This blog has a long history with the OBR, which I won’t go into here, although you can get a sense of it from this. It was the reason the blog is called We Know Zero. However I find myself returning to talk about them once again in the light of some of the Government’s latest spending (or removal of spending) plans.

Daniel Susskind had this to say about the role they are currently playing for the Government, to determine whether it is going the right way to achieve economic growth:

This was never meant to be the OBR’s purpose. Set up in 2010 by George Osborne, then chancellor, it was designed to solve a different problem: that the official UK public finance forecasts were not credible. The Treasury had a strong incentive to massage these numbers into better shape, whatever the political make-up of the government. And the belief was that an independent statistical authority would be free of that temptation. To that extent, the OBR is a success story: its forecasts do appear to be less biased.

At this point I need to stifle a snigger: less biased than what? I think it may not have a political reason for bias, but their methodology is like train tracks as I have maintained since this blog started in 2013: if you lay them out in a particular way then, even if you don’t want to call it bias, that is the way the train will run (to misquote Yes Minister). It may be statistically unbiased, in the same way that someone who misses a penalty past each post (I am sure that this analogy has nothing to do with my team going out of the Champions League this week) has, on average, hit the target.

However I agree with Susskind that the OBR was certainly never set up to advise on policy. As he goes on to say:

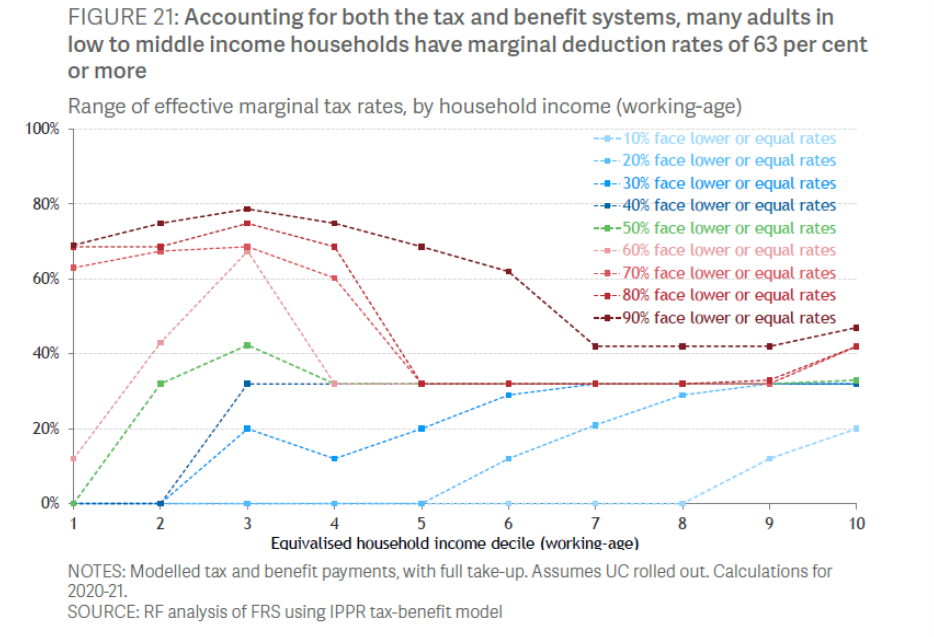

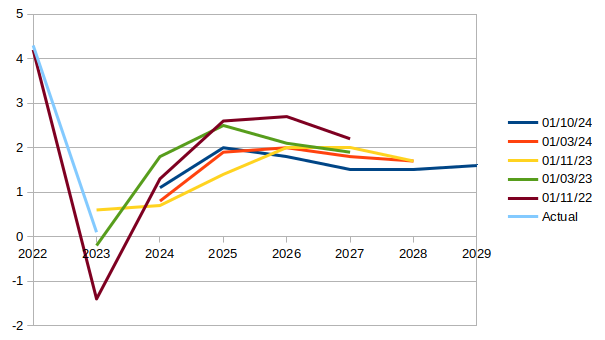

With that in mind, the idea that the OBR somehow knows enough to take each UK government policy and state its impact on growth to a single decimal point is fanciful. Yet that is what it will attempt to do at the end of the month, with immense practical consequence. A reduction of 0.1 percentage point in the OBR’s potential productivity growth forecast, for instance, is estimated to create a hole of £7bn-£8bn in the public finances — that is the equivalent of the entire budget of Defra.

Or the foreign aid budget or disability benefits or…the list looks likely to go on.

In an open letter this week, 17 major charities including Scope, Trussell Trust, Citizens Advice, Mencap, Sense, the Joseph Rowntree Foundation and the RNIB urged the Government not to cut the Personal Independence Payments (PIP) and the Limited Capability for Work payment, saying:

Scope’s analysis of government figures shows that without PIP, a further 700,000 more disabled households could be pushed into poverty. Life costs more for disabled people. Huge numbers already live in poverty as a result of these extra costs. The impact of any cuts to disability benefits would be devastating.

Meanwhile Roy Lilley looks at those cuts from the NHS end of the lens. I don’t agree with his assessment of the IFS, but there is nothing else here to argue with:

Currently, 2.9 million working-age adults are claiming disability benefits, an increase of 900,000 from pre-pandemic levels, with 500,000 attributing their main condition to mental health issues.

Lilley asks why this is, comparing the mental stress attributed to the pandemic with that of the Blitz. He then cites a study by the Tavistock Institute:

While, in the post war years, mental health issues were still stigmatised, post-war policies focused on social security and housing aimed to reduce economic stress that so often is the contributing factor to poor mental health.

We have done a lot to reduce the stigma of mental health issues, but:

I question the policies. Social and economic factors. Job insecurity and financial stress must be the key factors that have a negative impact on mental health well being.

Back to the Trussell Trust, who have been running a campaign for a while now to guarantee everyone the essentials to live on. As they say:

More than three quarters of people on Universal Credit and disability payments have already gone without essentials in the last six months.

Back to Lilley, who as I said, is primarily concerned with the NHS:

Since 2019 the NHS has experienced a 36% increase in patients seeking mental health services.

As he goes on to say:

Labour’s plan to cut benefits won’t solve the problem. It’ll very likely make it worse.

Policies cutting the root causes of people needing benefits, like safe homes and decent jobs would seem much more sensible.

Unfortunately Lilley’s “if there is one organisation worth paying attention to” IFS believe that OBR forecasts should continue to underpin the Chancellor’s spending decisions. I couldn’t disagree more.

That means constraining the Government to act as if all it knows is what the OBR knows. Which is precisely zero.