The Welsh Government made a fresh offer to health unions on 3 February which led to a suspension of all health strikes in Wales bar ambulance workers from the Unite union while negotiations continue.

On Friday the TSSA union (17,000 members) announced that members are to be given a vote on offers from the train companies in their long-running national dispute over pay, job security and conditions.

However:

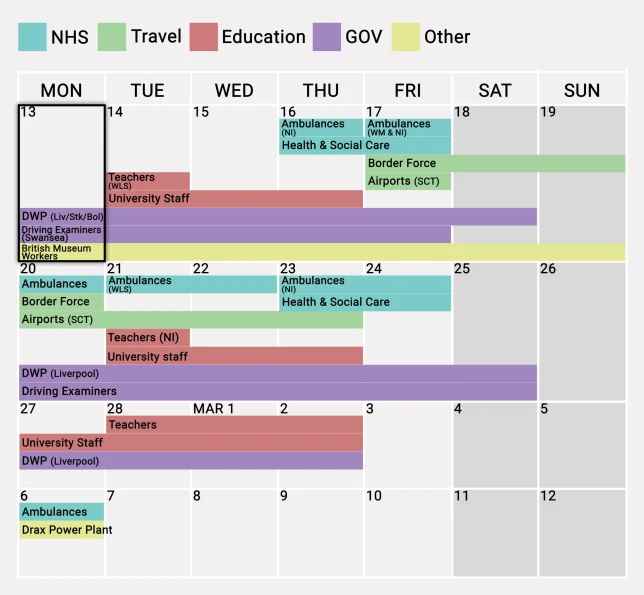

Ambulance workers, teachers and university staff are amongst those striking over the next 3 weeks.

The very much larger union, the RMT (82,000 members), have rejected the train companies’ deal (9% over 2 years) due to the additional conditions attached affecting safety on the railways.

The Scottish Government is in talks with the Royal College of Nursing (RCN) and other unions representing NHS staff over a pay settlement for 2023-24, after imposing a pay deal which would give health workers an average 7.5% rise in December, which RCN nurses rejected.

Nurses from A&E, intensive care and cancer wards could join fresh strikes in England, as the RCN considers a continuous 48-hour strike, which could begin in weeks.

According to Reuters, a recent Chartered Institute of Personnel Development (CIPD) survey indicates that the gap between public and private employers’ wage expectations has widened. Planned pay settlements in the public sector fell to 2% from 3% in the quarter before, compared to a median of 5% in the private sector.

Meanwhile the UCU and the four other higher education unions (EIS, GMB, UNISON and Unite) and employer representatives from the Universities and Colleges Employers Association (UCEA) have agreed to further talks mediated by conciliation service Acas. The discussions began yesterday and continue today, covering pay, equality, job insecurity and workloads.

The strike continues today for three consecutive days. In total 18 days of strike action are planned throughout February and March, with a new strike ballot planned for March.

It seems fairly clear that public sector employers need to offer rather more than they have to date if any of these disputes are going to be resolved any time soon.

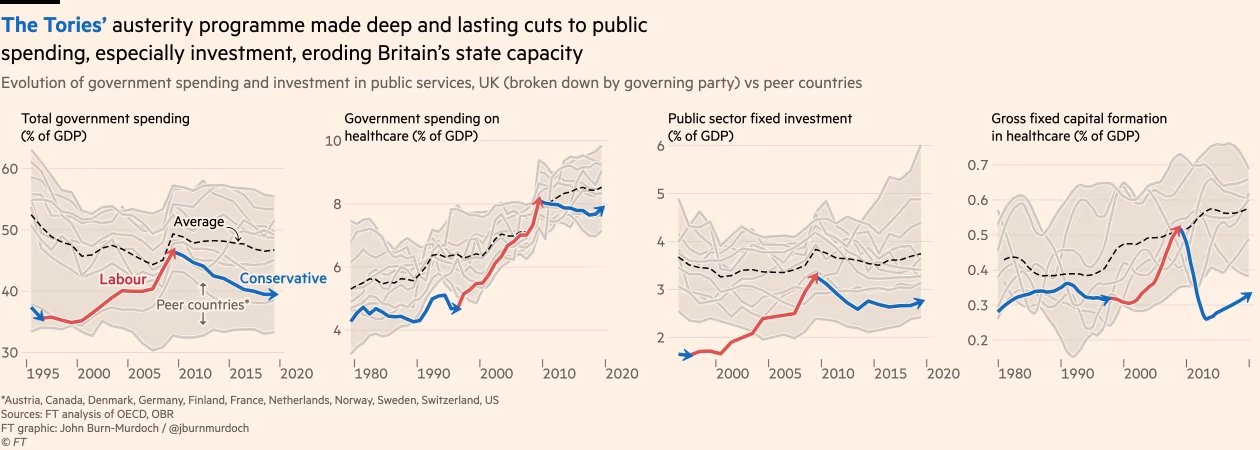

Day 3 of the UCU strike and we move onto fiscal austerity. This is the type of austerity we normally think of – increasing taxes and reducing government spending – and the most prevalent feature of all the UK governments we have had since 2010, with the cumulative lack of investment in the economy which is the underlying cause of most of the industrial action now taking place all around us. People are not just upset that their pay has not kept pace with inflation for 12 years, it is also the cumulative degradation of the conditions under which they work, seek healthcare, seek education for their children, travel anywhere or don ‘t travel anywhere that has enraged so many.

Rishi Sunak says he would love to give nurses a “massive” pay rise, but insists the money needs to be prioritised in other areas of the health service. Jeremy Hunt insists that his priority is tackling inflation and that public sector pay rises cannot be allowed to jeopardise this. Health secretary Steve Barclay hints that striking NHS staff could be offered a better pay deal from April – if unions accept “productivity and efficiency” reforms in return.

But improving productivity at work requires investment in where you work, as numerous studies have confirmed (one example here). Whereas, as the FT has shown recently, the UK has done the following since 2010:

Source: FT graphic by John Burn-Murdoch

And what about Jeremy Hunt’s reasons for keeping pay reducing in real terms in the public sector year after year? That paying an inflation matching increase would in some way “lock in” inflation. As Blair Fix tweeted recently:

Most economists accept that a wage-price spiral is possible, leading to runaway inflation. But why isn’t an interest-price spiral also possible? Interest and wages are just two forms of income. So why is one spiral ‘obvious’ while the other is blasphemy?

It doesn’t make sense until you realize that mainstream economists are in the business of legitimizing capitalist income. Wages can drive inflation (bad workers!) … but capitalist income is always productive.

He has also written about the problems caused by following economic theories treating inflation as a single value, when it is of course an average (or in fact usually at least an average of an average, sometimes switching between arithmetic and geometric averages in the process) taken of a highly volatile underlying data set. It is often said that inflation is redistributive: benefitting borrowers at the expense of lenders. However, one of the insights from Fix’s piece, drawing on Nitzan’s and Bichlar’s work in the 90s, is that big business also benefits from inflation: large corporations and oligopolies are raising prices the fastest at the expense of smaller businesses. Why do we never hear that this is driving inflation?

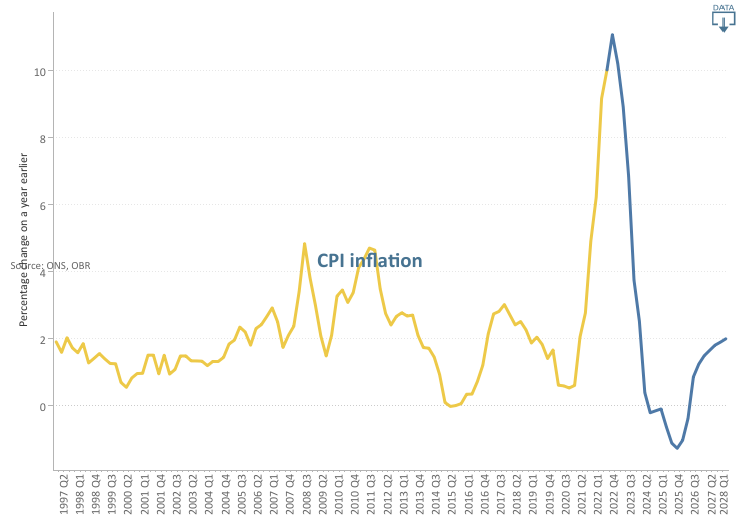

Because capitalist income is, in their view, “always productive”, you won’t hear about rent-price spirals or profit-price spirals from the current Government. Instead we will hear about how inflation needs to be reduced and this can only be done by further depressing the real value of all of our incomes for another year. This is what the Office for Budget Responsibility (OBR) has to say about CPI:

Following the Russian invasion of Ukraine, we now expect CPI inflation to peak in the fourth quarter of 2022 at its highest rate in around 40 years. The increase is driven primarily by higher gas prices feeding into sharp rises in domestic energy bills, alongside higher fuel prices and global goods inflation. Inflation then falls rapidly, and temporarily goes negative in mid-2024 as energy bills fall back and some global supply pressures reverse.

Source: Office for Budget Responsibility

On nominal wage growth and its contribution to Real Household Disposable Income (RHDI) they have this to say:

Nominal wage growth is also high in 2022 and 2023, although not high enough to prevent real wages from falling significantly. The contribution of labour income to annual RHDI growth then settles at an average of 2 percentage points a year over the remainder of the forecast.

Since one of the original motivations for starting this blog was the poor forecasting ability of the OBR, I am not going to set too much store on these forecasts, other than to point out the confidence it has that labour income demands will be thwarted and we will all see our real wages fall significantly over the next year. All in pursuit of a policy for which the expected value appears to be 6 months of deflation.

Deflation would be a disaster, As Frances Coppola has written:

Those who have money are happy because they are becoming wealthier. But someone, somewhere, is going hungry.

As she concludes:

So I’d rather money wasn’t deliberately kept scarce to placate savers. Let the supply of money respond to demand for it. When everyone wants to save in the form of money, you need to produce more of it so those who need to spend money don’t starve. Obviously, we don’t want to create so much money that it becomes worthless. But it is better to risk waking the demon of inflation than to deny people the means to live.

So when the Government says that they need to repress my pay in order to avoid locking in inflation, it reminds me of this paragraph from Catch 22:

Morale was deteriorating and it was all Yossarian’s fault. The country was in peril; he was jeopardizing his traditional rights of freedom and independence by daring to exercise them.

A Government intent on crushing real wage growth or even the hope of it while explicitly targeting deflation within the next two years; an extreme assymetry of power between wage earners on the one hand and lobbying corporations and asset owners on the other. This is why so many of us are exercising our traditional rights today.

It all began for me on 23 September 1985, the first day in my first graduate role as a management trainee at the home counties factory of a security printing firm. From the beginning I was left in no doubt by my new employers that the fairly powerful print unions at the time (SOGAT and the NGA) were the biggest impediment to the captains of industry within the firm from running the business successfully. Occasionally I was allowed into management meetings, where all of the things we could do if it wasn’t for the unions were discussed endlessly.

During my time in this first role, the printing industry changed dramatically: the typesetting was computerised, massively reducing the number employed virtually overnight and Rupert Murdoch set up his non-unionised newspaper factories at Wapping. There had already been three pieces of trade union legislation in the 1980s by the time I started work, the latest being the Trade Union Act of 1984, which required secret ballots for union elections and strikes rather than the show of hands which had been possible up until then. The Miners Strike had also only just ended in March 1985, which had a devastating impact on the trade unions more generally.

Further legislation now quickly followed:

the Public Order Act 1986 (which introduced new offences related to picketing, and increased police powers over protests involving groups of 20 people or more);

the Wages Act 1986 (which reduced many of the restrictions on employers fining and deducting money from employees’ pay, removed statutory holiday entitlement and reduced state funding for redundancies);

the Employment Act 1988 (which gave workers the right to not join a union, and trade union members the right to challenge strike ballots);

the Employment Act 1989 (which restricted trade union officials’ time off for duties and abolished government support for redundancy payments);

the Employment Act 1990 (which finally removed the closed shop – ie a workplace where union membership was compulsory – and secondary action protection);

the Trade Union and Labour Relations (Consolidation) Act 1992, which consolidated the legislation of the 80s and 90s, while clarifying that the right to take strike action was protected when it was “in contemplation or furtherance of a trade dispute”; and

the Trade Union Reform and Employment Rights Act 1993 (which gave trade unions a duty to inform employers of upcoming strikes).

This would appear to have given my first employers everything they could have wanted in terms of containing union power but, after some retrenchment in the 1990s owing to the incoming Labour Government taking the UK back into the Social Chapter of the Maastricht Treaty (which we had originally opted out of in 1992) in 1997, there was further legislation in the form of the Trade Union Act of 2016, which, amongst other measures:

introduced a new requirement of 50% of union members to vote in a ballot for strike action;

required that workers in important services (health, school education, fire, transport, nuclear decommissioning and border security) must gain at least 40% support of those entitled to vote in a workplace for a strike to be legal;

required two weeks’ notice of industrial action to be given to an employer (the employer can agree to one week);

limited the right to take industrial action after a strike ballot to six months, or nine months if the employer agrees.

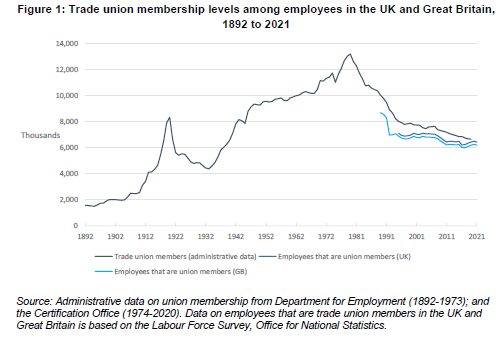

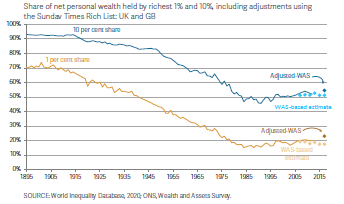

Over the period since 1985, wealth inequality, which had been steadily reducing since at least the end of World War I stalled and has been generally on a slightly increasing trend since:

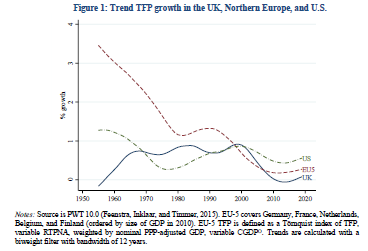

However, perhaps this was a price worth paying, if the forces of creativity and entrepreneurship had at last been allowed full rein, freed from the stifling dead hand of union power? Unfortunately not (TFP stands for total factor productivity in the graph below):

So whatever, the continuing problems of UK PLC, it does not look like union power was ever really one of the major ones. Undeterred, the Government is proposing further restrictions on trade unions and their members, including enforcing minimum service levels during strike action for ambulance staff, firefighters and railway workers and requiring some employees to work during a strike under threat of being sacked if they refuse.

The TUC has made a submission to the International Labour Organisation of the United Nations over what it sees as breaches of Conventions 87 (Freedom of Association and Protection of the Right to Organise) and 98 (Right to Organise and Collective Bargaining). As David Allen Green has blogged:

But regardless of your view on the ultimate rights and wrongs of strikes by public sector and other public service workers, there is something fundamentally objectionable in the current government’s proposals to compel certain “key” workers to attend work when they otherwise would be entitled to strike….Simply prohibiting other key workers from being able to strike, without sufficient alternative entitlements and arrangements to balance this loss of a right, is misconceived and illiberal.

It is an authoritarian gesture, rather than a solution to a problem.

Roy Lilley (at the Institute of Health and Social Care Management) in a postscript to a recent blog, focused on what a strategic failure the proposals represent within the NHS industrial dispute:

HMG plans, to ban strike action by some public workers is a further example of ‘push-back’ management. Push the disputes into the courts instead of dealing with the root-cause of strike action, improve industrial relations and representation.

So what has my part been in the downfall of trade unionism to date? In my first job, other than an abortive attempt to develop a new shift pattern(!) for the security guards in the factory, I had few skirmishes with union leaders compared to those with my management colleagues. In the finance sector, where I spent most of the middle 20 years of my working life, I rarely came across any staff representation at all. As a school teacher I joined the ATL rather than the NUT (they have since merged to form the National Education Union) due to its reputation for being determinedly non-militant. And, in my current role, I rather flounced out of the UCU over a difference of opinion over the pensions dispute raging at the time.

So I have not been a very good supporter of trade unionism over the years. However it now seems clear to me that the industrial austerity (ie the crushing of labour power within the economy, further discussed here) described above during my lifetime has been a political rather than an economic project all along. None of the economic justifications given for it since the 1980s have been borne out and the unopposed rugby of industrial management we have increasingly witnessed since has resulted, in my view, in poorer outcomes than if the 99% had been consulted regularly.

I sense that the current Government will only be satisfied when trade union membership levels fall to zero. So if, like me, you don’t want that to happen, the time to push back against running the economy at all times exclusively in the interests of the owners of capital is now.

Photo from the Climate Strike and march in Pittsburgh on 9/24/21. Link from: https://www.flickr.com/photos/9602574@N02/51512352257/. Photo taken by Mark Dixon(https://www.flickr.com/people/9602574@N02). This file is licensed under the Creative CommonsAttribution 2.0 Generic license.

Mark Blyth wrote a great book about how it was a dangerous idea; Simon Wren Lewis described it as a con; Stephanie Kelton defined it as the “deliberate infliction of harm upon society in the presence of alternatives”; Frances Coppola wrote about its terrible price; Steve Keen described it as naive; Mariana Mazzucato, Robert Skidelsky, Ann Pettifor, David Blanchflower and others wrote in the New Statesman on why the UK should not impose it in response to higher debt following the pandemic; and Richard Murphy gave the possible reasons for imposing it as “ignorance, dogmatism and spite”.

What are all of these economists talking about? Austerity. And nearly all of the criticism thrown at this “dangerous” idea is that it does not work economically (ie it will not bring down government debt levels or boost economic growth, the usual justifications given for pursuing it): a criticism for which there is a large and ever growing data set in support.

Now there are any number of Four Yorkshiremen out there to say that this thing we’re calling austerity is luxury and that we are all snowflakes to complain about it, so let’s be clear about what is meant here. Clara Mattei, in her excellent new bookThe Capital Order, describes the three forms of austerity policies: fiscal, monetary and industrial, usually used in combination. Fiscal austerity (reducing public spending, particularly on health, education and benefits and increasing the burden of taxation) and monetary austerity (reductions in the money supply and increases in interest rates) are familiar to most of us and normally the only elements of austerity discussed in the media. To these Mattei adds the idea of industrial austerity, which includes (often described as supply side policies, with the connotation of getting the economy fit to compete in world markets) policies aimed at reducing the negotiating power of workers, from anti-union legislation, to reductions in unemployment benefits, minimum wage levels and wage levels and job security within the public sector.

The contention of The Capital Order is that the reason that austerity has been used again and again in the last 100 years, despite repeatedly failing to achieve the economic goals used to justify it, is that its goals have not been economic but political. The political goal of austerity policies is to defend capitalism whenever events make it seem likely that people will look for alternatives (think World War I or the socialism following World War II or the 2008 crash, or now, the pandemic). Whenever government intervention in the economy has been needed on a sufficient scale to demonstrate that economies can strike a different balance between capital accumulation and labour power, austerity has been brought out immediately afterwards to put labour power back in its box, by making nearly everyone too poor, too busy and too regulated to be able to protest about it.

If this premise is accepted, and I think Mattei makes a convincing case in her analysis of post-World War I austerity policies in Italy and the UK, then the implications are profound. Rather than repeated wrong-headed economic policies by people who do not understand economics, we would instead have deliberate political policies by people who completely understand what they are trying to achieve by them.

The other part of the strategy, via the first international financial conferences in Brussels and then Genoa, in 1920 and 1922 respectively, was to establish an international consensus for policies where “individuals had to work harder, consume less, expect less from the government as a social actor, and renounce any from of labour action that would impede the flow of production.” Lord Chalmers, former permanent secretary at the UK Treasury, summarised this approach as: “work hard, live hard, save hard”. The aim was to return to a pre World War I economic orthodoxy and therefore remove what would be very painful economic measures for most people from the political sphere and into the sphere of “economic science”.

A quotation from the League of Nations in 1920 sums up the how important it was that such a consensus be achieved, to make it extremely difficult for any country to stand against it:

This principle must be clearly brought home to the peoples of all countries; for it will be impossible otherwise to arouse them from a dream of false hopes and illusions to the recognition of hard facts.

These “hard facts” then become the justification for sticking with economic policies, however discredited they might be economically, and buttress them: against alternative economic views (the effective shutdown of the New Approaches to Economic Challenges (NAEC) unit of the OECD being the most recent high profile example) and against popular pressure to change course (eg through such measures as central bank independence from government control over monetary austerity or proposed legislation to limit the scope of political protest).

And of course this effective outlawing of alternative schools of economic thought has other implications too. For example, as Steve Keen has shown, the potential impact of climate change in economic models to date has been disastrously underestimated, allowing fossil fuel lobbyists to delay climate action as a result.

We have all three types of austerity in play at the moment in the UK: monetary, fiscal and industrial. We can either believe that this is designed to force our compliance with the mantra to “work hard, live hard, save hard” even if we do not want to, or that it is for the economic reasons given. The former option requires us to believe that the elites in nearly every government in the world are committed to defending capitalism at all costs and that, if we want to contest this, we will have the political battle of our lives on our hands with the odds steadily more stacked against us with every new piece of legislation passed; the latter requires us to believe that our governments are economically ignorant, dogmatic and spiteful. All our current problems and our solutions to them: from the economic crisis, to the ecological crisis and the increasing political crises globally (what Adam Tooze calls the polycrisis) – depend on what we decide to believe.

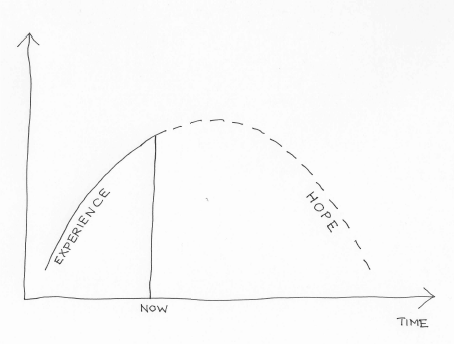

There is a particular variety of We Know Zero graphs that look like this one – showing an experience of a steady increase in something (usually bad, but not always) up until now, followed by a projection of that thing falling in the future. My wife Marsha suggested I call them Hope-over-Experience graphs, which seems to suit them very well.

Such diagrams are often very comforting for those who want to maintain the status quo. Let’s look at three such curves in particular (the excellent Doughnut Economics by Kate Raworth has alerted me to the first two of these).

The Kuznets Curve

There is a considerable body of evidence, most notably from Kate Pickett and Richard Wilkinson, that inequality impacts most health and social problems adversely, to the detriment of all socio-economic groups, but what is to be done about it? Enter our first Hope-over-Experience graph. In this case the x-axis is actually income per capita, but to the extent that this is something expected to increase with time I don’t think this matters too much. The y-axis is inequality. It was originally proposed by Simon Kuznets (the inventor of GDP) in his 1955 paper Economic Growth and Income Inequality (my apologies, but you will need journal access to read this) based on data from England, Germany and the United States from 1875 onwards, and the belief that economic growth will automatically deal with inequality has been a powerful influence on economic policy at the World Bank and elsewhere since.

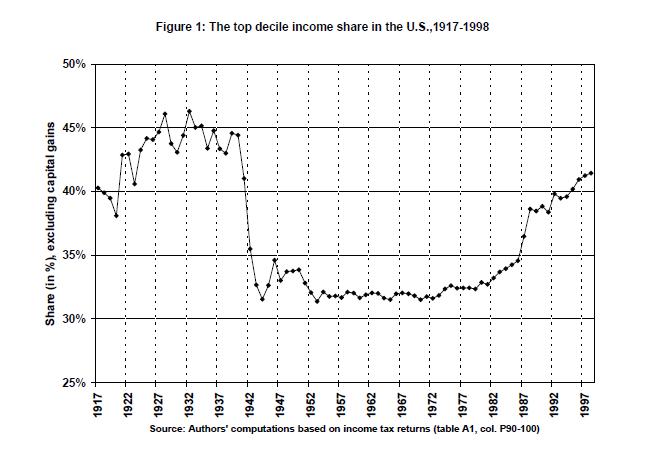

However, more recent data has shown the patterns suggested by this limited original data set are no longer correct, if indeed they ever were. Thomas Piketty and Emmanuel Saez, in their 2001 paper Income Inequality in the United States 1913-1998, state:

In particular, the evidence presented in this paper, together with the evidence on France by Piketty (2001a, 2001b) and the U.K. by Atkinson (2001), strongly suggest that there was no such thing as a “spontaneous”, Kuznets-like decline of inequality in developed countries during the first half of the 20th century. The inequality decline was to a large extent accidental (depression, inflation, wars) and amplified by political factors (progressive taxation). This does not mean that the current rise of inequality will not be followed by a mechanical downturn during the first few decades of the 21st century: this is simply saying that such a mechanical downturn apparently never occurred in the past.

Their data suggests a curve which looks like this instead:

The Environmental Kuznets Curve

This was first proposed by Gene Grossman and Alan Krueger in 1994 in their working paper Economic Growth and the Environment, which suggested that there was an eventual inverse relationship between pollution and income per capita, with a turning point mooted at around $8,000. Most of their graphs are not quite as U-shaped as the Kuznets Curve, but this nonetheless has come to be known as the Environmental Kuznets Curve.

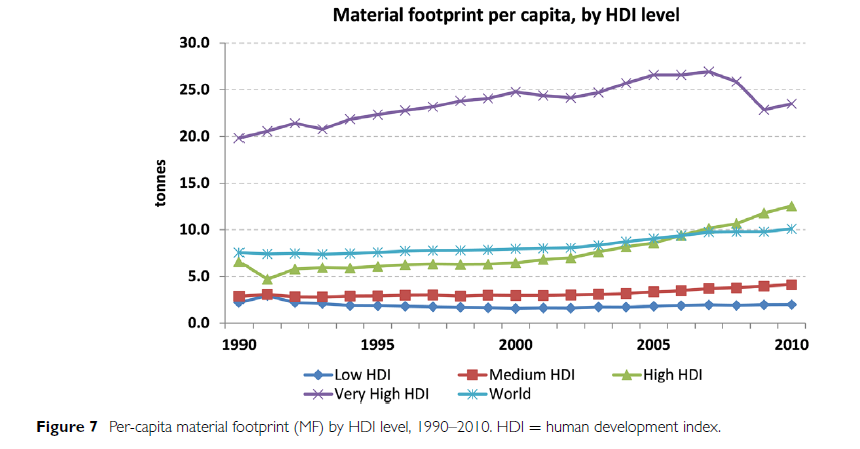

However, in 2016, the international industrial ecology research community and United Nations Environment agreed on a comprehensive data set for global material extraction and trade covering 40 years of global economic activity and natural resource use, which led to several papers including the UNEP Global Material Flows and Resource Productivity: A Report of the International Resource Panel (again apologies but journal access needed). Their graph of material extraction instead looked like this:

The Human Development Index (HDI) is the geometric average of 3 indices: Gross National Income, Health and Education. An optimum score of 1 is achieved where life expectancy is 85 or more years, adult literacy is 100%, school enrolment is 100% and the Gross National Income is US$40 000 or more per person per year in purchasing power parity. So again, this is not very supportive of a reduction in material footprint with increased wealth.

Which brings us to the third graph, often cited as an argument for why one of the most obvious ways to reduce inequality rather than just focusing on average income per capita, ie make taxation more progressive, is pointless.

The Laffer Curve

The story of the Laffer Curve, dating from the 1970s, is recounted by Arthur Laffer himself here. It plots tax rates against tax revenues to indicate that there is a tax rate beyond which tax revenues actually reduce. As he says:

The Laffer Curve itself does not say whether a tax cut will raise or lower revenues. Revenue responses to a tax rate change will depend upon the tax system in place, the time period being considered, the ease of movement into underground activities, the level of tax rates already in place, the prevalence of legal and accounting-driven tax loopholes, and the proclivities of the productive factors. If the existing tax rate is too high…then a tax-rate cut would result in increased tax revenues. The economic effect of the tax cut would outweigh the arithmetic effect of the tax cut.

However, returning to Piketty, this time in the 2011 paper, Optimal Taxation of Top Labor Incomes: A Tale of Three Elasticities by Piketty, Saez and Stefanie Stantcheva, the evidence underpinning this curve is again highly questionable. As they point out in the abstract (bold type added by me):

This paper presents a model of optimal labor income taxation where top incomes respond to marginal tax rates through three channels: (1) standard labor supply, (2) tax avoidance, (3) compensation bargaining…The macro-evidence from 18 OECD countries shows that there is a strong negative correlation between top tax rates and top 1% income shares since 1960, implying that the overall elasticity is large. However, top income share increases have not translated into higher economic growth. US CEO pay evidence shows that pay for luck is quantitatively more important when top tax rates are low. International CEO pay evidence shows that CEO pay is strongly negatively correlated with top tax rates even controlling for firm characteristics and performance, and this correlation is stronger in firms with poor governance. All those results suggest that bargaining effects play a role in the link between top incomes and top tax rates implying that optimal top tax rates could be higher than commonly assumed.

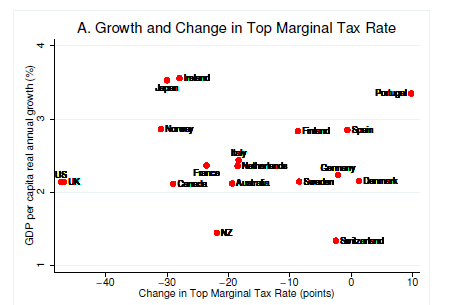

There are a number of charts which could be used from this paper, but I have chosen the plot of economic growth against changes in top marginal tax rate to illustrate most clearly the problems with the Laffer Curve idea:

This graph should show an inverse relationship if the Laffer Curve were true.

Why do I feel the need to debunk these simple so-called economic laws which are nothing of the sort? Because you will always prioritise economic growth over everything else if you believe that:

Growth will fix inequality;

Growth will fix pollution;

Trying to fix inequality through the tax system is counter-productive.

And these beliefs will then also have policy implications when faced with a different sort of curve.

This was an explainer from Grant Sanderson at 3Blue1Brown about COVID-19 from March 2020 setting out quite simply how it was likely to spread, and how different case numbers in different countries (eg between Italy and the UK) were as likely to be due to being at different time points since the start of the pandemic as reflecting the relative success of their containment policies. We now know the UK Government locked down too late, at least partly because they prioritised economic growth over containment policies in the first few weeks:

Those attitudes changed and we have had an incredibly successful vaccine rollout in the UK, but this has been at the expense of any idea of international cooperation in vaccine supply. Wealthy countries such as the UK have bought enough vaccinations to cover our populations almost three times over, while Covax, the global vaccine procurement scheme, only aims to vaccinate 20% of the populations of recipient countries this year.

This is very short-sighted if we think there might be an international issue even more threatening to life than COVID-19 which can only be combatted by unprecedented levels of international cooperation. And of course this is exactly what we have in the form of the climate emergency and our final graph (from the National Oceanic and Atmospheric Administration (NOAA) in the US showing the relentless rise in the level of carbon dioxide in the atmosphere as global emissions continue to increase:

Living in Hope-over-Experience may be very comfortable for some people for a limited time, but if it stops us engaging with the more implacable curves of the world we actually live in then none of us will be safe.

I have written about school qualifications once before here in 2014, when I was criticising the move to adding an A* grade at GCSE and the consequent narrowing of the grade boundaries to mimic the A-level ones. We have of course since moved to a numerical grade system for GCSEs which is even narrower. However, if the exam grade system was a bad way to assess students, the algorithm which replaced it in the summer (explained here and critiqued here) was clearly worse still.

So, against a background of steadily less reliable grade information at both GCSE and A-level, it was interesting to look at the Institute and Faculty of Actuaries’ (IFoA’s) employer directory and note that, of the 25 separate adverts for graduate roles, 11 of them have an A-level or UCAS points requirement in addition to the university degree requirement. My question is why?

I understand that employers, particularly this year, are likely to have very large numbers of applicants and need some way of reducing the number they need to review in detail, but there are many much better sieves than A-levels these days. Psychometric tests can assess how rusty students’ numeracy is. Application forms can be digital and given a computerised first pass on any number of criteria and, if the questions are constructed thoughtfully, will give companies a smaller set of applicants much more closely aligned to their goals than the grade given at mathematics A-level.

Even if you accept the grades as representative, there are clearly issues around social mobility and widening participation from relying on them to exclude a large number of candidates initially, which was highlighted when an algorithm attempted to reproduce the results based on subject studied and school attended. The news today that they will not be trying this again this summer is encouraging, but even if mark allocations are fairer, many problems with A-levels remain.

I have felt that this has been a growing issue for some time – it has always seemed to me ridiculous that a student on my programme (the BSc Mathematics and Actuarial Science at the University of Leicester – a qualification accredited by the IFoA), doing well and on track for all 6 of the core principles exemptions available as a result, still feels the need to retake an A level taken before they had discovered the motivation for actuarial work that they now have, in order to have a chance with many of the top employers. Are those employers so lacking in confidence in the integrity of their own profession’s qualification system that they need the security backstop of an A-level pass?

It is likely to be a tough environment for young people attempting to start their careers this year, whatever their skill set. I hope employers will review their current approach to recruitment and check they are not inadvertently pulling up the ladder before seeing all of the talent available.

NASA, ESA, and the Hubble Heritage Team (STScI/AURA), Public domain, via Wikimedia Commons

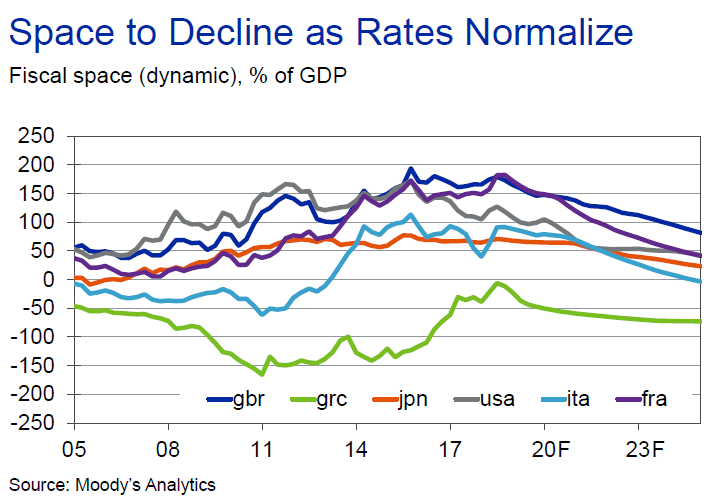

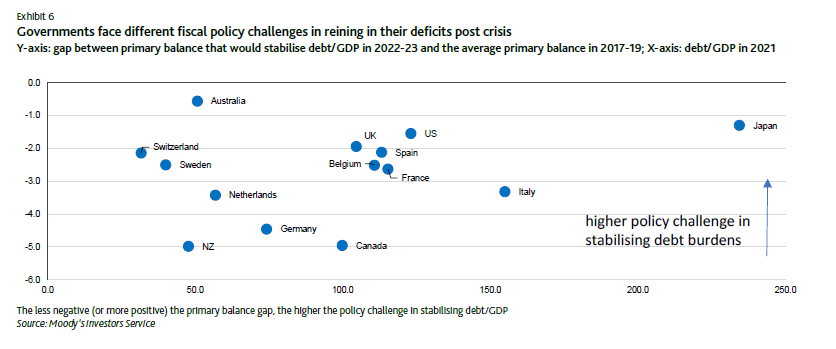

Fiscal space is defined as the difference between a nation’s sovereign debt-to-GDP ratio and the limit beyond which the nation will default unless policymakers take fiscal steps that are outside of anything they have done historically. That limit is sometimes referred to as the fiscal cliff, just to ram home the imagery of fixed physical limits beyond which disaster beckons.

How much fiscal space does the UK have? Moody’s have an answer, which depends most heavily on when you ask the question. In September 2019 it was as follows:

This shows the UK with a fiscal space (the “dynamic” means they assume interest rates increase as borrowing does, due to “crowding out” arguments – ie government borrowing pushing up the price of borrowing for everyone – so beloved of most economists) of around 175% of GDP, with this then projected to fall over the following 5 years as rates “normalized”. While the cost of borrowing seems to be dynamic, the actual borrowing itself is not allowed to be in these calculations – it is assumed that they just add to debt without increasing the revenue components of the primary balance.

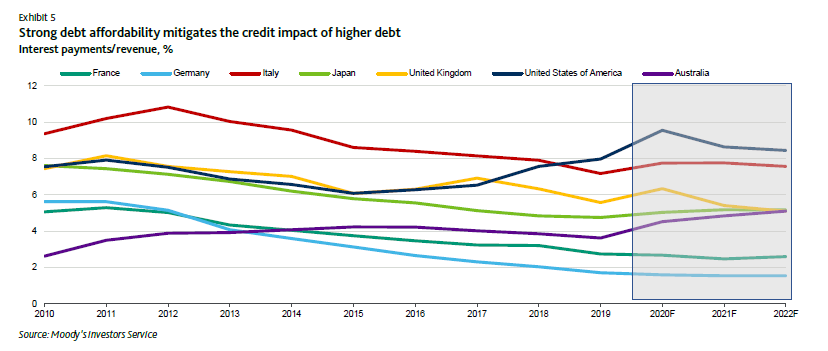

Well of course then we had 2020, at which point (June 2020) Moody’s appear to have stopped talking about fiscal space and instead are now focusing on something called “debt affordability”. What happened to dynamism and crowding out? Not explained:

However despite this triumph of debt affordability, they then produce another graph to indicate that governments still need to be bearing down on debt to GDP ratios:

As they say in the document “rating implications will depend on governments’ ability to reverse debt trajectories ahead of potential future shocks”. Remember this was in June 2020. Let’s also remind ourselves of another graph:

Requiring governments to reverse debt trajectories in this environment is insane and likely to result in more deaths if not ignored. However as recently as last month in their issuer comment for the UK they said:

However, compared to the government’s March budget (that was quickly overtaken by events), there are some initial signs that fiscal policy outside of investment is likely to be less expansive than previously announced. What remains unclear is whether this ambition will be able to withstand the political pressures that seem to be inevitable given the government’s previous commitments. Even before the Spending Review, longer-term spending commitments for health, education, and defence had already been announced. Together, these three areas account for around 60% of total expenditure.

I have been hard on Moody’s in this piece, they are most certainly not alone. But this attempt to divorce sovereign debt levels from what is actually going on in countries needs to stop as does the constant discounting of the value of any government spending at all. Political pressures to spend more on health and education are not always things that governments need to “withstand” in order to look good in a Moody’s graph. There are far more important things at stake.

I am just at the start of exploring the Green New Deal (GND), how it might work in the UK and its implications for the economy more generally. I have decided to start in an area I know a little bit about, namely education and skills, but three charts have stood out for me already in suggesting that a number of seemingly unrelated current problems may have very related solutions.

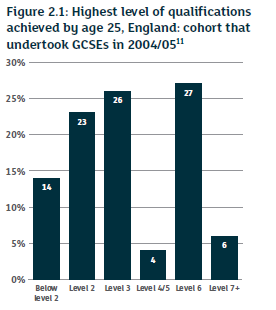

The first comes from the Augar Review into post 18 education and funding. The discussion around this when it came out in May 2019 was predominantly on the recommendations concerning increased funding for FE colleges and changes to the funding arrangements for universities. However there was a lot more to the Review than this and this chart was the most striking for me.

As you can see we hardly have any Level 4/5 as the highest level of qualification in England. What is Level 4/5? Well Level 3 means A levels, a BTEC Diploma or a craft qualification. Level 6 means a degree. In between are Levels 4 and 5. Level 5 is Foundation degrees, Higher National Diplomas (HNDs), Diplomas of Higher Education (DipHEs) and Level 4 is Higher National Certificates (HNCs), full Accounting Technician qualifications, etc.

As the Review says (my highlights in bold):

In England, only 4 per cent of 25 year-olds hold a Level 4 or Level 5 qualification as their highest level, compared to nearly 30 per cent for both Level 3 and Level 6. In contrast, in Germany, Level 4 and 5 makes up 20 per cent of all higher education enrolments.

Those few who do obtain a Level 4 or 5 award – often by a rather circuitous route – move into well-paid skilled jobs; the median annual income of someone with a Level 4 or 5 is around £2,000 higher than someone with a Level 3 by the age of 26 and comparable to the earnings of some graduates. Similarly…Level 3 apprenticeships in the skilled trades and engineering are very highly valued by employers – indeed in the latter case, for men at age 28, more than some Level 6 degrees. However…apprenticeship in England has in recent years been concentrated at lower levels (typically Level 2) than is common in the rest of Europe. Skill shortages in contrast are most evident at Levels 3 and above.

Employers have dealt with some skills shortages (for example in construction) by hiring recent immigrants with the relevant skills. They have also responded to the lack of Level 4 or 5 qualified applicants by taking on graduates as technicians, although without the relevant practical training graduates are often actually under-skilled for such roles and tend to leave quickly.

England’s education and training system currently stands in the way of taking on technician apprentices in emerging and small sectors. With no central mechanism for ensuring coverage, some employers have told us that it is often hard to identify colleges or other training providers willing to provide the necessary education and training. Providers will only do so if they are assured of a critical mass of apprentices, since otherwise the training is financially non-viable – especially if it requires expensive equipment.

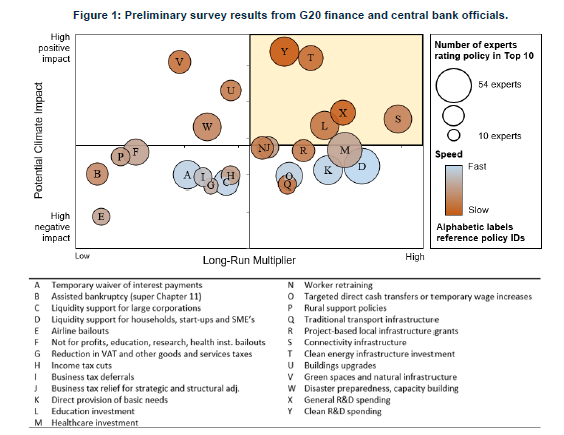

The second chart or diagram comes from the paper called A net-zero emissions economic recovery from COVID-19 from the Oxford Smith School. This looks at the potential impact on reducing carbon emissions on the vertical axis and the long run multiplier (ie the increase in national income as a result of a stimulus to the economy). The obvious things to concentrate on in such a chart are those in the top right quadrant, ie high impact both environmentally and economically. The five areas unambiguously in this quadrant are Y (Clean research and development (R&D) spending), T (Clean energy infrastructure investment – ie alternatives to fossil fuels), S (Connectivity infrastructure, particularly broadband), X (General R&D spending) and L (Education investment).

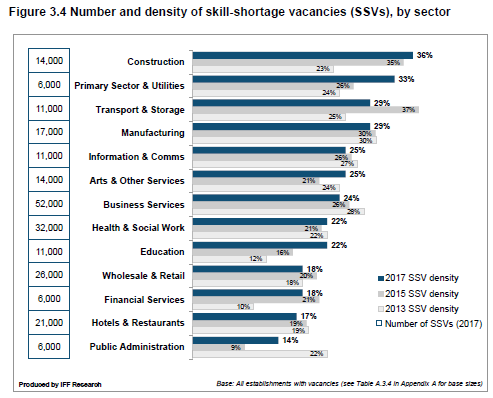

And the final chart comes from the employer skills survey 2017 from the Department for Education in August 2018 (the latest one to emerge so far). This shows the vacancies due to there being insufficient people with the appropriate skills to fill them.

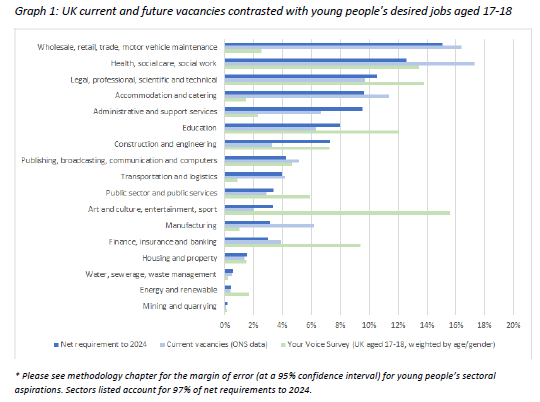

This should perhaps be considered in conjunction with the following very interesting comparison between the sectors where jobs are available and those where 17-18 year old typically would prefer to work (from Disconnected: Career aspirations and jobs in the UK by Chambers et al):

And this is before the big increases in skilled technicians in skilled trades, and in both scientific and technical areas and professional and managerial areas that a GND will require, coupled with the transformation of our economy as a result of the fourth industrial revolution that appears to be anticipated, at least in part, by the 17-18 year olds answering the survey. As the 2020 Progress Report to Parliament from the Committee on Climate Change on Reducing UK Emissions from last month says:

There are clear economic, social, and environmental benefits from immediate expansion of the following measures (again, my highlights in bold):

Investments in low-carbon and climate-resilient infrastructure.

Support for reskilling, retraining and research for a net-zero, climate-resilient economy.

Upgrades to our homes and other buildings ensuring they are fit for the future.

Action to make it easy for people to walk, cycle, and work remotely.

Tree planting, peatland restoration, green spaces and other green infrastructure.

Three different problems, all with a major part of their solution in the reconfiguration of our further and higher education systems to skill and reskill, train and retrain, the generations we are relying on to secure all our futures. It looks like a good place to start!

CPD doesn’t have to feel like this: a youthful man-o’-warsman, from the diary of an English lad who served in the British frigate Macedonian during her memorable action with the American frigate United States; who afterward deserted. Source: https://www.flickr.com/photos/internetarchivebookimages/14594689439/

According to Daniel and Richard Susskind’s the Future of the Professions, there is a Grand Bargain between society and the professions, which means (and I am paraphrasing a little here), in return for professions providing:

Expertise, experience and judgement;

Delivered affordably, accessibly, reassuringly and reliably;

With knowledge and methods maintained and kept up to date, members trained, standards and quality of work enforced and only appropriately qualified individuals allowed in;

Acting honestly and in good faith; and

Putting clients interests ahead of their own.

Society will give the professions:

Respect and status;

Exclusive rights to perform/provide socially significant activities or services; and

Independence to decide how they do it and how much they can be paid for it.

It is with regard to the knowledge and methods point above that nearly all professions have some sort of continuing professional development (CPD) requirement. The Institute and Faculty of Actuaries (IFoA) consultation on their proposed new CPD scheme is currently open and runs until 17 April. I will be responding to it via the online questionnaire, but thought it might be worth airing a few points more widely too, to promote some discussion just in case anyone has any bandwidth for anything not directly corona-related at the moment.

Overall I think this is a move very definitely in the right direction. I have some criticisms, which I will come to, but I very much welcome:

the broadening of the scope of CPD activities. I am clearly not the only one who has experienced a talk or discussion or even an arts event about which I would have said, in the words of Walter Scott: One hour of life, crowded to the full with glorious action, and filled with noble risks, is worth whole years of those mean observances of paltry decorum, in which men steal through existence, like sluggish waters through a marsh, without either honour or observation. And yet would have been unable to record it in my CPD because there was no other actuary present and no way of proving I was there!

the introduction of reflective practice discussions. There are few details about how these will work and who will run them (the suggestion I took from the consultation was that they would be centrally run, which I think would be a mistake for reasons I will explain below). However in principle this is a great idea, getting people together to talk about what they are doing to develop their thinking in important areas and sharing their experiences on how the journey is going. I am not aware of any other profession moving in this direction currently, but I very much welcome it.

The removal of the need to be audited annually on CPD recorded. The 2018 Annual Report of the Disciplinary Board of the Institute and Faculty of Actuaries indicates that there were 2 cases of non-compliance with CPD referred to them and 3 cases of failure to hold a practising certificate. The current system therefore does bring the words sledgehammer and nut to mind.

However I do also have some criticisms:

there is much made of how they are proposing to prescribe a single requirement for all members. I found it difficult to answer whether I agreed or disagreed with this proposal as I didn’t feel that they had: people who work for firms who have signed up to the profession’s Quality Assurance Scheme (QAS), practising certificate holders, Practising Members (we will come to these), Non-Practising Members and students all have different rules applying to them. My concern here is that this 5 tier system will translate into inequalities of status within the profession, and some members having a louder voice than others.

keeping students (completely outside the CPD system via the Personal and Professional Development (PPD) scheme) and QAS members completely dependent upon their firms for professional development risks, in my view, narrowing the development undertaken rather than the broadening that the proposals overall intend.

I am very concerned about the examples given to clarify what is meant by a Non-Practising Member: retired from actuarial practice; not carrying out technical actuarial work; or on a career break. As technical actuarial work is not defined in the consultation, the suspicion is that this will be the usual suspects of life, general insurance, finance and investment and pensions, with wider fields including the education field where I practise, certainly NED roles but also perhaps resources and environment work or, particularly topical at the moment, health and care. Obviously members may choose not to apply for non-practising status, but I do not believe that they should have the option to if they are using their judgement to analyse complex situations to help the people or organisations they are working with to make decisions.

currently most categories of member need to complete 2 hours annually of Professional Skills Training (PST). The materials provided by the profession to support members in complying with this requirement are extensive and excellent, but there are a wide range of ways in which it is currently met, from company events to regional community events to individuals registering the video and other content they have interacted with online. In my view this allows members to tailor what they think they need in a given year and, as a provider of these sessions for a number of years now, I have been impressed by the open and frank discussions which have become possible with our attendees on difficult questions involving potential reputational risk. My main concern with the proposals on this are that members will not feel the need to subject themselves to these sessions if the professional skills requirements are to be relaxed as far as just a learning outcome related to managing professional ethical challenges.

I am enthusiastic about the replacement of the audit of CPD records with an invitation to a reflective practice session instead, however I would be concerned if these were all centrally controlled, as opposed to the wide range of current providers for PST. I well remember sitting in professionalism CPD sessions run by senior members of the IFoA in a room full of other scheme actuaries and none of us prepared to admit to making any mistakes in our client work in front of each other. It would be regrettable if these sessions became formalised to the point that they were no longer useful.

my final point is that, if we are moving from a strictly audited system to one which will be much more light touch, perhaps this is also an opportunity to increase the hours from the current 30 hours for practising certificate holders and 15 for nearly everyone else. Doing a quick check I found that the Society of Actuaries requires 50 hours over 2 years; and the General Medical Council requires 250 hours over 5 years. At the other end of the scale, the Institute of Chartered Accounts in England and Wales (ICAEW) and the Law Society have no specific requirements at all. The ICAEW, hilariously in my view, includes the following in its guidance: There is no requirement to achieve a certain number of hours or points, and the notion of structured and unstructured activities no longer exists. There is no requirement to attend a certain number of courses or seminars. There may be periods when, having reflected, you quite reasonably conclude that you already have all the current skills and knowledge necessary for your work and that you do not need to undertake any further CPD activity at that moment. However, if we believe, as I do, that our work has never been so technical nor demanded a wider range of skills, many of which have not been traditionally demanded of actuaries previously, we should surely require that we move closer to the top of this range.

CPD has a range of uses beyond meeting the Susskind’s grand bargain:

it allows us to share our practice with each other and challenge each other;

it allows us to move between practice areas or respond to new ideas in our existing ones;

it is a means for the profession to disseminate urgent changes in expectations of members (in conjunction with the alerts which are issued occasionally);

but, perhaps most importantly, it allows us as individuals to reflect on what we are doing and the direction we are taking and consider whether we might want to change either of these.

Carefully chosen, it really can spare us a system of Scott’s mean observances of paltry decorum and instead provide more hours of glorious action!

On 23 March 2018, Universities UK (UUK), the universities’ employer body, issued an offer to the University and College Union (UCU) to end the Universities Superannuation Scheme (USS) pensions dispute. The UCU agreed to put it to their members and, on 13 April, announced that the proposals had been accepted by a margin of around 2 to 1. The main proposals, as summarised by Sally Hunt the UCU general secretary, revolved around the setting up of a Joint Expert Panel (JEP).

The JEP’s members were proposed by UUK and UCU – Ronnie Bowie, Sally Bridgeland and Chris Curry were proposed by UUK (two actuaries and the Director of the Pensions Policy Institute respectively). UCU proposed Saul Jacka (professor of statistics at the University of Warwick and a Turing fellow at the Alan Turing Institute), Deborah Mabbett (professor of public policy at Birkbeck) and Catherine Donnelly (associate professor at Heriot-Watt University, where she heads up a unit focusing on pensions, investment and insurance research). The Chair is Joanne Segars, a well respected and very experienced former CEO of the Pensions and Lifetime Savings Association (PLSA) who had most recently been working with the Local Government Pension Scheme.

The Terms of Reference of the JEP were also published, which stated that the purpose of the panel was to:

make an assessment of the 2017 valuation;

focus in particular on reviewing the basis of the scheme valuation, assumptions and associated tests; and

agree key principles to underpin the future joint approach of UUK and UCU to the valuation of the USS fund.

They also stated that the panel would take into account:

the unique nature of the HE sector, intergenerational fairness and equality considerations;

the clear wish of staff to have a guaranteed pension comparable with current provision whilst meeting the affordability challenges for all parties; and

In response to this, the USS Trustee made a proposal for concluding the 2017 valuation and preparing a 2018 valuation which could more fully take account of the JEP recommendations. This was accepted by UUK after a reduction in deficit reduction contributions from 6% to 5% was made and finally by the Pensions Regulator here, which noted that the proposal for the 2017 valuation is at the very limit of what TPR finds acceptable as it would see the Scheme carry higher levels of risk than we would consider manageable for a ‘tending to strong’ covenant.

The 2018 valuation process has been proceeding at pace, with the USS Trustee proposal following the consultation response from UUK of 3 options for future contribution patterns leading to indicative agreement from UUK for the third option of a total contribution rate of 30.7% from October 2019 and a further valuation in 2020. Following the September 2018 report, the JEP is working on a follow up report for September 2019 in relation to the USS valuation process in general. The second phase of work on the USS valuation has two parts; the first is concerned with the valuation process and governance, the second with the long-term sustainability of the scheme.

UCU have rejected all 3 options and set out a timetable for ballots on industrial action from 9 September in the event of any agreement which does not represent no detriment to members, ie no reduction in benefits or increase in employee contributions from the 8% level they were at before 1 April 2019. The JEP have suggested (while accepting that their numbers are indicative only, without detailed modelling) that, if all the measures they propose were adopted, the contribution rate could be reduced to 29.2%, split 20.1% employer and 9.1% employee in accordance with the cost sharing agreement. This compares with the USS Option 3 proposal of a split of 21.1% employer and 9.6% employee.

The UCU position looks a long way from the one that the Trustee and UUK appear to be edging towards, and I fear that a strike ballot may therefore be inevitable.

However, I think there is an equally important area mentioned in the JEP report where USS can radically improve how its members engage with a scheme which will be, for most, their major source of income in retirement.

How USS engages with its members

In their report the JEP, rightly I think, devoted several pages to member involvement in the valuation process, information and transparency and building trust and confidence, matters which will be a particular focus of their second report. They observed that:

longer consultation periods, initiated at an earlier stage, could facilitate member involvement via universities’ internal processes, which might help to build confidence in the valuation and a shared sense of ownership – helping to avoid future, damaging, industrial disputes.

there is no formal, scheme-wide mechanism for involving members in the valuation process or for assessing their appetite for changes to the Scheme

for future valuation cycles it will be important that the Trustee and Scheme Actuary interact more, at an earlier stage, with all stakeholders, particularly with regard to setting valuation assumptions and expectations

lack of understanding is likely to have contributed to falling levels of member confidence in the Scheme. It might be helpful for the Scheme to provide simple-to-understand guides which use clearly defined terminology to aid the understanding of the majority of Scheme members

the lack of trust in the valuation process and the Scheme has given rise to a view, albeit not a universal one, that USS is not being as open as it could be with stakeholders….whilst observing the need for confidentiality…the Panel suggests the Trustee may wish to consider how to share more of the information currently deemed confidential, eg on a redacted basis or in a summarised form. This would aid understanding of the valuation process…and, importantly, help rebuild confidence in the Scheme and its governance.

I would take such suggestions a step further, as I believe much of this communication would be wasted within the current adversarial environment, and indeed would be likely to be “spun” by one side or the other. It is clear that there is little trust in the USS Trustee on the part of the UCU officers. However, the ability of the 21,685 (out of 24,707 total votes) who voted to strike and then the 21,683 (out of 33,973 total votes) who voted to end the strike to determine what could or could not happen to a scheme with 396,278 members (as at 31 March 2017, 190,546 of them active) was, I think, unhelpful to the process of achieving a consensus more generally. Engagement needs to go much further than negotiations between UUK and UCU during valuation processes. USS does need to do far far more, in conjunction with the UCU and others, to engage members to help them understand their finances first before launching into what can be fairly abstract pensions discussions even for university professors.

The good news is that the membership have become much more aware of their pension scheme, mainly as a result of last year’s industrial action, and, being the inquisitive people they are, will I am sure now be looking for a higher degree of information (and education) from their pension provider about their benefit provision in future.

As the Pensions Policy Institute and many others have been saying for years, the decisions we are asking people to make are complex and subject to many different influences and biases. These decisions can be helped enormously if more care is taken in the nature and timing of how members are communicated with. Members will not value benefits they don’t understand and ultimately this scheme is only going to work in the long term if the people in it are trusted to be part of the decisions about its future.