Roman Krznaric has recently written a book (History for Tomorrow) of suggestions for how we can learn useful things from history to navigate our way into the future: from how to nurture tolerance, bridge the inequality gap and revive faith in democracy to how to break fossil fuel addiction, kick consumer habits and secure water for all. In the introduction to all of this, there is a particularly arresting paragraph (perhaps particularly so for me as I was born in October 1962):

“Can history really live up to such promise as a guide in a complex world? In October 1962, in the midst of the Cuban Missile Crisis, President John F Kennedy turned for counsel to a recent work of popular history, Barbara W Tuchman’s The Guns of August, which chronicled the series of misperceptions, miscalculations and bungles by political and military leaders that had contributed to the outbreak of the First World War. Kennedy was worried that an aggressive policy response from the US might lead to a similar cascade of decisions that could provoke Soviet premier Nikita Khrushchev to push the nuclear button. ‘I am not going to follow a course which will allow anyone to write a comparable book about this time – The Missiles of October‘, the president told his brother, Attorney General Robert Kennedy. ‘If anyone is around to write after this, they are going to understand that we made every effort to find peace and every effort to give our adversary room to move’.”

Unfortunately JFK did not fully get his wish. Yes nuclear war was averted but a movie was made in 1974 with the title The Missiles of October, starring William Devane and Martin Sheen and with JFK’s brother getting a writing credit! JFK was assassinated a year after the events of October 1962 and his brother was assassinated in 1968.

Sometimes history can just put what seem like current quite extreme events into a broader context.

For instance, which US Secretary of State said of the UK:

All we needed was one regiment. The Black Watch would have done. Just one regiment, but you wouldn’t. Well don’t expect us to save you again. They can invade Sussex and we wouldn’t do a damn thing about it.

Sounds like the kind of thing JD Vance would have said at Munich, doesn’t it? But it was in fact Dean Rusk in 1964 after the UK declined to send troops to Vietnam (something I discovered from Alan Johnson’s biography of Harold Wilson). So immediately we can see that, objectionable as Vance is, Vances have happened to us in the past and we’ve survived them. If, as seems likely, we are going to be reversing many of the assumptions of globalisation over the next few years, we should perhaps expect international diplomacy to look more like the 1960s than the 2010s.

Another example, courtesy of Ed Conway. Trump’s bid to secure minerals in return for continued support of Ukraine seems extreme to us. Until we realise that FDR considered all kinds of possible things from the UK in return for the Lend-Lease deal which allowed the UK to continue fighting the Second World War.

Once we realise that some aspects of Trump’s behaviour merely belong to a period of international relations that we thought we had evolved beyond rather than being totally unprecedented, then we can understand it better and respond accordingly.

My 60th birthday celebrations, a couple of years ago now, centred around train journeys to the South of France and then onto Madrid. The highlight was (pictured above) spending a large part of my birthday, in mid October, on a huge deserted beach at Narbonne and being able to comfortably swim in the sea. So much space.

And the trains also seemed so much more spacious. I travel a lot on trains in the UK, with sometimes comedically little space. And I am not just talking about space in terms of leg room in European trains, but also whenever you want to walk over to the restaurant carriage on the upper floor of a double decker train to improve the views, with a bar and an array of kidney shaped tables dotted around the carriage to eat hot meals at, before ambling back to your seat. Mental space is much greater too, with fewer announcements and partitions between passengers to reduce the amount of conversation bouncing around the carriage. I had several 5-6 hour journeys over the two weeks I was away, and they were without exception very relaxing experiences.

So enough travelogue. What point am I making? It is the importance of space.

I think of other things where my view of it has been affected by the space attached to it. Take swimming, for example. I spent three of my formative years (aged 3 to 6) in Singapore where my father was stationed with the RAF. We swam outdoors at the Singapore Swimming Club every afternoon and lived in flats right next to a beach. Swimming was all about space – on my back staring up at the limitless sky, or mask and snorkels on and face down to explore the depths of the pools.

Back in the UK, it has never been anything like the same experience. I have swum in pools in village schools in Yorkshire, council pools in Cheltenham and Witney, the pools built for the Youth Games in Sheffield, a private school’s tiny pool in Oxford where I did my bronze survival badge. Endless school outings with compulsory swim caps and cold water. I have swum in lakes and spent probably more time in the Cherwell than was strictly healthy, sometimes deliberately, sometimes because the canoes we were given at school were designed to be manoeuvrable rather than stable. I have swum in decaying metal structures in spa towns and pools fed by spring water with no heating in the Peak District. I only discovered body boarding relatively late and the joys of doing it for much longer in colder seas with a wetsuit even later (last year). I also spent a fascinating morning with the Wild Woman of the Wye, Angela Jones, learning how to swim safely in the river in our current polluted times. And it certainly feels like the decline in swimming quality in recent years extends indoors as well as outdoors. The Wyndley or Beeches Leisure Centres near my part of Sutton Coldfield just don’t hold much appeal for me. Sure there are bodies of water there, but nothing to lift your spirit while using them and the constraints, in terms of the narrow time slots and even narrower lanes you are confined to, are the very opposite of my earliest experiences of water. I am lucky enough to be able to afford the local David Lloyd Centre, with much less pressure on their pools, in particular their excellent outdoor pool in Birmingham, which is miraculously underused. On a day with bright sun, with the birds singing and a light breeze rustling the trees just enough to drown out the industrial hum from next door and push back the smell of solvents, I can sometime almost imagine I am back in the Singapore Swimming Club.

But generally when you attempt to venture outside you find the constraints are even greater than those at Wyndley swimming pool. According to the Right to Roam campaign group we only have access to 3% of rivers in England. Meanwhile the Outdoor Swimming Society are campaigning for swimming access to reservoirs.

On land we have slightly more access, but half of the land area of England is owned by around 1% of the population. As Guy Shrubsole points out:

The aristocracy and landed gentry still own around 30% of England, whilst the country’s homeowners own just 5% of the land. The public sector owns around 8% of England; the country’s 24 non-Royal Dukes own a million acres of Britain.

I can only redistribute some space in my direction, on a train, in a pool of water, by paying more than most can afford for those experiences, and allowing me to behave like a non-Royal Duke for a short time.

This has huge implications for carbon sequestration of course, with, for example, 60% of deep peat owned by just 124 landowners. These landowners are not looking after it very well either, with upland peat being degraded as a result of moorland burning for grouse moors, and lowland peat in the Fens and elsewhere being damaged through drainage for intensive agriculture. As a result, England’s peat soils are now a net source of carbon emissions rather than a sink, leaking around 11 million tonnes of CO2 annually. The Government has committed to protecting 30% of land in the UK for nature by 2030, but is itself hugely constrained by the concentrated ownership of land.

So our land is like our swimming pools: tightly constrained by the narrow time slots and narrower lanes most of us are allowed access to. We are being stifled by the property rights of a tiny minority.

Milan Kundera wrote his The Book of Laughter and Forgetting in 1979, a few years after moving to France and the same year he had his Czech citizenship revoked. His books had all been banned in Czechoslovakia in 1968, as most of them poked fun at the regime in one way or the other. The Book of Laughter and Forgetting was no exception, focusing, via seven stories, on what we choose to forget in history, politics and our own lives. One of the themes is a word which is difficult to translate into English: litost.

Litost seems to mean an emotional state of feeling of being on your own suddenly brought face to face with how obvious your own hopelessness is. Or something to that effect. Kundera explored several aspects of litost at length in the novel. However, for all the difficulties of describing it exactly, litost feels like a useful word for our times, our politics and our economics.

I want to focus on two specific examples of forgetting and the sudden incidents of litost which have brought them back into focus.

The first, although not chronologically, would be the pandemic. There are several articles around suddenly about the lessons we have not learnt from the pandemic, to mark the fifth anniversary of the first lockdown. Christina Pagel, backed up by module 1 of the Covid-19 Inquiry, reckons:

Preventing future lockdowns requires planning, preparation, investment in public health infrastructure, and investment in testing, virology and medical research…

She takes issue with some of the commentary as follows:

But the tenor of reporting and public opinion seems to be that “lockdowns were terrible and so we must not have lockdowns again”. This is the wrong lesson. Lockdowns are terrible but so are unchecked deadly pandemics. The question should be “lockdowns were terrible, so how can we prevent the spread of a new pandemic so we never need one again?”.

However the stampede to get back to “normal” has mitigated against investing in infrastructure and led to a massive reduction in testing and reporting, and the Covid-19 Inquiry has given the government cover (all questions can just be responded to by saying that the Covid Inquiry is still looking at what happened) to actively forget it as quickly as possible. Meanwhile the final module of the Covid-19 Inquiry is not due to conclude until early 2026, which one must hope is before the next pandemic hits. For which, as the former Chief Scientific Adviser and other leading experts have said, we are not remotely prepared, and certainly no better prepared than we were in 2020.

It is tempting to think that this is the first major recent instance involving the forgetting of a crisis to the extent that its repetition would be just as devastating the second time. Which is perhaps a sign of how complete our collective amnesia about 2008 has become.

Make no mistake, 2008 was a complete meltdown of the core of our financial system. People I know who were working in banks at the time described how even the most experienced people around them had no idea what to do. Alistair Darling, Chancellor of the Exchequer at the time, claimed we were hours away from a “breakdown in law and order”.

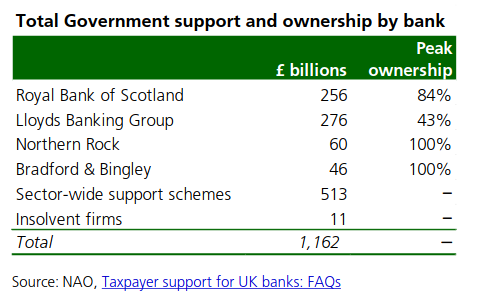

According to the Commons Library briefing note from October 2018, the Office for Budget Responsibility (OBR) estimates that, as at the end of January 2018, the interventions had cost the public £23 billion overall. The net balance is the result of a £27 billion loss on the RBS rescue, offset by some net gains on other schemes. Total support in cash and guarantees added up to almost £1.2 trillion, including the nationalisation of Northern Rock (purchased by Virgin Money, which has since been acquired by the Nationwide Building Society) and the Bradford & Bingley (sold to Santander) and major stakes in RBS (now NatWest) and Lloyds. Peak government ownership in these banks is shown below:

If you read the Bank of England wacky timeline 10 years on from 2018, you will see a lot about how prepared they are to fight the last war again. As a result of this, cover has been given to actively forget 2008 as quickly as possible.

Except now various people are arguing that the risks of the next financial crisis are increasing again. The FT reported in January on the IMF’s warnings (from their Global Financial Stability Report from April 2024) about the rise in private credit bringing systemic risks.

Meanwhile Steve Keen (one of the very few who actually predicted the 2008 crisis) in his latest work Money and Macroeconomics from First Principles, for Elon Musk and Other Engineers has a whole chapter devoted to triggering crises by reducing government debt, which makes the following point:

A serious crisis, triggered by a private debt bubble and crash, has followed every sustained attempt to reduce government debt. This can be seen by comparing data on government and private debt back to 1834.

(By the way, Steve Keen is running a webinar for the Institute and Faculty of Actuaries entitled Why actuaries need a new economics on Friday 4 April which I thoroughly recommend if you are interested)

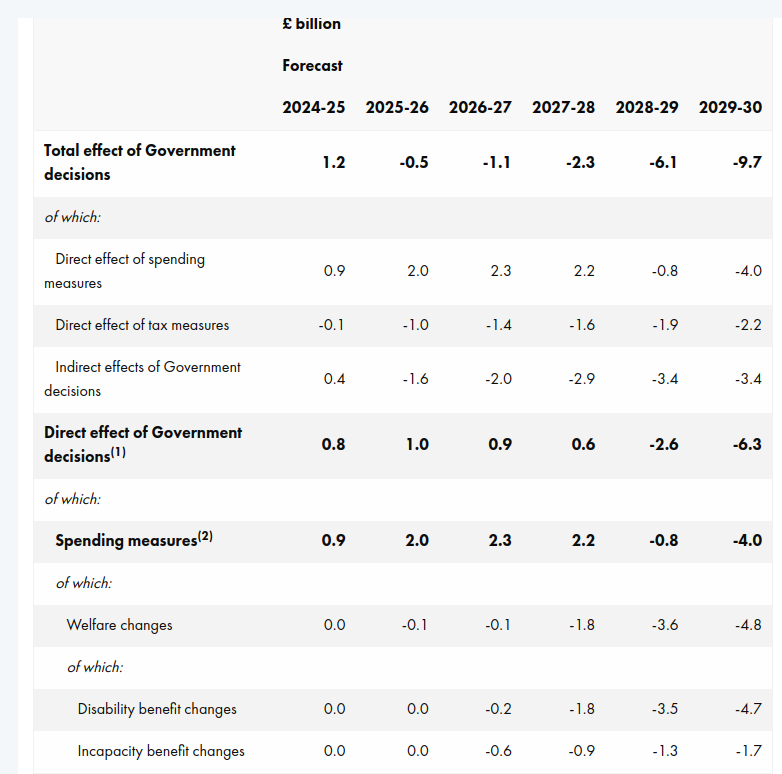

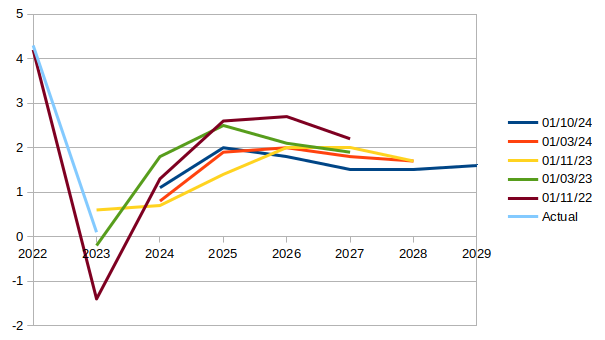

Which brings us to the Spring Statement, which was about (yes, you’ve guessed it!) reducing government debt (or the new formulation of this “increasing OBR headroom”) and boosting GDP growth. Watching the Chief Secretary to the Treasury, Darren Jones, and Paul Johnson from the IFS nodding along together in the BBC interviews immediately afterwards, you realised how the idea of allowing the OBR to set policy has taken hold. Johnson’s only complaint seemed to be that they appeared to be targeting headroom to the decimal point over other considerations.

I have already written about the insanity of making OBR forecasts the source of your hard spending limits in government. The backdrop to this Statement was already bad enough. As Citizens Advice have said, people’s financial resilience has never been lower.

But aside from the callousness of it all, it does not even make sense economically. The OBR have rewarded the government for sticking to them so closely by halving their GDP growth projections and, in the absence of any new taxes, it seems as if disabled people are being expected to do a lot of the heavy lifting by 2029-30:

Part of this is predicated on throwing 400,000 people off Personal Independence Payments (PIPs) by 2029-30. According to the FT:

About 250,000 people, including 50,000 children, will be pushed into relative poverty by the cuts, according to a government impact assessment.

We are left standing. Abandoned, to watch the idiocy of what’s lost… the security, human dignity and wellbeing of our fellow man, woman and their family… everything that matters.

As an exercise in fighting the last war, or, according to Steve Keen, the wars successive governments have been fighting since 1834, it takes some beating. It was litost on steroids for millions of people.

So what does the government think these people are going to fill the income gap with? It will be private debt of course. And for those in poverty, the terms are not good (eg New Horizons has a representative APR of 49% with rates between 9.3% APR and maximum 1,721% APR).

And for those who can currently afford a mortgage (from page 47 of the OBR report):

Average interest rates on the stock of mortgages are expected to rise from around 3.7 per cent in 2024 to a peak of 4.7 per cent in 2028, then stay around that level until the end of the forecast. The high proportion of fixed-rate mortgages (around 85 per cent) means increases in Bank Rate feed through slowly to the stock of mortgages. The Bank of England estimates around one-third of those on fixed rate mortgages have not refixed since rates started to rise in mid-2021, so the full impact of higher interest rates has not yet been passed on.

So, even before considering the future tax increases the FT appears to be expecting, the levels of private debt look like they will shoot up very quickly. And we all know (excluding the government it seems) where that leads…

I want to talk about The Future by Naomi Alderman. I read it last year, after wandering around the Hay Festival bookshop moaning that they don’t do science fiction and then coming across Naomi’s book and realising I had just missed her being interviewed. Then I watched the interview and bought both The Future and The Power (which I will talk about at some future date, but which is equally terrific).

The book is about Lenk Sketlish, CEO of the Fantail social network, Zimri Nommik, CEO of the logistics and purchasing giant Anvil, Ellen Bywater, CEO of Medlar Technologies, the world’ most profitable personal computing company, and the people working for them, and the people linked with those people. Zimri, Ellen and Lenk are at least as monstrous as Jeff, Sundar, Elon, Tim and Mark. And they are all preparing for the end of the world.

(If you need to remind yourself what Elon, Jeff, Mark and Sundar all look like milling around, below is a link to Trump’s inauguration:

Anvil is set up with alerts for signs of the end of the world being reported anywhere: giant hailstones, plague of locusts, Mpox, rain of blood which turned out to be a protest for menstrual equity involving blood-soaked tampons being thrown at Lenk and co as they emerged from a courthouse in Washington. The information Zimri, Ellen and Lenk have on everybody else in the world makes them feel all seeing, all hearing, all knowing. Combined with riches unknown to anyone before in history it makes them feel invulnerable, even to the end of the world, even to each other. Which turns out, of course, to be their decisive vulnerability.

It takes in survivalism, religious cults and wraps it all up in a thriller plot which is absolutely the kind of science fiction you want to be reading now instead of listening out for the latest antics of the horse in the hospital. And it was all written over a year before Elon even started with DOGE. The Future by Naomi Alderman is a fantastic read, particularly if you would like to see someone like Musk get an appropriate end to his story. I obviously won’t spoil it by saying what that is, but I don’t think I would be giving anything away by saying rockets are involved!

This blog has a long history with the OBR, which I won’t go into here, although you can get a sense of it from this. It was the reason the blog is called We Know Zero. However I find myself returning to talk about them once again in the light of some of the Government’s latest spending (or removal of spending) plans.

Daniel Susskind had this to say about the role they are currently playing for the Government, to determine whether it is going the right way to achieve economic growth:

This was never meant to be the OBR’s purpose. Set up in 2010 by George Osborne, then chancellor, it was designed to solve a different problem: that the official UK public finance forecasts were not credible. The Treasury had a strong incentive to massage these numbers into better shape, whatever the political make-up of the government. And the belief was that an independent statistical authority would be free of that temptation. To that extent, the OBR is a success story: its forecasts do appear to be less biased.

At this point I need to stifle a snigger: less biased than what? I think it may not have a political reason for bias, but their methodology is like train tracks as I have maintained since this blog started in 2013: if you lay them out in a particular way then, even if you don’t want to call it bias, that is the way the train will run (to misquote Yes Minister). It may be statistically unbiased, in the same way that someone who misses a penalty past each post (I am sure that this analogy has nothing to do with my team going out of the Champions League this week) has, on average, hit the target.

However I agree with Susskind that the OBR was certainly never set up to advise on policy. As he goes on to say:

With that in mind, the idea that the OBR somehow knows enough to take each UK government policy and state its impact on growth to a single decimal point is fanciful. Yet that is what it will attempt to do at the end of the month, with immense practical consequence. A reduction of 0.1 percentage point in the OBR’s potential productivity growth forecast, for instance, is estimated to create a hole of £7bn-£8bn in the public finances — that is the equivalent of the entire budget of Defra.

Or the foreign aid budget or disability benefits or…the list looks likely to go on.

In an open letter this week, 17 major charities including Scope, Trussell Trust, Citizens Advice, Mencap, Sense, the Joseph Rowntree Foundation and the RNIB urged the Government not to cut the Personal Independence Payments (PIP) and the Limited Capability for Work payment, saying:

Scope’s analysis of government figures shows that without PIP, a further 700,000 more disabled households could be pushed into poverty. Life costs more for disabled people. Huge numbers already live in poverty as a result of these extra costs. The impact of any cuts to disability benefits would be devastating.

Meanwhile Roy Lilley looks at those cuts from the NHS end of the lens. I don’t agree with his assessment of the IFS, but there is nothing else here to argue with:

Currently, 2.9 million working-age adults are claiming disability benefits, an increase of 900,000 from pre-pandemic levels, with 500,000 attributing their main condition to mental health issues.

Lilley asks why this is, comparing the mental stress attributed to the pandemic with that of the Blitz. He then cites a study by the Tavistock Institute:

While, in the post war years, mental health issues were still stigmatised, post-war policies focused on social security and housing aimed to reduce economic stress that so often is the contributing factor to poor mental health.

We have done a lot to reduce the stigma of mental health issues, but:

I question the policies. Social and economic factors. Job insecurity and financial stress must be the key factors that have a negative impact on mental health well being.

Back to the Trussell Trust, who have been running a campaign for a while now to guarantee everyone the essentials to live on. As they say:

More than three quarters of people on Universal Credit and disability payments have already gone without essentials in the last six months.

Back to Lilley, who as I said, is primarily concerned with the NHS:

Since 2019 the NHS has experienced a 36% increase in patients seeking mental health services.

As he goes on to say:

Labour’s plan to cut benefits won’t solve the problem. It’ll very likely make it worse.

Policies cutting the root causes of people needing benefits, like safe homes and decent jobs would seem much more sensible.

Just a quick note to apologise to readers via the email newsletter about the some of my recent posts which included embedded YouTube videos. They didn’t appear in the emails – you needed to click the read in browser link to see them. This must have made some of what I was writing about (eg about Phoebe Buffay) even more incomprehensible than usual! I intend to link to them for the time being (as I did yesterday) rather than embed them until I can work out a way to smuggle them past mail servers!

You will have all seen the work mug staple: “The Difficult We Do Immediately. The Impossible Takes a Little Longer”. The original quotation in the title, originally attributed to Charles Alexandre de Calonne, the Finance Minister for Louis XVI, in response to a request for money from his Queen, Marie Antoinette, appeared in a collection from 1794, this was a year after Louis and Marie Antoinette (but not Charles, who survived another nine years) died on the guillotine and five since George Washington had been inaugurated as the first President of the United States. It seems as if the seemingly impossible may need to be attempted once again.

So let’s start by expanding on the problem which I brought up in my last post. The problem goes much wider than Donald Trump. He is assembling a court of loyalists around him, in the style of a mob boss, which as has been observed by others, has been the prelude to fascism in the past. As Jason Stanley, Professor of Philosophy at Yale and author of Erasing History: how fascists rewrite the past to control the future, puts it: “the United States is your enemy”. There is also considerable circumstantial evidence to suggest that Trump is considered an agent of influence by Putin’s regime in Russia.

The difficulty of what I am about to suggest is also the reason why it is so urgent: our relationship with the United States (the one we keep needing reassurance by successive US Presidents of its special nature) is positively symbiotic. George Monbiot lists some of our vulnerabilities here:

Through the “Five Eyes” partnership, the UK automatically shares signals intelligence, human intelligence and defence intelligence with the US government. The two governments, with other western nations, run a wide range of joint intelligence programmes, such as Prism, Echelon, Tempora and XKeyscore. The US National Security Agency (NSA) uses the UK agency GCHQ as a subcontractor.

Depending on whose definitions you accept, the US has either 11 or 13 military bases and listening stations in the UK. They include RAF Lakenheath in Suffolk, from which it deploys F-35 jets; RAF Menwith Hill in North Yorkshire, which carries out military espionage and operational support for the NSA in the US; RAF Croughton, part-operated by the CIA, which allegedly used the base to spy on Angela Merkel among many others; and RAF Fylingdales, part of the US Space Surveillance Network. If the US now sides with Russia against the UK and Europe, these could just as well be Russian bases and listening stations.

Then we come to our weapon systems… among the crucial components of our defence are F-35 stealth jets, designed and patented in the US.

Many of our weapons systems might be dependent on US CPUs and other digital technologies, or on US systems such as Starlink, owned by Musk, or GPS, owned by the US Space Force. Which of our weapons systems could achieve battle-readiness without US involvement and consent? Which could be remotely disabled by the US military?

Then there is our independent nuclear deterrent, which is “neither British nor independent” according to Professor Norman Dombey, Emeritus Professor of Physics and Astronomy at the University of Sussex.

Then there is the sheer cost of rearming with Europe to the extent necessary in the absence of the United States’ support, suggesting 3.5% rather than 2.5% of GDP is what will be required, suggesting the UK Government, with its WCAIWCDI approach described here, will need to find something in addition to the foreign aid budget to ransack. I will be talking more about defence spending in a future post.

It is small wonder that some commentators, such as Arthur Snell, former Assistant Director for Counter-Terrorism at the Foreign and Commonwealth Office, conclude that disentangling ourselves from the United States may be impossible. And that is just considering defence and security considerations.

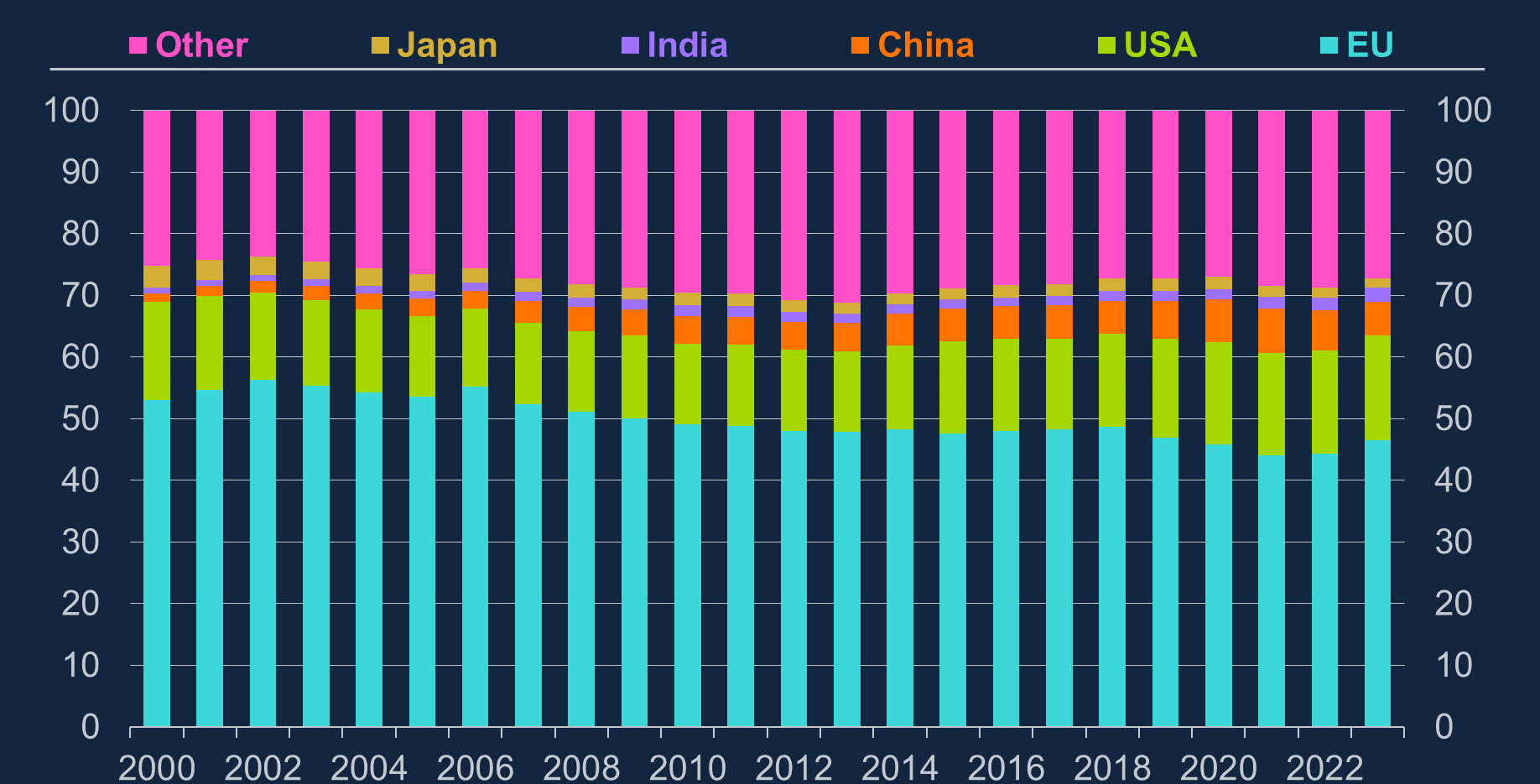

On the economy the symbiosis is just as evident. First of all there is the sizeable proportion of our imports and exports of both goods and services which are with the United States. Only in June 2023, we were trying hard to develop these further with something called the Atlantic Declaration. Although, as a recent speech by Megan Greene of the Bank of England’s Monetary Policy Committee shows, our trade with the US as a proportion has remained remarkably stable since 2000 at least.

Source: ONS and Bank calculations. Trade weights for each trading partner are calculated as the sum of bilateral exports and imports as a share of total UK trade. Data is annual and in current prices. EU refers to the EU27. Latest data point is 2023

Culturally, the United States is embedded in our laptops and mobile phones, our television programmes and movies, and our social media. Its concerns have permeated our language and our politics. A reasonable proportion of our political and financial elite have been to their universities and theirs to ours. Many of our employers have US parents: just in the actuarial world, two of the three biggest consultancies (Aon and Willis Towers Watson) are described as British-American firms, with the other one (Mercer) headquartered in New York. It has Apple. It has Amazon. It has Google. It has Meta and, of course, X.

And perhaps the greatest entanglement of our two countries is political, to the extent that we routinely send our politicians to each other countries to support election campaigns and our media breathlessly report every in and out of the US Presidential elections. We are lucky if a French or German one is mentioned more than a couple of weeks before it takes place. Whether it is the language thing (we are still VERY resistant to learning other languages) or the post imperial thing (feeling like we have a special understanding of the problems the United States face as a self-appointed global police force) or the degree of financialisation of our economy or for some other reason, it is very hard to avoid a sense of being conjoined with the United States of America.

But it is precisely because our relationship is so close in so many important areas that we are particularly vulnerable to US pressure – the harder it will be to disentangle ourselves, the more urgent it is that we do.

As David Allen Green puts it this week, the US is currently undergoing a diplomatic revolution. Originally applied to France’s realignment of all of its alliances away from Prussia and towards Austria, which ultimately led to the work mug motto at the start of this piece, the US appears to be realigning itself towards Russia and away from the UK and the EU. As Green goes on to say:

Other countries would now be prudent to regulate their affairs so as to minimise or eliminate their dependency on the United States – it is no longer a question of waiting out until the next United States elections.

And other political systems would be wise to limit what can be done within their own constitutions by executive order, and to strengthen the roles of the legislature and the judiciary (and also of internal independent legal advice within government).

The last seems key to me. We cannot, particularly now we are outside the EU, afford for our main ally to be capable of being so capricious. This applies whether the US are allowed to and do elect a President in 2028 who is respectful of its institutions and constitution. We always felt Americans were very respectful of their constitution because they never stopped talking about it, but it turns out to have been a thin veneer with little meaning. Much like our discussion of sovereignty in the UK.

The first thing we need to do is to stop obsessing about what John Mulaney memorably referred to as a “horse in a hospital” in 2019. Despite the fact that was five years ago and we have now seen a horse in the hospital before, many have been turned off news coverage altogether by the anxiety caused as a result of the constant media narration of what Trump and Musk have done next each day. The dangers of treating the Trump and Musk chaos as a TV show are potentially existential in the US but grave for us in the UK too.

While we may have deep sympathy for the people in the US and other countries caught up in the chaos, our priority has to be to get our own house in order. Otherwise we won’t be any help to anyone.

My priorities would be the ones I set out in October 2022, only now with much greater urgency.

We can’t have parties with only 20% of the popular vote (34% of a 60% turnout) having an absolute majority of 174 seats. We need proportional representation, so that every vote counts equally and perhaps we might get somewhere near the turnout of Germany’s last election of 82.5%.

Reform media ownership and promote plurality in support of a more democratic and accountable media system. The Media Reform Coalition has produced a manifesto for a people’s media which I support: it includes proposals for an Independent Media Commons – with participatory newsrooms, community radio stations, digital innovators and cultural producers, supported by democratically-controlled public resources to tell the stories of all the UK’s communities. As we know, our social media is controlled by Meta (with Facebook, WhatsApp and Instagram), all of which have more than 2 billion active users and Google with YouTube, also with more than 2 billion active users. X still has over half a billion, despite what Musk has done with it. In newspapers, 90% of daily circulation is controlled by three firms: News UK, Daily Mail Group and Reach plc (which has most of the local titles you’ve ever heard of, including the Birmingham Mail and Birmingham Live, as well as The Daily Express and the Daily Star).

Reform election finance. Recommendations for doing this were provided in the July 2021 report by the Committee on Standards in Public Life. There was an eye-watering amount of money spent in the US Presidential Election this time: The Democrats spent $1.8 billion and the Republicans $1.4 billion, with $2.6 billion and $1.7 billion respectively being spent by the two parties on the Senate and House races. In the UK, paradoxically, the relatively small amount of money donated to parties mean that they are potentially more vulnerable to well organised lobbying operations. This is why the offer of $100 million by Musk to Reform led for calls to restrict foreign political donations to profits generated within the UK.

This way we would be more resilient to the many ways that the current chaotic United States establishment can reach into our own politics and governance, and start to develop policies with broad support which can reduce our dependency on the United States.

For reasons I won’t go into involving a green double decker bus, a holiday cottage in St Ives and some raw scallops, I started watching a box set of the Sopranos in September 2023, rather later than the rest of the world, which had finished with the mobsters from Brooklyn in June 2007. We finally reached the 21st episode of series 6 a few months before Christmas 2024. And reacted in much the same way as I now gather (having researched it primarily to check I hadn’t got an incomplete box set) the rest of the world did over 17 years ago.

There are many advantages to watching something so long after the media around it has moved on. You get left in peace to watch it at your own pace. No one is giving you spoilers in little teasers stuck between other programmes. The chat shows are not talking about it. You don’t have to hear what every minor celebrity thought about it. You aren’t being constantly encouraged to get excited about it. You can just watch it.

However, now I have read up on the reaction at the time and the increasingly irritated responses of the show’s creator David Chase to the line of questioning he was getting about it, I think there is something for us here in March 2025. In particular, I am thinking about the following comment Chase made soon after the last episode first aired:

[The ending] said much more than Tony facedown in a bowl of onion rings with a bullet in his head, or taking over the New York mob. Tony Soprano had been people’s alter ego. They gleefully watched him rob, kill, pillage, lie and cheat. They cheered him on. And then, all of a sudden, they wanted to see him punished for all that. They wanted “justice”. I thought that was disgusting, frankly.

Chase also made reference to the fact that the US was involved in war against the Taliban in Afghanistan at the time and the Al-Qaeda unexploded car bombs in London that month:

There was a war going on that week and attempted terror attacks in London. But these people were talking about onion rings.

Which brings me to Donald Trump. Chase was interviewed by, amongst others, The Irish Times in 2019, the 20th anniversary of the first episode, and Trump perhaps inevitably came up in response to a question about the influences The Sopranos has had:

The use of a deeply flawed hero and his problems. And when news shows talk about Trump, for example, they’ll say it’s like The Sopranos. People, including your own paper, use The Sopranos as an example of crookedness and culpability. I don’t watch a lot of series television. Unfortunately what I do is spend my time watching CNN, Fox and MSNBC. So I get good and depressed, and angry.

What struck me about The Sopranos was how chaos followed him everywhere he went. Any normal person who interacted with his people got exploited, corrupted if possible and often destroyed, whether it was an AA sponsor who gets drawn into gambling on a scale he can’t handle, or someone who wants to cooperate in a movie, or even the staff and other patients where Tony is recuperating from being shot. He appears to be behaving normally and then he will suddenly beat up his own bodyguard for no other reason than to show his people that he’s not over the hill. He is both ridiculously sentimental and utterly ruthless if he feels threatened. And yet you are still left rooting for him a lot of the time, which of course is what made it such a fascinating series and also explained the consternation when the screen went black.

Now this is all very well when we are talking about a fictional character heading up a mob operation in Brooklyn. However it becomes something else entirely when it is a real President of the United States. There are so many perils to dealing with Trump: those which are like The Sopranos, ie the danger of being exploited, corrupted and destroyed by him. We saw this in full operation yesterday in the extraordinary treatment of Volodymyr Zelenskyy by him and his chief henchman JD Vance.

The full Oval Office remarks of President Trump, Ukrainian President Zelenskyy and Vice President Vance that ended in a contentious exchange over continued support amid the ongoing war with Russia. For more context and news coverage, click here: https://www.nbcnews.com

And when he is found guilty of 34 counts of falsifying business records, making him a convicted felon, it is not, as he claims “a rigged trial by a conflicted judge who was corrupt”, to be laughed off as just another one of Trump’s scrapes from which he emerges victorious.

We need to get our heads up out of the onion rings. This is not TV entertainment, it is the immediate future of the United States, impacting all of us whose countries need to interact with them without being exploited, corrupted or destroyed. He poses a serious risk to all of us.

So the question is what to do about it? This is what I intend to address in my next post.

It started as soon as they came into government in July.

“If we cannot afford it, we cannot do it.”

This was obviously a rebuttal to the Keynes statement from the 1940s:

“Anything we can actually do, we can afford.”

The list of things “we can’t afford” started to grow, including:

Winter fuel payments for pensioners not on Pensions Credit. This cut the number of pensioners receiving the winter fuel payment from 11.4 million to 1.5 million and will save £1.5bn in the next financial year.

Stopping reforms to social care proposed by Sir Andrew Dilnot. These would have meant making the means test for local authority support more generous and raising the capital limit from £23,500 to £100,000. Estimated saving: £1 billion.

In April, the employer national insurance rates will increase (from a previous decrease we now “cannot afford”). These are forecast to raise between £23.8 billion and £25.7 billion a year, for the five years 2025/26 to 2029/30.

So far, so predictable, based on the we-cannot-afford-it-we-cannot-do-it (WCAIWCDI) philosophy. But then we had a tweak.

In response to criticisms of the decision to approve the construction of a third runway at Heathrow, the UK’s Business Secretary Jonathan Reynolds came up with a new formulation:

“We simply cannot afford to say we don’t build reservoirs any more, we don’t build railways, we don’t build runways. That’s not good enough, we will be left behind.”

Burrowing through the double negative we have a complete reversal of WCAIWCDI. Instead we now have we-cannot-afford-to-say-we-don’t-build-X, where X is something they desire to build. WCATSWDBX if someone wanted to reduce it to an acronym. Obviously you would have to be fairly determined to do so.

So we-can’t-afford-it can be used both positively and negatively it seems. We can’t do it if it is bad spending, we can’t afford to say we don’t do it if it’s good spending.

And now we come to defence spending as the US support for Ukraine starts to look highly conditional. We are still not sure whether this is in the WCAIWCDI or the WCATSWDBX camp. On the one hand, the PM has said that we are prepared to send troups to Ukraine, which sounds like WCATSWDBX. On the other hand, recent statements by the defence secretary and the PM also suggest that they are not considering anything beyond an increase in defence spending from 2.3% of GDP to 2.5%. Which sounds more like WCAWCDI.

Elsewhere there has been optimism amongst some (eg here and here) that the need to increase defence spending will topple the WCAIWCDI regime and allow other spending priorities in too. Others fear that any increases will just lead to further cuts to other public spending.

It’s no way to run a railroad. The government needs to be more Phoebe Buffay and just tell us what they do and don’t want to spend money on instead of telling us that we can’t afford things to avoid the discussion like an overbearing parent. Then we could have a proper family argument about them.

The Charybdis is a swirling water feature in the temperate house at Savill Garden. It was designed by Giles Rayner in 2006. https://funandgames.org/web/wp-content/uploads/2020/09/The-Charybdis_Savill-Gardens_9257-2-scaled.jpg

This is a quote attributed to Lenin (courtsey of Branko Milanovic’s X account, where a gentle exchange about whether it was genuine ensued), which seems perfect for the moment we are in.

It was back in 1998 that George Monbiot first pointed out that no sector was as wedded to PFI deals as health. The famous example in Captive State of the Walsgrave hospital in Coventry, knocked down and replaced by a smaller hospital at much greater cost, was just one of many. It didn’t occur to me at the time, but the wider lesson from these early examples, borne out by everything we have seen since, is that privatisation, in whatever form (and, after all, what is PFI but the privatisation of a funding source), always solves a smaller problem than the one you have. The history of privatisation in the NHS has been a series of smaller easier problems dealt with in some cases very efficiently by the private sector (although the efficiency only ever seems to increase the profits of the private companies concerned rather than reduce their price). As it has been in transport (with rail franchises yo-yoing in and out of state control whenever the ask becomes too complex for the train operators taking them on), and utilities, mail services, etc etc.

And the size of the problems that the private sector can take on would appear to be getting smaller.

Take insurance. Ann Pettifor highlights this week what Petra Hielkema, chair of the European Insurance and Occupational Pensions Authority, has to say about the future of the sector in the FT. Apparently he told them that governments and banks will struggle to cope with the soaring costs of natural catastrophes such as floods and wildfires. More households will be unable to insure their homes and the mounting losses from natural disasters could destabilise banks. Two things he said were particularly striking:

“I think it is the biggest risk facing society, frankly” and “Member states — they can’t cope with this.”

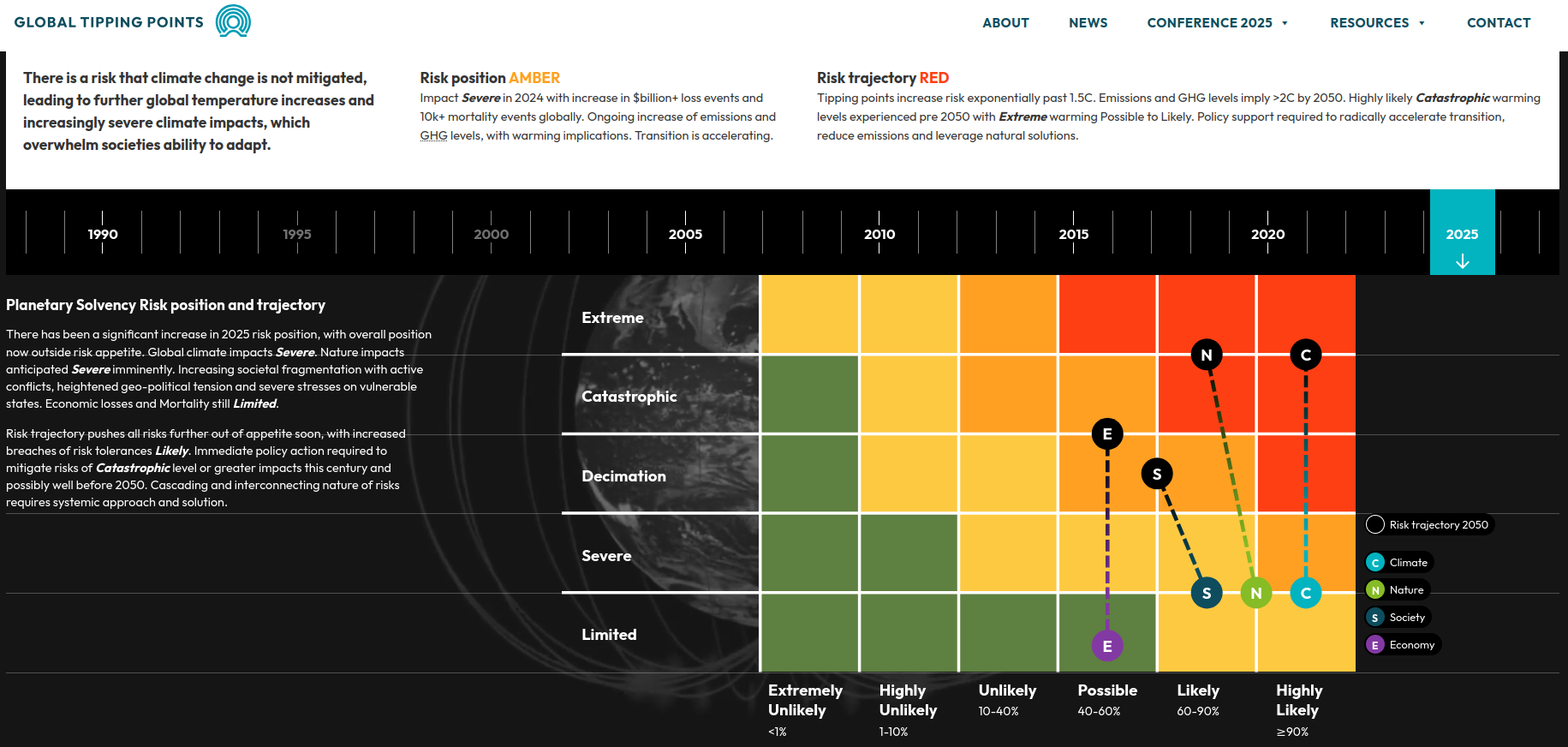

This contrast between public and private ownership of problems struck me while I was reading the excellent report from the Institute and Faculty of Actuaries and the University of Exeter on climate change: Planetary Solvency. By taking the approach that an insurance company would take in determining its risk appetite and then seeing if its risk exposure matched up to it, it occurred to me that the reason this had never been done before for global climate change was that any insurer would have left such a market years ago on the basis of a brief initial analysis of the problem. Something that a private insurer can always do with any problem.

What if, instead of the NHS being threatened by covert privatisation, the threat is that even the smaller problems private health is currently solving within the system get handed back to the NHS? Because that is the difference. During the pandemic, the threat was that the NHS might not be able to cope with the surge in very ill people and that many would die without care as a result. The reason large parts of NHS operations were repurposed and we were all urged to “flatten the curve” was because, ultimately, there is noone the NHS can hand the responsibility back to and their resources are measured in hours of the right people available to work for them rather than pounds spent and so have a hard physical limit. Although there were significant failures as the Covid Inquiry is currently exploring, the NHS as a whole did not fall over.

However, neither did the US system, because an insurer merely withdraws from a market which might cause it to. It has no responsibility to the system as a whole.

As one MIT researcher responded to being asked about the lessons for the US system of the pandemic:

“The pandemic has revealed the American health care system to be a non-system.”

So it seems to me that arguments about privatisation and nationalisation are a bit beside the point. We have big problems, getting bigger every day, which absolutely have to be solved and limited physical resources with which to do so. Unfortunately His Majesty’s Opposition are still trying to disentangle themselves from the wreckage of Tufton Street’s “thought leadership”, risking a Trumpian climate change denying, health service privatising Reform Party replacing them, and His Majesty’s Government appear to have no idea what they are doing.

So reality does feel pretty radical at the moment. We need to be equally radical in our response to it.

{kind=link}