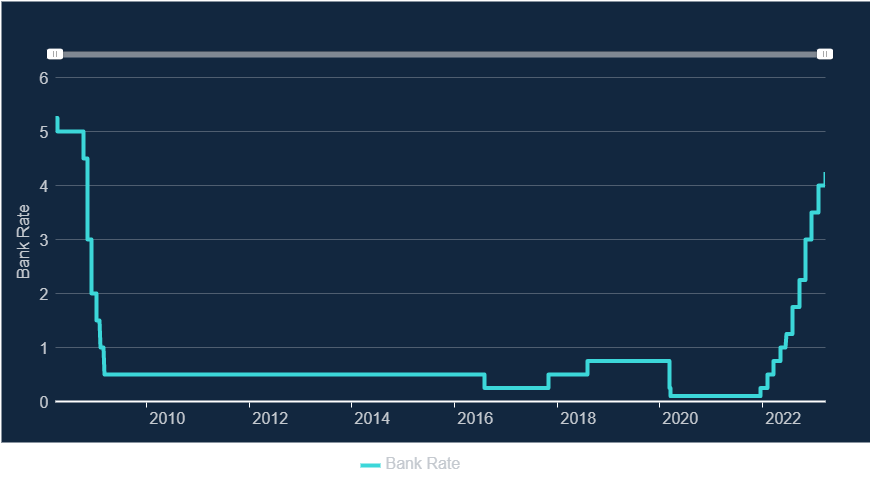

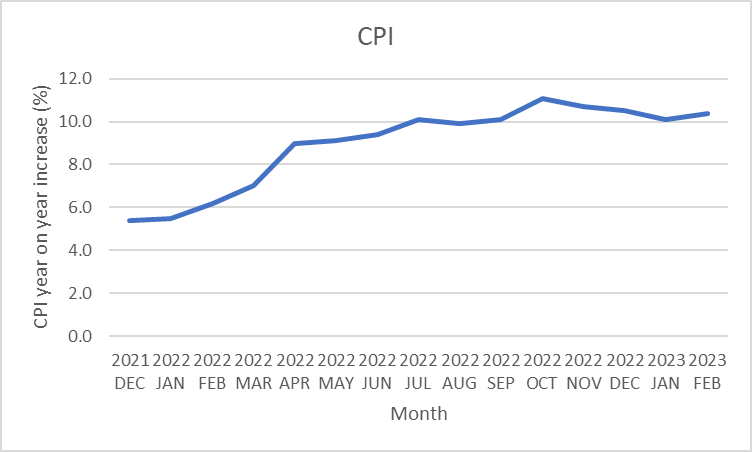

The Bank of England has today raised the Bank Base Rate for the 11th time since December 2021 to 4.25%. Its stated goal is to tackle inflation. So let’s have a look at inflation since December 2021:

Now that doesn’t look like a policy which is working does it, but I am being a little unfair. There is supposed to be a lag between movements in interest rates and impacts on inflation after all. Opinions differ about how long the lag is: a paper from Lancaster University from 2001 suggests over a year based on US and UK data since 1953, and a generally accepted 18-24 month lag has been routinely quoted in economics text books for many years. However, Catherine Mann, an external member of the Bank’s Monetary Policy Committee, at the end of a very long speech to the Resolution Foundation on 23 February 2023 which dealt with the transmission mechanisms between monetary policy and the economy in considerable detail, concluded with the following summary of why this time is different:

So, what does this all mean for monetary policy? Typically, we assume that the world is

sufficiently stable such that the estimated relationships between, for example Bank Rate

and inflation also are stable and we can look to these when deliberating monetary policy

stance – the folk wisdom of 18 to 24 months.

In this speech, I have presented state-of-the-art evidence which shows that, in normal

times, the monetary transmission into inflation is in fact faster, peaking within the first year.

But, I have also reviewed factors that may change these relationships – change the long

and variable lags – including a) that there has been a sequence of shocks, b) that the

transmission from monetary policy to financial markets has been quick, but not all in the

direction of tightening, and c) that the degree of backward- or forward-lookingness in

expectations formation influences the effectiveness of monetary policy. Going forward,

how should this reassessment of lags determine the appropriate monetary policy strategy?

She then went on to say that financial conditions remained too loose and ended with the following chilling words:

We have an inflation remit, and we will achieve it one way or another.

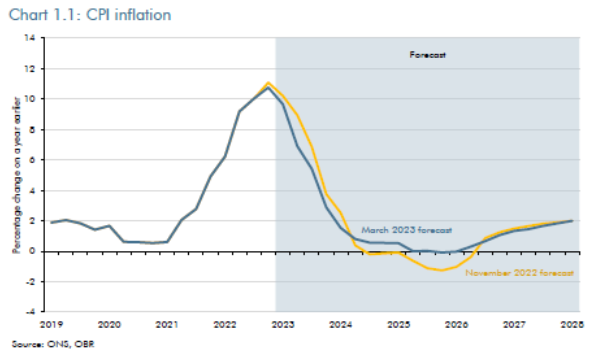

Now you will notice from the CPI graph that the big increases happened between December 2021 and April 2022, when the rate of increase went up from 5.4% to 9.0%. As the price increases are always measured relative to the same month 12 months earlier, once we pass the April 2023 point, this price shock will inevitably be in all months in the comparison and the headline rate will start to plummet. The latest OBR forecast for CPI therefore looks like this:

Bearing in mind that the Bank of England’s CPI remit is 2%, and with all the usual caveats about OBR forecasts, it appears that Catherine and her colleagues are intent on over-achieving it.

One person I have been reading a lot recently on inflation is Blair Fix. He recently posted a great piece showing the empirical evidence to support the theory that higher interest rates increase inflation. His most recent piece reframes the whole question of inflation into the idea of competing price raising. When wages rise more than prices (yes, my younger readers, that did sometimes happen), people working for wages (ie most of us) win. When interest rates rise more quickly then prices, people who have assets available to lend to other people (ie not most of us) win. What we call inflation is bad because our wages don’t keep up with it. In the 1970s by and large they did and our borrowings were reduced in value by the inflation of prices. So inflation tends to redistribute wealth according to where the prices are allowed to rise.

Blair Fix also discriminates between price battles, which are the endless struggles between workers and creditors, and price wars, which are less frequent but result from an escalation when everyone joins in, normally after a price shock of some kind.

We are currently in a price war. The Bank appears to have picked the side of the creditors and the protection of real interest rates over the protection of real wages, which is perhaps inevitable when union power is now so diminished and the financialisation of our economy so advanced. It is perhaps the first real test of the economy we have created in the wake of 2007 and who it really works for when under fire. A former member of the Monetary Policy Committee, David Blanchflower, has called the latest rate rise “resignation stuff”. On the other side, Catherine Mann and her colleagues may even now be thinking they have not yet gone far enough.