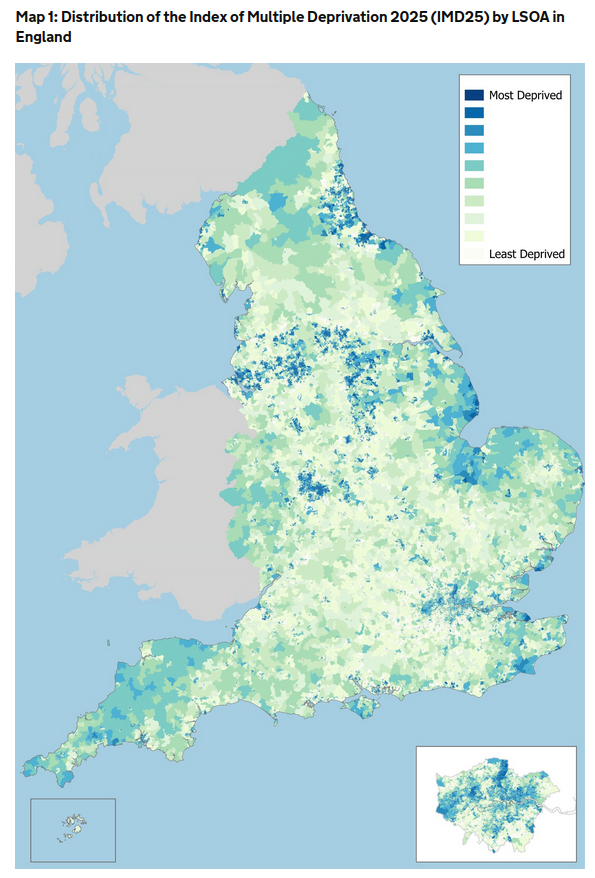

This goes just as much for the UK, where pretty much everywhere outside London is infrastructure-starved (and, as Nicholas Shaxson and John Christensen show here in their written evidence to a UK Parliamentary Committee, even where infrastructure is built outside London, the financing of it sucks money away from the area where the infrastructure is being built and towards finance centres, predominantly in London), but there is also strong resistance from all the main parties to significant redistribution via the benefit system. This results in inequalities which even the FT feels moved to comment on and a map of multiple deprivation in England which looks like this:

The good news is that it doesn’t have to be this way in the UK, there are prominent examples of countries operating in a different way, eg China. The bad news is that China is not doing it because of economics. They are doing it because the state was set up to build big from the beginning. It is in its nature. The lesson of China is that it will keep doing the same things whatever the situation (eg trying to fix the population fall caused by an engineering solution with another engineering solution). Sometimes the world economy will reward their approach and sometimes it will punish it, but that will not be the primary driver for how they behave. I think this may be true of the US, the EU states and the UK too.

Daniel Kahneman showed us in Thinking Fast and Slow, how most of our mental space is used to rationalise decisions we have already taken. One of the places where I part company with Wang is in his reverence for economists. He believes that the US should listen more to both engineers and economists to challenge the lawyerly society.

In the foreword for The Principles of Economics Course from 1990 by Phillip Saunders and William Walstad, Paul Samuelson, the first person from the US to win the Nobel Memorial Prize in Economic Sciences in 1970, wrote:

“Poets are the unacknowledged legislators of the World.” It was a poet who said that, exercising occupational license. Some sage, it may have been I, declared in similar vein: “I don’t care who writes a nation’s laws—or crafts its advanced treaties—if I can write its economic textbooks.” The first lick is the privileged one, impinging on the beginner’s tabula rasa at its most impressionable state.

My view would be that the economists are already in charge.

As a result, my fear is that economics is now used for rationalising decisions we have already made in many countries now, including our own. We are going to do what we are going to do. The economics is just the fig leaf we use to rationalise what may otherwise appear unfair, cruel, divisive and hope-denying policies. The financial constraints are less than they are cracked up to be, but they are a convenient fiction for a government which lacks any guiding principles for spending and investment otherwise and therefore fears that everyone would just be asking for more resources in its absence, and they would have no way of deciding between them.

Title page vignette of Hard Times by Charles Dickens. Thomas Gradgrind Apprehends His Children Louisa and Tom at the Circus, 1870

It was Fredric Jameson (according to Owen Hatherley in the New Statesman) who first said:

“It seems to be easier for us today to imagine the thoroughgoing deterioration of the earth and of nature than the breakdown of late capitalism”. I was reminded of this by my reading this week.

It all started when I began watching Shifty, Adam Curtis’ latest set of films on iPlayer aiming to convey a sense of shifting power structures and where they might lead. Alongside the startling revelation that The Land of Make Believe by Bucks Fizz was written as an anti-Thatcher protest song, there was a short clip of Eric Hobsbawm talking about all of the words which needed to be invented in the late 18th century and early 19th to allow people to discuss the rise of capitalism and its implications. So I picked up a copy of his The Age of Revolution 1789-1848 to look into this a little further.

The first chapter of Hobsbawm’s introduction from 1962, the year of my birth, expanded on the list:

Words are witnesses which often speak louder than documents. Let us consider a few English words which were invented, or gained their modern meanings, substantially in the period of sixty years with which this volume deals. They are such words as ‘industry’, ‘industrialist’, ‘factory’, ‘middle class’, ‘working class’, ‘capitalism’ and ‘socialism’. They include ‘aristocracy’ as well as ‘railway’, ‘liberal’ and ‘conservative’ as political terms, ‘nationality’, ‘scientist’ and ‘engineer’, ‘proletariat’ and (economic) ‘crisis’. ‘Utilitarian’ and ‘statistics’, ‘sociology’ and several other names of modern sciences, ‘journalism’ and ‘ideology’, are all coinages or adaptations of this period. So is ‘strike’ and ‘pauperism’.

What is striking about these words is how they frame most of our economic and political discussions still. The term “middle class” originated in 1812. Noone referred to an “industrial revolution” until English and French socialists did in the 1820s, despite what it described having been in progress since at least the 1780s.

Today the founder of the World Economic Forum has coined the phrase “Fourth Industrial Revolution” or 4IR or Industry 4.0 for those who prefer something snappier. Its blurb is positively messianic:

The Fourth Industrial Revolution represents a fundamental change in the way we live, work and relate to one another. It is a new chapter in human development, enabled by extraordinary technology advances commensurate with those of the first, second and third industrial revolutions. These advances are merging the physical, digital and biological worlds in ways that create both huge promise and potential peril. The speed, breadth and depth of this revolution is forcing us to rethink how countries develop, how organisations create value and even what it means to be human. The Fourth Industrial Revolution is about more than just technology-driven change; it is an opportunity to help everyone, including leaders, policy-makers and people from all income groups and nations, to harness converging technologies in order to create an inclusive, human-centred future. The real opportunity is to look beyond technology, and find ways to give the greatest number of people the ability to positively impact their families, organisations and communities.

Note that, despite the slight concession in the last couple of sentences that an industrial revolution is about more then technology-driven change, they are clear that the technology is the main thing. It is also confused: is the future they see one in which “technology advances merge the physical, digital and biological worlds” to such an extent that we have “to rethink” what it “means to be human”? Or are we creating an “inclusive, human-centred future”?

Hobsbawm describes why utilitarianism (” the greatest happiness of the greatest number”) never really took off amongst the newly created middle class, who rejected Hobbes in favour of Locke because “he at least put private property beyond the range of interference and attack as the most basic of ‘natural rights'”, whereas Hobbes would have seen it as just another form of utility. This then led to this natural order of property ownership being woven into the reassuring (for property owners) political economy of Adam Smith and the natural social order arising from “sovereign individuals of a certain psychological constitution pursuing their self-interest in competition with one another”. This was of course the underpinning theory of capitalism.

Hobsbawm then describes the society of Britain in the 1840s in the following terms:

A pietistic protestantism, rigid, self-righteous, unintellectual, obsessed with puritan morality to the point where hypocrisy was its automatic companion, dominated this desolate epoch.

In 1851 access to the professions in Britain was extremely limited, requiring long years of education to support oneself through and opportunities to do so which were rare. There were 16,000 lawyers (not counting judges) but only 1,700 law students. There were 17,000 physicians and surgeons and 3,500 medical students and assistants. The UK population in 1851 was around 27 million. Compare these numbers to the relatively tiny actuarial profession in the UK today, with around 19,000 members overall in the UK.

The only real opening to the professions for many was therefore teaching. In Britain “76,000 men and women in 1851 described themselves as schoolmasters/mistresses or general teachers, not to mention the 20,000 or so governesses, the well-known last resource of penniless educated girls unable or unwilling to earn their living in less respectable ways”.

Admittedly most professions were only just establishing themselves in the 1840s. My own, despite actuarial activity getting off the ground in earnest with Edmund Halley’s demonstration of how the terms of the English Government’s life annuities issue of 1692 were more generous than it realised, did not form the Institute of Actuaries (now part of the Institute and Faculty of Actuaries) until 1848. The Pharmaceutical Society of Great Britain (now the Royal Pharmaceutical Society) was formed in 1841. The Royal College of Veterinary Surgeons was established by royal charter in 1844. The Royal Institute of British Architects (RIBA) was founded in 1834. The Society of Telegraph Engineers, later the Institute of Electrical Engineers (now part of the Institute of Engineering and Technology), was formed in 1871. The Edinburgh Society of Accountants and the Glasgow Institute of Accountants and Actuaries were granted royal charters in the mid 1850s, before England’s various accounting institutes merged into the Institute of Chartered Accountants in England and Wales in 1880.

However “for every man who moved up into the business classes, a greater number necessarily moved down. In the second place economic independence required technical qualifications, attitudes of mind, or financial resources (however modest) which were simply not in the possession of most men and women.” As Hobsbawm goes on to say, it was a system which:

…trod the unvirtuous, the weak, the sinful (i.e. those who neither made money nor controlled their emotional or financial expenditures) into the mud where they so plainly belonged, deserving at best only of their betters’ charity. There was some capitalist economic sense in this. Small entrepreneurs had to plough back much of their profits into the business if they were to become big entrepreneurs. The masses of new proletarians had to be broken into the industrial rhythm of labour by the most draconic labour discipline, or left to rot if they would not accept it. And yet even today the heart contracts at the sight of the landscape constructed by that generation.

This was the landscape upon which the professions alongside much else of our modern world were constructed. The industrial revolution is often presented in a way that suggests that technical innovations were its main driver, but Hobsbawm shows us that this was not so. As he says:

Fortunately few intellectual refinements were necessary to make the Industrial Revolution. Its technical inventions were exceedingly modest, and in no way beyond the scope of intelligent artisans experimenting in their workshops, or of the constructive capacities of carpenters, millwrights and locksmiths: the flying shuttle, the spinning jenny, the mule. Even its scientifically most sophisticated machine, James Watt’s rotary steam-engine (1784), required no more physics than had been available for the best part of a century—the proper theory of steam engines was only developed ex post facto by the Frenchman Carnot in the 1820s—and could build on several generations of practical employment for steam engines, mostly in mines.

What it did require though was the obliteration of alternatives for the vast majority of people to “the industrial rhythm of labour” and a radical reinvention of the language.

These are not easy things to accomplish which is why we cannot easily imagine the breakdown of late capitalism. However if we focus on AI etc as the drivers of the next industrial revolution, we will probably be missing where the action really is.

This blog has a long history with the OBR, which I won’t go into here, although you can get a sense of it from this. It was the reason the blog is called We Know Zero. However I find myself returning to talk about them once again in the light of some of the Government’s latest spending (or removal of spending) plans.

Daniel Susskind had this to say about the role they are currently playing for the Government, to determine whether it is going the right way to achieve economic growth:

This was never meant to be the OBR’s purpose. Set up in 2010 by George Osborne, then chancellor, it was designed to solve a different problem: that the official UK public finance forecasts were not credible. The Treasury had a strong incentive to massage these numbers into better shape, whatever the political make-up of the government. And the belief was that an independent statistical authority would be free of that temptation. To that extent, the OBR is a success story: its forecasts do appear to be less biased.

At this point I need to stifle a snigger: less biased than what? I think it may not have a political reason for bias, but their methodology is like train tracks as I have maintained since this blog started in 2013: if you lay them out in a particular way then, even if you don’t want to call it bias, that is the way the train will run (to misquote Yes Minister). It may be statistically unbiased, in the same way that someone who misses a penalty past each post (I am sure that this analogy has nothing to do with my team going out of the Champions League this week) has, on average, hit the target.

However I agree with Susskind that the OBR was certainly never set up to advise on policy. As he goes on to say:

With that in mind, the idea that the OBR somehow knows enough to take each UK government policy and state its impact on growth to a single decimal point is fanciful. Yet that is what it will attempt to do at the end of the month, with immense practical consequence. A reduction of 0.1 percentage point in the OBR’s potential productivity growth forecast, for instance, is estimated to create a hole of £7bn-£8bn in the public finances — that is the equivalent of the entire budget of Defra.

Or the foreign aid budget or disability benefits or…the list looks likely to go on.

In an open letter this week, 17 major charities including Scope, Trussell Trust, Citizens Advice, Mencap, Sense, the Joseph Rowntree Foundation and the RNIB urged the Government not to cut the Personal Independence Payments (PIP) and the Limited Capability for Work payment, saying:

Scope’s analysis of government figures shows that without PIP, a further 700,000 more disabled households could be pushed into poverty. Life costs more for disabled people. Huge numbers already live in poverty as a result of these extra costs. The impact of any cuts to disability benefits would be devastating.

Meanwhile Roy Lilley looks at those cuts from the NHS end of the lens. I don’t agree with his assessment of the IFS, but there is nothing else here to argue with:

Currently, 2.9 million working-age adults are claiming disability benefits, an increase of 900,000 from pre-pandemic levels, with 500,000 attributing their main condition to mental health issues.

Lilley asks why this is, comparing the mental stress attributed to the pandemic with that of the Blitz. He then cites a study by the Tavistock Institute:

While, in the post war years, mental health issues were still stigmatised, post-war policies focused on social security and housing aimed to reduce economic stress that so often is the contributing factor to poor mental health.

We have done a lot to reduce the stigma of mental health issues, but:

I question the policies. Social and economic factors. Job insecurity and financial stress must be the key factors that have a negative impact on mental health well being.

Back to the Trussell Trust, who have been running a campaign for a while now to guarantee everyone the essentials to live on. As they say:

More than three quarters of people on Universal Credit and disability payments have already gone without essentials in the last six months.

Back to Lilley, who as I said, is primarily concerned with the NHS:

Since 2019 the NHS has experienced a 36% increase in patients seeking mental health services.

As he goes on to say:

Labour’s plan to cut benefits won’t solve the problem. It’ll very likely make it worse.

Policies cutting the root causes of people needing benefits, like safe homes and decent jobs would seem much more sensible.

The year is 2100. Earth is approaching a peak population of 9.5 billion people. Despite some notable progress in decarbonising our activities and more progress on carbon capture of various types than expected 80 years ago, overall we have not managed to shift much off the Intergovernmental Panel on Climate Change (IPCC) middle-of-the-road shared socioeconomic pathway (SSP2). Some countries have done much better than others, with income inequality a problem both within and between them. Carbon emissions stayed fairly level until 2050 before starting to fall, but net zero has still not been achieved.1

Temperatures have risen by 2.7 degrees compared to pre-industrial levels. Africa has split between a north which has seen a recovery of rainfall and a south which is no longer habitable for humans. The Indian monsoon rains have failed. The Himalayan glaciers providing the waters of the Indus, Ganges and Brahmaputra, the Mekong, Yangtze and Yellow rivers have reduced by 90% from their pre-industrial levels.

The Amazonian rain forest basin has dried out completely. In Brazil, Venezuela, Columbia, East Peru and Bolivia life has become increasingly difficult due to wild fires. Drought is now permanent in the sub-tropics and Central America. Australia has become the world’s driest nation.

In the US Gulf of Mexico high sea temperatures drive 180+ mph winds.2 Flooding is widespread with sea levels having risen by 0.6 metres on average compared to 2020.3 Many plant species have become extinct as they were unable to adapt to such a sudden change in climate.

Food prices continue to soar, with temperatures, droughts and the inundation of arable land adversely affecting many crops. Massive migrations have led to increasingly severe military and police responses from the most popular destination countries. There is fear that we have not yet seen the end of the terrible costs of climate change, with temperatures continuing to rise.

England has a new Eastern coastline, which became a certainty once the decision was taken that the cost benefit analysis did not justify the expense on the massive coastal defences which would have been required to prevent it. Sleaford is now a seaside town. Birmingham is the only major city which has not been significantly affected by sea level rise4 and there are calls for the capital to be moved there. However London hangs grimly on following the failure of the Thames Barrier in the 2040s. An Intertidal Property Pricing Index (IPPI) has sprung up, which sucks in money as investors bet on the development opportunities in the aftermath of the catastrophe.5

This, or something like it, is the future we are currently on track for but none of us wants. So let’s change the trajectory.

Notes:

The IPCC’s SSP2 narrative description.

Mark Lynas, Six Degrees: Our Future On A Hotter Planet, Harper Perennial, 2008 for the scientific consensus at the time on the consequences of 3 degrees warming

https://sealevel.nasa.gov/ipcc-ar6-sea-level-projection-tool?type=global (accessed 5 July 2023)

https://coastal.climatecentral.org/ (accessed 5 July 2023) for the maps of England following 2.7 degrees warming by 2100 following current trajectories

IPPI borrowed from Kim Stanley Robinson’s depiction of a future New York after two pulses totalling 15 metres (50 feet) of sea level rise in New York 2140, Orbit, 2018

For those of you who have ever bought or sold a house (and I realise that that is a dwindling proportion as we move down the age ranges), it occurred to me that the UK increasingly resembles the worst kind of vendor. The sort that removes the lightbulbs and the doorknobs before giving up possession.

Harold Macmillan referred to Margaret Thatcher’s Government “selling off the family silver” in response to the widespread privatisations of public assets at the time. This Government has gone further, denying funding to the health and social security safety net we all rely on to such an extent that, as Health Equity in England: The Marmot’s Review 10 Years On found in 2020:

people can expect to spend more of their lives in poor health;

improvements to life expectancy have stalled, and declined for women in the most deprived 10% of areas;

the health gap has grown between wealthy and deprived areas; and

living in a deprived area of the North East is worse for your health than living in a similarly deprived area in London, to the extent that life expectancy is nearly five years less.

However it is even worse than that. I once bought a house from a man who had done all of his own plumbing, despite being a telephone engineer. He proudly took me up to the airing cupboard, where the boiler room displayed piping of complexity which would not have been out of place on a nuclear submarine.

“Everything has its own stop cock.” He said. He might even have called them isolation valves. I just thought of how many different leaks were possible from what he had constructed.

And so it proved. We had a plumber on speed dial before long and, with every new job he undertook for us, most of which was to undo the “work” of which the former owner had been so proud, he used to intone “what a man”, more to himself than to us.

Brexit, even as its architects start to disavow it in the face of the increasingly overwhelming evidence of the bullet holes in our own feet, is our home-made plumbing. And I am sure that there are any number of people around the world, looking at us and intoning “what a man” to themselves. It no longer matters to most of us how much the Brexiteers think they have buffed up their sovereignty isolation valves. Every week brings a new story about another leak of what Macmillan endearingly referred to as our “treasure” that it has enabled.

On immigration, we are like that house on the street which noone from the area wants to go anywhere near. Neighbours only reluctantly enter into any kind of dispute about who should replace the shared fence. There is a huge-sounding dog which barks at you fiercely if you venture up the driveway, on which the only car is on bricks. It feels like, if we were to ultimately die as a nation, noone would notice for years until the smell coming from inside became too much for anyone to ignore any more.

Anyway, enough of all that. I am off to the Hay Festival tomorrow for my annual infusion of ideas, erudition and words just flowing all around me. And so I must leave you with a book recommendation. I will be taking The Golden Mole by Katherine Rundell with me, a brilliant beautifully illustrated book (illustrations by Talya Baldwin) with each chapter focused on a different endangered species. Sounds bleak? No! The writing is so good that you are soon just overwhelmed by the richness you hadn’t even been aware of and might otherwise never have been. I have been reading it very slowly as I really do not want it to end. As Katherine says about The Human at the end of the book, with a different take on treasure:

For what is the finest treasure? Life. It is everything that lives, and the earth upon which they depend: narwhal, spider, pangolin, swift, faulted and shining human. It calls out for more furious, more iron-willed treasuring.

I have this book because Katherine described it so compellingly in an interview at the Hay Winter Festival (a smaller one in November each year). She has also written a book about John Donne, the metaphysical poet, called Super-Infinite. I had not considered until now that I was remotely interested in John Donne, but I also cannot imagine that the week will pass without me buying this and reading it too.

I recently finished reading Chasm City by Alastair Reynolds, which I highly recommend. In it, sufficiently rich people have been able to buy a programme of treatments which make them immortal. Not that they can’t die, but they needn’t if they’re careful. Good science fiction, I thought.

Then I read Paul Kitson’s (the new UK Head of Pensions Consulting at EY) piece on LinkedIn where he wrote (bold mine):

Pension schemes, corporate sponsors, members – everyone, in fact – must now contend with a forward looking plan that (somehow!) considers on one side the possibility of future pandemic outbreaks shortening life expectancy, and on the other side the many £billions being spent on ‘regenerative medicine’ (AKA “the ending of ageing” or “escape velocity for death”!).

So perhaps not entirely, I thought.

In Chasm City, the immortals who live in “the Canopy” have two main problems:

Hanging on to their wealth and, if possible, increasing it, as forever is a long time to finance.

Boredom.

One particular group amuse themselves by hunting poor people in “the Mulch” (lower level where the poor live). Others indulge in increasingly dangerous pastimes to inject some urgency into the otherwise featureless expanse of their lives. No wealth moves from the Canopy to the Mulch, not even in a trickle.

I am just finishing Do Androids Dream of Electric Sheep by Philip K Dick (a classic, I know, but I hadn’t read it before, although I have seen Bladerunner). One of the features of the post-apocalyptic world of 1992 described are “mood organs” which allow you to dial up a given mood at any time, eg 481 is “awareness of the manifold possibilities open to me in the future” whereas 888 is the desire to watch TV, no matter what’s on it. Again, good science fiction, I thought.

Then I read a piece in this months’ Actuary magazine called Apt apps, about doctors being recommended by NICE to offer patients with insomnia the Sleepio app as an effective and cost-saving alternative to sleeping pills. So perhaps not entirely, I thought.

The first book was written in 2001 and the second in 1968, so it would seem that lead times are variable.

Both books deal with the fragility of identity, whether via memory implants and religious viruses in Reynolds’ book or how we go about separating androids from people from “chickenheads” in Dick’s. The divisions between the life experiences of the different groups are so stark, but it is the characteristics of the people in them which takes up everyone’s time and attention in both books, rather than the structure of the societies which create such extreme winners and losers. Which suddenly doesn’t feel like science fiction at all.

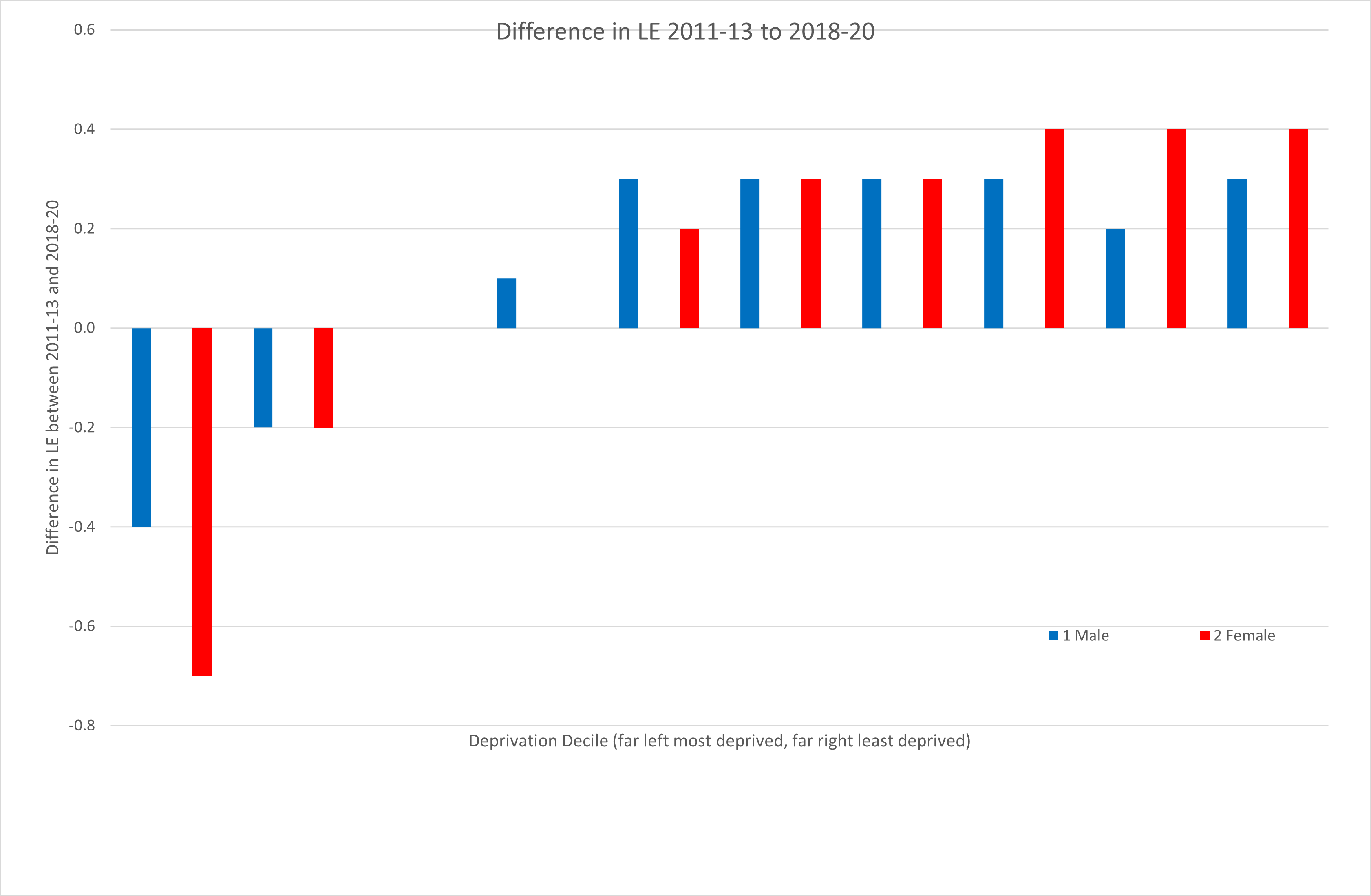

Meanwhile what has happened to England’s life expectancies by decile of deprivation in the last 10 years?

Source: ONS https://www.ons.gov.uk/peoplepopulationandcommunity/healthandsocialcare/healthinequalities/bulletins/healthstatelifeexpectanciesbyindexofmultipledeprivationimd/2018to2020#health-state-life-expectancies-data

So not quite immortality yet at the top, but inequality is clearly worsening in life expectancy. The Government Actuary’s Department gave an upbeat view last year on what the impact of the recent Levelling Up White Paper might be. Others are upbeat too.

However the Government’s track record is not good on inequality. Sir Michael Marmot produced the Marmot Review on health inequalities in the UK in 2010 and then followed this up with a review of what progress had been made 10 years later. As he points out in his recent interview in The Actuary:

Health spending fell from around 42% to 35% during the 2010s. He notes that this reduction was carried out in a regressive way: “There has been a 16% reduction in health spending for the most affluent, but a 32% reduction for the most deprived groups.” In addition, he says, while unemployment fell over the course of the decade, the income of employed people also went down – so the proportion of people living in poverty rose, as did child poverty.

These are the kinds of interventions that matter for most people rather than sleep apps or regenerative medicine to achieve escape velocity from death. And they are definitely not science fiction.

NASA, ESA, and the Hubble Heritage Team (STScI/AURA), Public domain, via Wikimedia Commons

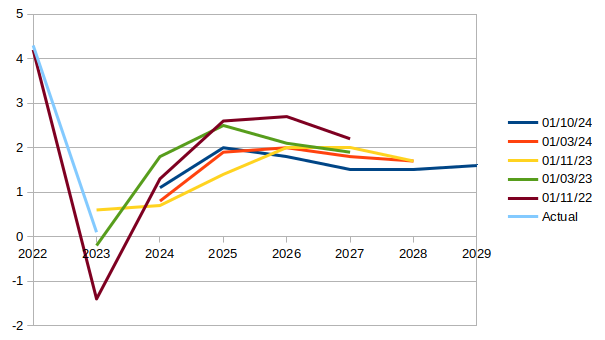

Fiscal space is defined as the difference between a nation’s sovereign debt-to-GDP ratio and the limit beyond which the nation will default unless policymakers take fiscal steps that are outside of anything they have done historically. That limit is sometimes referred to as the fiscal cliff, just to ram home the imagery of fixed physical limits beyond which disaster beckons.

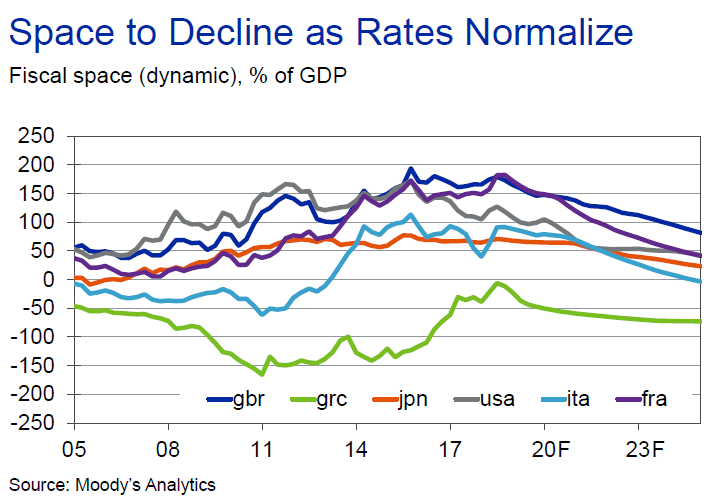

How much fiscal space does the UK have? Moody’s have an answer, which depends most heavily on when you ask the question. In September 2019 it was as follows:

This shows the UK with a fiscal space (the “dynamic” means they assume interest rates increase as borrowing does, due to “crowding out” arguments – ie government borrowing pushing up the price of borrowing for everyone – so beloved of most economists) of around 175% of GDP, with this then projected to fall over the following 5 years as rates “normalized”. While the cost of borrowing seems to be dynamic, the actual borrowing itself is not allowed to be in these calculations – it is assumed that they just add to debt without increasing the revenue components of the primary balance.

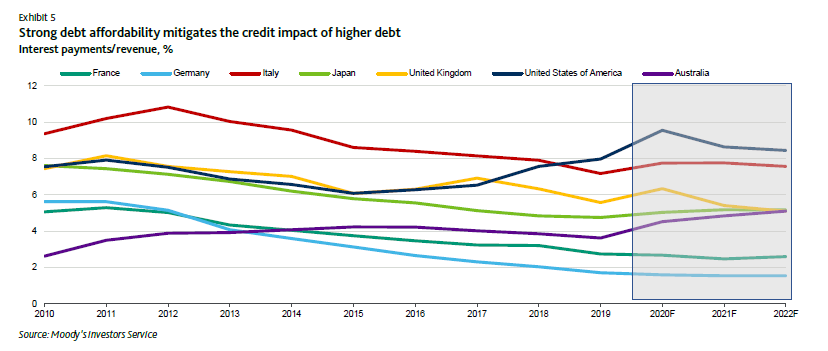

Well of course then we had 2020, at which point (June 2020) Moody’s appear to have stopped talking about fiscal space and instead are now focusing on something called “debt affordability”. What happened to dynamism and crowding out? Not explained:

However despite this triumph of debt affordability, they then produce another graph to indicate that governments still need to be bearing down on debt to GDP ratios:

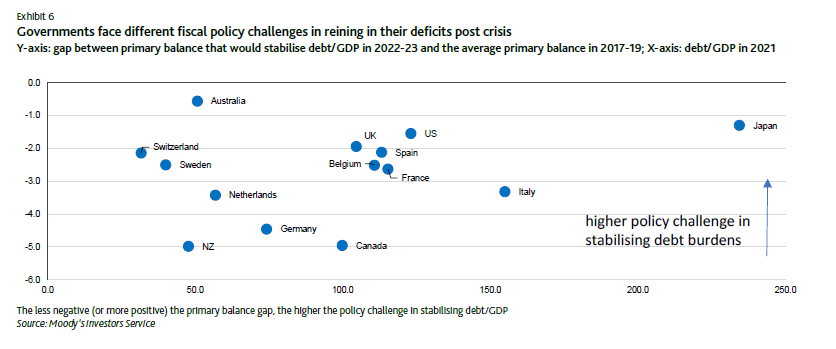

As they say in the document “rating implications will depend on governments’ ability to reverse debt trajectories ahead of potential future shocks”. Remember this was in June 2020. Let’s also remind ourselves of another graph:

Requiring governments to reverse debt trajectories in this environment is insane and likely to result in more deaths if not ignored. However as recently as last month in their issuer comment for the UK they said:

However, compared to the government’s March budget (that was quickly overtaken by events), there are some initial signs that fiscal policy outside of investment is likely to be less expansive than previously announced. What remains unclear is whether this ambition will be able to withstand the political pressures that seem to be inevitable given the government’s previous commitments. Even before the Spending Review, longer-term spending commitments for health, education, and defence had already been announced. Together, these three areas account for around 60% of total expenditure.

I have been hard on Moody’s in this piece, they are most certainly not alone. But this attempt to divorce sovereign debt levels from what is actually going on in countries needs to stop as does the constant discounting of the value of any government spending at all. Political pressures to spend more on health and education are not always things that governments need to “withstand” in order to look good in a Moody’s graph. There are far more important things at stake.

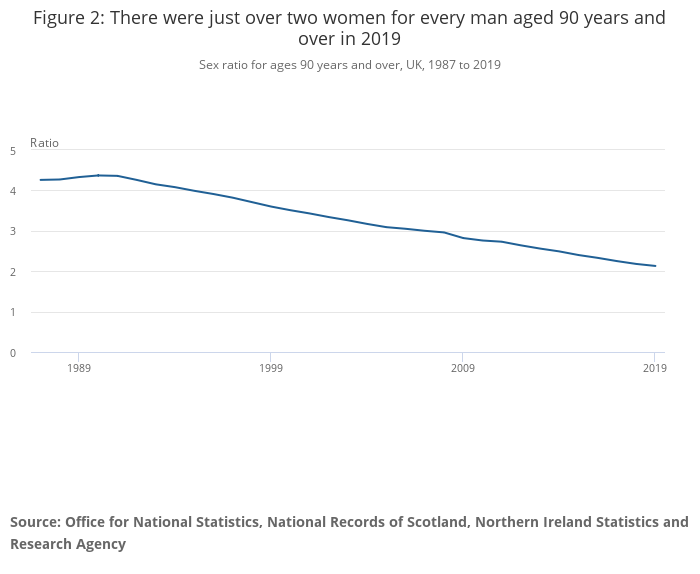

I previously wrote a blog in 2013 based around the Office for National Statistics (ONS) statistical bulletin entitled Estimates of the Very Old (including Centenarians), 2002-2011, England and Wales, which summarises how the proportions living to 90 years old and above have changed since 1981. It showed us a population living within a population: Nonagenarian (ie the over 90s) England and Wales (NEW) within the full population of England and Wales. I thought it might be time for an update, based on the latest ONS bulletin from September 2020, which now covers the period 2002-2019.

There have been quite a few changes. There are still more women than men in NEW, although the overall ratio has reduced from 2.7:1 in 2011 to around 2:1 in 2019 (see below). The NEW population, which was somewhere between the sizes of Malta’s and Cape Verde’s full population in 2011, has now just passed that of Western Sahara and has its sights firmly set on passing Luxembourg’s population next.

The population of NEW is still growing far more quickly than that of England and Wales, or indeed the UK, with a 25% increase between 2011 and 2019. However, with the NEW population you need to look beyond just improvements in public health and medical advances to the time at which they were being born. For instance, the number of people alive at almost every age from 90 years and above was higher in 2019 than in 2018, but with by far the largest increase at age 99 years (62.2%). This was caused by a big increase in births from the second half of 1919, compared to the previous year, as a result of the end of World War 1!

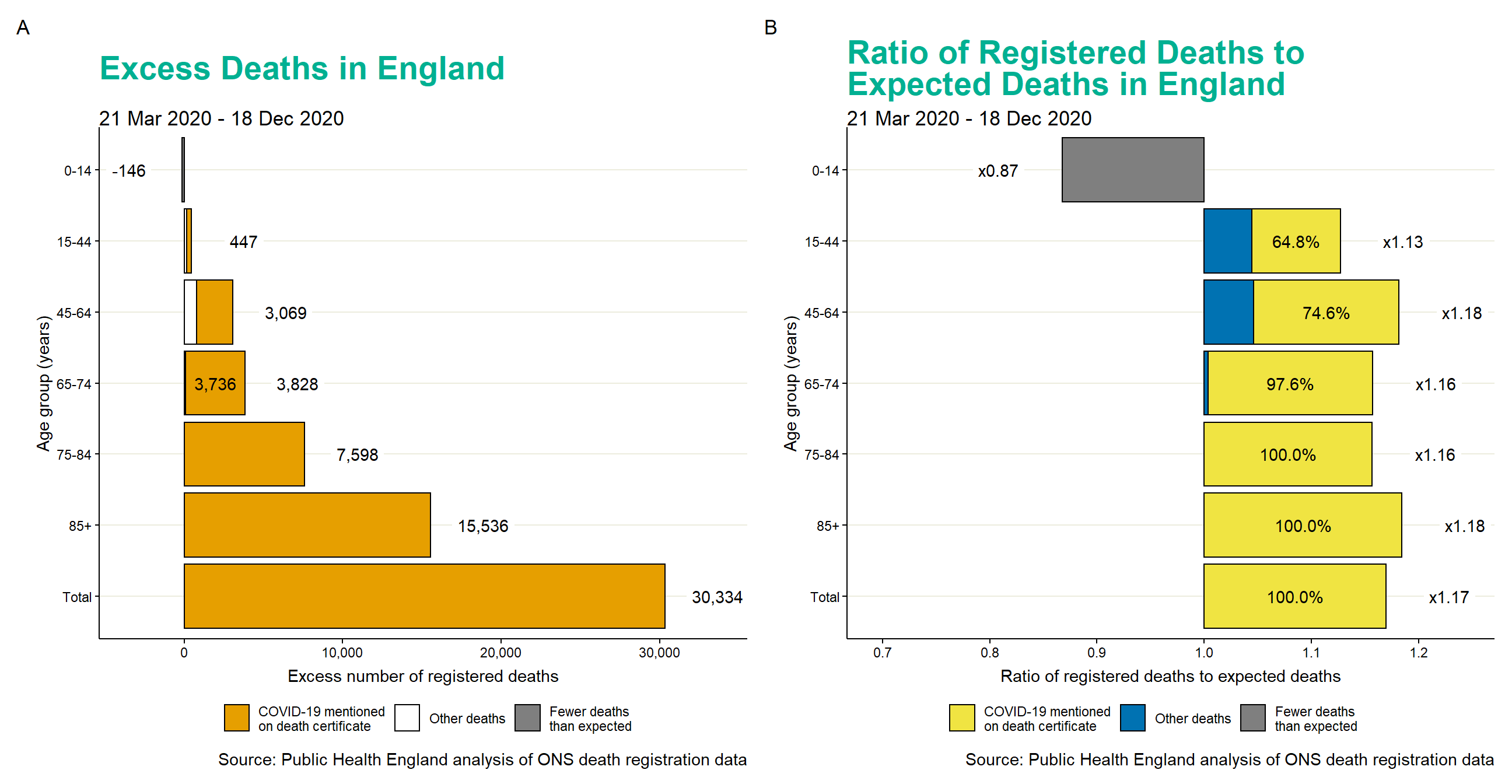

The bulletin ends with a sombre reminder that, although we would normally expect the large increase in those aged 99 years in 2019 to translate into a record number of centenarians in 2020, other factors, particularly the COVID-19 pandemic, are likely to have had a significant impact. COVID-19 deaths are highest for the 85 years and over age group. Public Health England have calculated excess deaths in the over 85 population at 11,656 between 21 March and 18 December 2020 (with 13,844 categorised as COVID deaths, suggesting a drop in excess deaths from other causes). This compares with the 2019 NEW population of 605,181, an increase of 21,157 on 2018.

I am an actuary. I have worked for over 22 years either in, or serving in some capacity (apart from the two years I spent learning to be a teacher), the finance industry. I spent the 12 years before that mostly either bringing up children or writing unpublishable novels, with some early career experiences in the security printing industry thrown in which I thank principally for teaching me early that no way of doing things is for ever. Seven of my former employers no longer exist, mostly swallowed up in subsequent corporate transactions. I am increasingly convinced that a “career” like mine is no longer possible for the next generation, and my most recent evidence for this is based predominantly on two excellent books.

The first is The Finance Curse by Nicholas Shaxson. This demonstrates, convincingly, that a huge part of our current malaise as a nation, whether it is the loss of control over our own affairs, or the current, Victorian, levels of inequality or the fact that we don’t appear to invest in any of things we need to prosper as a society any more, can be traced back ultimately (sometimes via very cunning circuitous routes) to the Faustian pacts the City of London have lobbied the rest of us into with the rest of the world.

The second is The Pinch by David Willetts (and link to his slides – one of which is shown above – on it from 2015 here), whose central argument is that we are not attaching sufficient value to the claims of future generations, and that this is an intellectual failure of my generation: the one that spawned both me and Boris Johnson. I will declare an interest here: David is Chancellor at the University of Leicester, where I work as an actuarial science lecturer, in addition to all of his many other achievements and will be speaking at the Leicester Actuarial Science Society on 11 March on intergenerational fairness linked to a new edition of his book.

So for any highly talented twenty-somethings looking to make his or her mark in the world (and I have been privileged to meet and teach many of you over the last few years), I would, very hesitantly (because you probably don’t need me of all people to be giving you an agenda), suggest that the following things might be a priority for your generation:

Don’t be distracted by the short term. Most people now want action on climate change, for instance, which has been delayed to a ridiculous extent by our inability to place sufficient value on the needs of future generations. Most of the things worth working towards and campaigning on are long-term problems with solutions which require long-term patient consensus-building. Our generation have been unable to do this seriously, yours cannot afford to be so distracted.

Stay focused on the big issues: What is the proper allocation of wealth between the generations? Most of the problems we fixate on, like obesity or anti-social behaviour or credit card debt are just symptoms of the breakdown of the inter-generational contract which the baby boomers (because we felt that we could do so because of our greater numbers) have visited upon our societies. We have then presumed to pass moral judgement on the generation we have so comprehensively wronged, which is of course an easier message for many in our generation to hear but is one of the main reasons we have become too distracted to deal with the big long-term issues that we face as a society.

Don’t make it all about good guys and bad guys. It is easy to vilify individuals in this great inter-generational psychodrama that we have all been living through, and it might make you feel momentarily more empowered or encouraged as a result, but in the long term the power is with you anyway and you will be more effective if you make it about good and bad systems. Good systems pursue the interests of our own people, whereas bad systems pursue the interests of people who need to be persuaded to invest in our society but have no real long term interest in doing so: ie other societies who clearly need to prioritise their own people’s needs and tax avoiding multinational companies and individuals.

I would like to finish with the concluding sentences of The Pinch:

The modern condition is supposed to be the search for meaning in a world where unreflective obligations to institutions or ways of doing things are eroded. The link between generations past, present and future is a source of meaning which is as natural as could be. It is both cultural and economic, personal and ethical. We must understand and honour those ties which bind the generations.

In the nine years since The Pinch was published we have done the very opposite of honouring the ties which bind the generations. We must hope that the generation following us have more wisdom.