To Generation Z: a message of support from a Boomer

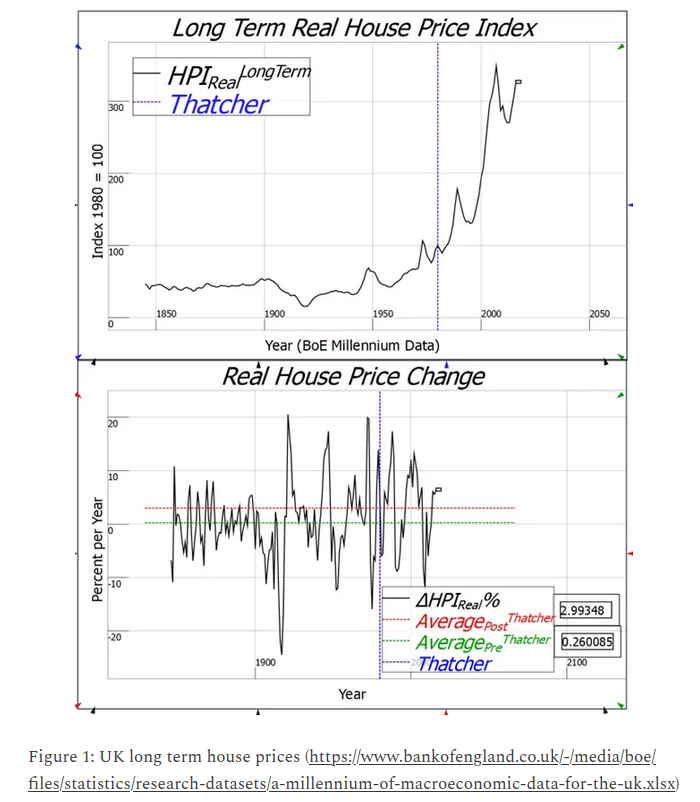

So you’ve worked your way through school and now university, developing the skills you were told would always be in high demand, credentialising yourself as a protection against the vagaries of the global economy. You may have serious doubts about ever being able to afford a house of your own, particularly if your area of work is very concentrated in London…

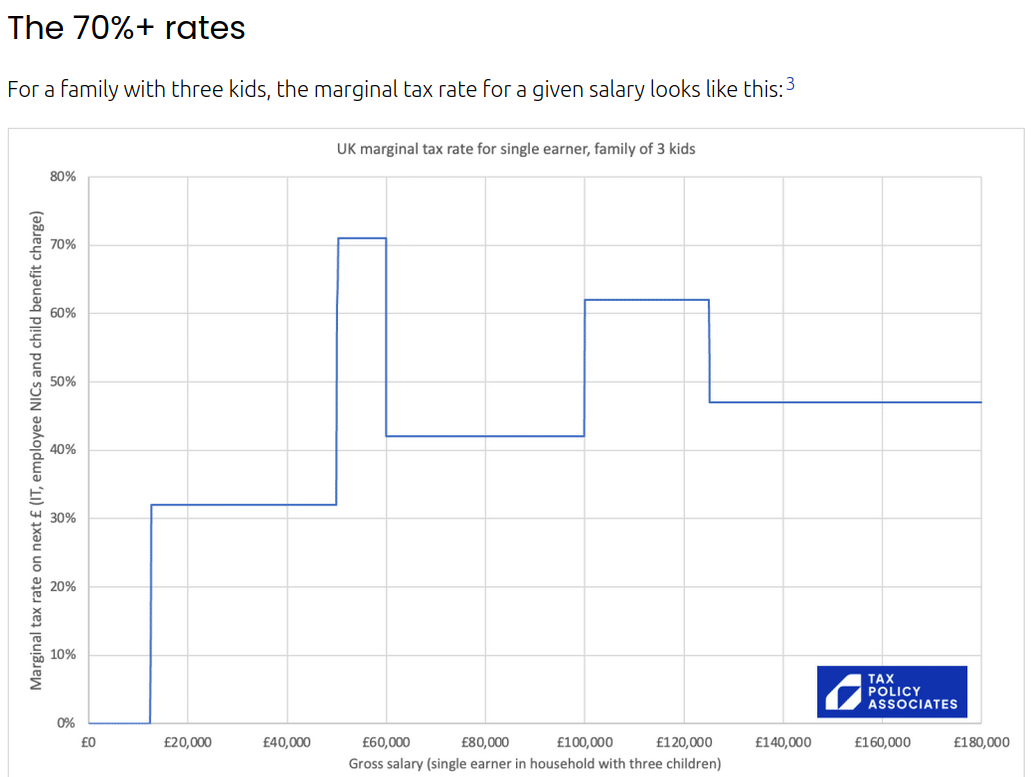

…and you resent the additional tax that your generation pays to support higher education:

But you still had belief in being able to operate successfully within the graduate market.

A rational functional graduate job market should be assessing your skills and competencies against the desired attributes of those currently performing the role and making selections accordingly. That is a system both the companies and graduates can plan for.

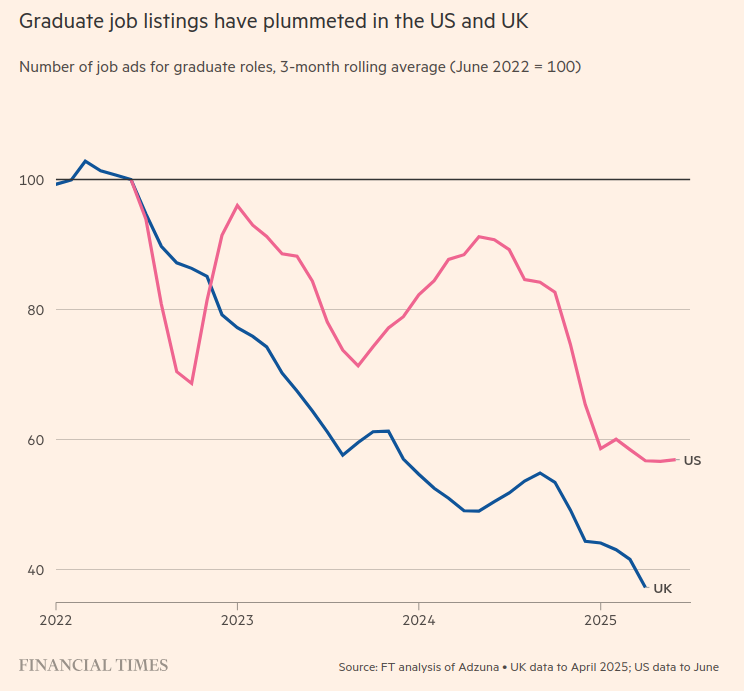

It is very different from a Rush. The first phenomenon known as a Rush was the Californian Gold Rush of 1848-55. However the capitalist phenomenon of transforming an area to facilitate intensive production probably dates from sugar production in Madeira in the 15th century. There have been many since, but all neatly described by this Punch cartoon from 1849:

A Rush is a big deal. The Californian Gold Rush resulted in the creation of California, now the 5th largest economy in the world. But when it comes to employment, a Rush is not like an orderly jobs market. As Carlo Iacono describes, in an excellent article on the characteristics of the current AI Rush:

The railway mania of the 1840s bankrupted thousands of investors and destroyed hundreds of companies. It also left Britain with a national rail network that powered a century of industrial dominance. The fibre-optic boom of the late 1990s wiped out about $5 trillion in market value across the broader dot-com crash. It also wired the world for the internet age.

A Rush is a difficult and unpredictable place to build a career, with a lot riding on dumb luck as much as any personal characteristics you might have. There is very little you can count on in a Rush. This one is even less predictable because as Carlo also points out:

When the railway bubble burst in the 1840s, the steel tracks remained. When the fibre-optic bubble burst in 2001, the “dark fibre” buried in the ground was still there, ready to carry traffic for decades. These crashes were painful, but they left behind durable infrastructure that society could repurpose.

Whereas the 40–60% of US real GDP growth in the first half of 2025 explained by investment in AI infrastructure isn’t like that:

The core assets are GPUs with short economic half-lives: in practice, they’re depreciated over ~3–5 years, and architectures are turning over faster (Hopper to Blackwell in roughly two years). Data centres filled with current-generation chips aren’t valuable, salvageable infrastructure when the bubble bursts. They’re warehouses full of rapidly depreciating silicon.

So today’s graduates are certainly going to need resilience, but that’s just what their future employers are requiring of them. They also need to build their own support structures which are going to see them through the massive disruption which is coming whether or not the enormous bet on AI is successful or not. The battle to be centaurs, rather than reverse-centaurs, as I set out in my last post (or as Carlo Iacono describes beautifully in his discussion of the legacy of the Luddites here), requires these alliances. To stop thinking of yourselves as being in competition with each other and start thinking of yourselves as being in competition for resources with my generation.

I remember when I first realised my generation (late Boomer, just before Generation X) was now making the weather. I had just sat a 304 Pensions and Other Benefits actuarial exam in London (now SP4 – unsuccessfully as it turned out), and nipped in to a matinee of Sam Mendes’ American Beauty and watched the plastic bag scene. I was 37 at the time.

My feeling is that despite our increasingly strident efforts to do so, our generation is now deservedly losing power and is trying to hang on by making reverse centaurs of your generation as a last ditch attempt to remain in control. It is like the scene in another movie, Triangle of Sadness, where the elite are swept onto a desert island and expect the servant who is the only one with survival skills in such an environment to carry on being their servant.

Don’t fall for it. My advice to young professionals is pretty much the same as it was to actuarial students last year on the launch of chartered actuary status:

If you are planning to join a profession to make a positive difference in the world, and that is in my view the best reason to do so, then you are going to have to shake a few things up along the way.

Perhaps there is a type of business you think the world is crying out for but it doesn’t know it yet because it doesn’t exist. Start one.

Perhaps there is an obvious skill set to run alongside your professional one which most of your fellow professionals haven’t realised would turbo-charge the effectiveness of both. Acquire it.

Perhaps your company has a client who noone has taken the time to put themselves in their shoes and communicate in a way they will properly understand and value. Be that person.

Or perhaps there are existing businesses who are struggling to manage their way in changing markets and need someone who can make sense of the data which is telling them this. Be that person.

All why remaining grounded in which ever community you have chosen for yourself. Be the member of your organisation or community who makes it better by being there.

None of these are reverse centaur positions. Don’t settle for anything less. This is your time.

{kind=link}