This review originally appeared in the April issue of Brum Group News, the newsletter of the Birmingham Science Fiction Group and is reproduced here (with light editing) by kind permission

A few years ago the historian Adam Tooze said the following about the times we are living in:

If you’ve been feeling confused and as though everything is impacting on you at the same time, this is not a personal, private experience. This is actually a collective experience.

The word he came up with for this experience was “polycrisis”. It described the interplay of the Covid pandemic, Ukraine war and the energy, cost-of-living and climate crises. To that we could now add Trump 2nd term, war in Gaza and now the Gulf.

I am reviewing this book while I have Covid, which has certainly facilitated the kind of inner focus which I think the book is asking for. Because Slow Gods is polycrisis in the form of space opera, but a curiously interior-monologuey kind of space opera, more psychological than boom-boom.

The premise, as Claire North set out for us at the Birmingham Science Fiction Group last June, is that a binary star system is due to collapse which will obliterate all life within an 83 light-year blast radius. Unusually, the populations in the vicinity are warned of this precisely 100 years in advance by a perfect black sphere moving through space at sub-light-speed and known by everyone as the Slow.

The Slow listens to everything, remembers it and will consider it.

We follow the story through the eyes of Maw, who has been killed and has recovered in such a way as to be very difficult to kill after that. Making Maw an ideal candidate for Pilot, the organic sentient needed in the pilot’s seat of any ship wishing to enter arcspace which lets it travel across the universe faster than light, at huge personal cost. Pilots die frequently and each planetary system has its own way of choosing and rewarding its Pilots. Only Maw appears to be able to act as Pilot again and again, which makes the people around Maw nervous.

The main thing about Maw which makes people nervous is Maw’s relationship with “the darkness” which reaches into any ship in arcspace, in many cases sending people mad. Maw, instead, becomes “curious”, exploiting a changing relationship and perception of matter in the darkness to do monstrous things. But, despite all this, Maw is still required to keep running missions, although usually with a mechanical assistant to keep Maw from getting “dysregulated”.

This unusual set up turns out to be a way of observing the psychology of the polycrisis with some clarity. The United Social Venture is an empire where its subjects acquired debt just from being born (measured in Glint):

Everything the Venture gave us – the air we breathed, the roads we walked down, the schools we learned in – had been sweated for, bled for, and our debts were a marker of the needful labour we would give back in return.

This economic system was referred to as Shine. The Shine were one of the few systems which used prisoners for Pilot work.

One of the joys of the book is the exploration of difference, lots of details about avoiding giving offence when the Xi of Xihanna ask Maw to pilot a ship to Adjumir to bring out historical artefacts and Maw meets Gebre of the Haalo Institute. Maw finds that Normspeak is regarded as a very crude way of communicating and starts, haltingly, to learn Adjumiri (which is at least in part a click language). So begins a very moving love story.

Gender differences between systems are very striking. The Shine have only two genders – “he” and “she” – although the elite also have hé and shé. The most manly and the most feminine.

There are four genders in Xihanna, but they are not regarded as particularly important characteristics of a person and dispensed with once you know someone well. On Adjumir, there are eight, with very few Adjumiris remaining the same gender all their lives. These differences are picked out by the brilliant use of pronouns, a useful technique in a book full of characters. Even mechanicals, who have no particular interest in gender, are referred to as qe/qis as a mark of respect as “they do not wish to be put in the same category as a bowl of soup or a broken chair”.

We join Maw towards the end of the 100 year programme to evacuate the populations of Adjumir and Hadda to relative safety, with 800 million still on the planets and increasingly desperate. The Slow has effectively taken on a role as God through its massive databases, calculation capacity and sheer longevity. It seeks out Maw as it has plans for him. The Slow has been around so long that qe sees everything in the very long run. Which means that the emotional turmoil and intense highs and lows of individual lives are all averaged out to nothing. Qe calculates in terms of galaxy-level populations on the basis of what qe has come to think of as love.

What calculation would the Slow make about our world, with all our nation states and their often tiny differences blown up to justify war aims? Donald Trump certainly has to have the most Shine of any US President for some time.

Slow Gods moves slowly but relentlessly towards a showdown between Maw and Theodosius Rhode, the Executor of the Shine and executioner of his mother. There is much tragedy along the way and the ending is not straightforward but ultimately very satisfying. It’s an uplifting ride.

OK I don’t know if this is a remotely helpful post, but it really feels to me like one of those months we will look back on, like March 2020, and wonder what we were thinking. To recap: on 4 March 2020, while Italy were shutting all their schools and a month after the WHO had declared a global health emergency, we were noting that the number of cases in the UK had jumped from 53 to 87 in one day.

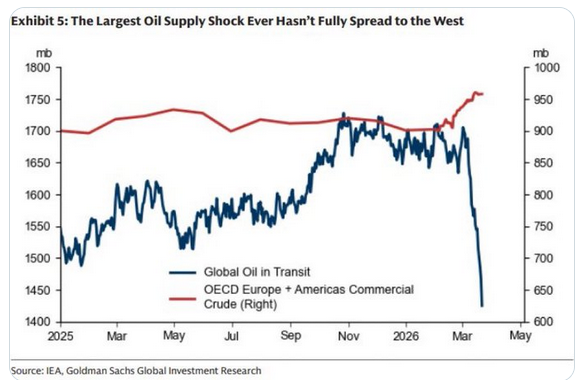

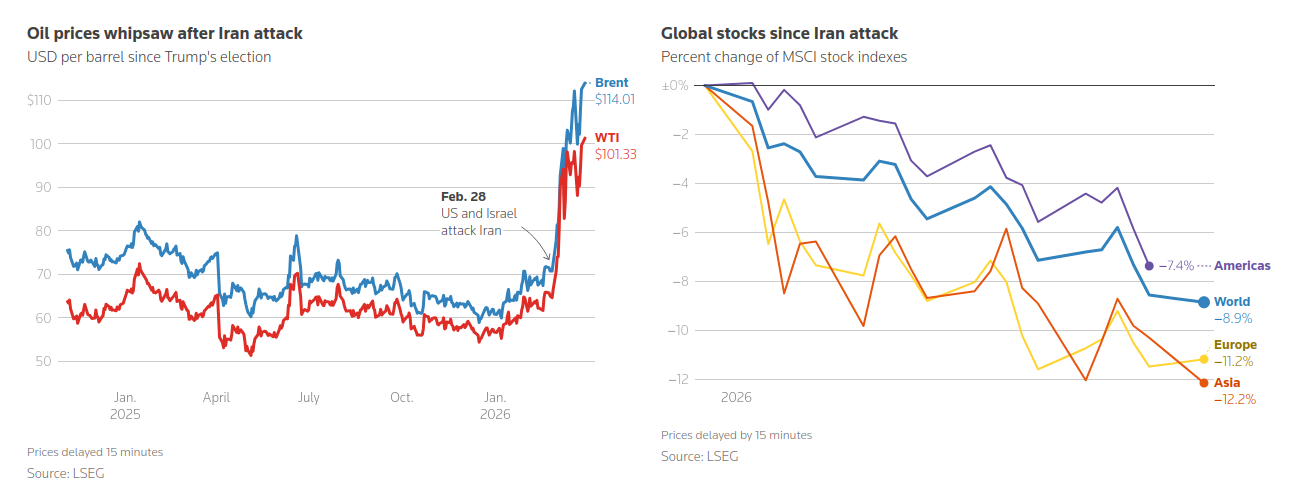

Jump forward to now and the number of tankers with oil on board is in freefall:

Trump is talking about invading Kharg Island and “obliterating” Iran’s energy facilities, and we are sitting in the time lags of international fossil fuel freight waiting to see what will happen. But we already know what is going to happen. Just like the pandemic, we will be taking similar measures to the countries already more affected very soon. The order looks like Asia, followed by Africa, then Europe and only then, ironically, the United States.

So what is going on in Asia right now? Well the Philippines announced a national energy emergency six days ago, setting up an authority to oversee the orderly distribution of fuel, food, medicines, and other essential goods. Sri Lanka has announced a four-day week for all government employees. Egypt is ordering restaurants, cafés and shops to close at 9pm to safeguard dwindling energy reserves. Slovenia has brought in fuel rationing. Moldova’s Parliament has also voted to impose a state of emergency in the country’s energy sector. Australia is offering free public transport. Measures are also being taken in Thailand, Ethiopia, Myanmar, Vietnam, Bangladesh and South Sudan.

On 3 March 2020, the UK Government unveiled their Coronavirus Action Plan, which outlined what the UK had done and what it planned to do next. Paul Cosford, a medical director at Public Health England, said widespread transmission of COVID-19 in the United Kingdom was “highly likely”.

On 4 March 2020, the Daily Express were telling us:

Which we clearly weren’t. Meanwhile the Daily Mail was anticipating future lockdowns and 6 million people being off sick:

The next day we had the first Covid death in the UK. And life was on hold for the next two years.

Our response to the energy crisis seems to be almost entirely focused on

1. The cost-of-living crisis; and

2. The financial markets.

The Education Secretary has said that motorists should fill up as normal as the government is “well prepared” for disruption. The trouble is, many of us still remember September 2000:

So that would be enough to make us all feel nervous about shortages and queues for everything, having our lives disrupted and out of our control. But the real potential issue is not even being talked about, certainly not by the government. It is a shortage of food. Steve Keen sets out the economics of global food production here. This does not tend to feature prominently in mainstream economic analyses which are energy and food blind for the most part, although the FT did have this graph a couple of weeks ago:

As Steve Keen says:

Survival will depend on grain reserves. China has of the order of 18 months in reserve, which will insulate it from the disruptions of 2026. The USA and India have substantial reserves as well, but some countries—including the UK—have virtually none.

…Famines will ensue, and even countries that have never experienced such events could be forced into food rationing. This includes the UK and Australia, and a patchwork of countries across Europe.

This is what people are nervous about: not being able to get enough food, either because it isn’t available at all or not at a price they can afford. Calling that a cost-of-living crisis is a bit like calling the Black Death a labour market crisis. And it doesn’t stop there. As Steve Keen continues:

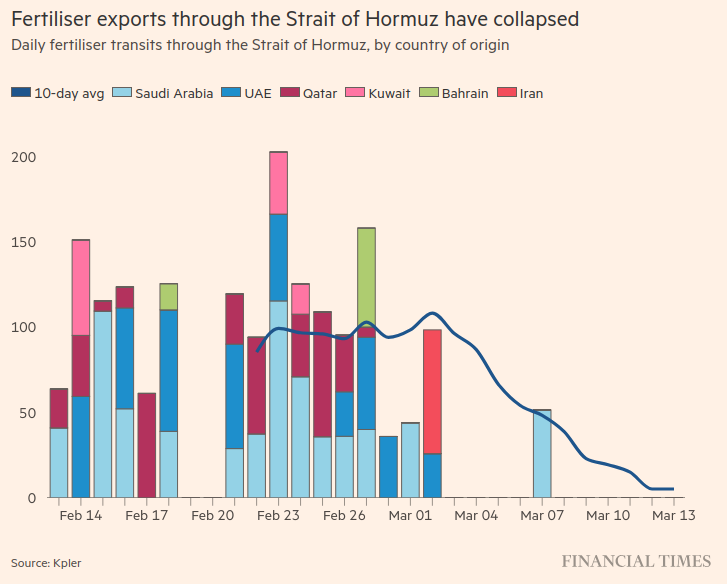

Other critical products that normally pass through the Strait of Hormuz include Helium, which is critical to the production of semiconductors, and sulphuric acid, which is critical to numerous production processes. The closure of the Strait cuts off one third of global helium output and about half of global sulphuric acid output.

With critical industrial inputs cut as well, the problems will cascade well past food alone—though that is clearly the most damaging impact. With LNG, petroleum, helium and sulphuric acid production cut, the capacity to undertake repairs to damaged facilities will also be hindered.

The TED War is rather like smashing a spider’s web—and then killing the spider.

The spider certainly looks in a poor state of health at the moment, and parts of the web will take years to fix. This is the crisis we are all inevitably going to be entering in the next few weeks. For who knows how long.

A risk management approach to this crisis would involve communicating a plan to the country that minimised the impulse to hoard resources and protected the most vulnerable from extreme prices, rather than bland reassurances from government ministers. We need this to be in place very quickly now.

Seven years ago I wrote about Catch 22 and actuarial practice, concluding, rather piously:

If we want far fewer actuaries to be employed in not growing alfalfa in the future and far more working on making the finance structures of our economy work better, whether to support a Green New Deal or more generally, we first need to embrace the idea that our current economic priorities are indeed insane.

So imagine my excitement at finding Catch 22 grabbed out of the pages of fiction and informing US foreign policy. Not convinced? Compare two passages. The first, from Catch 22, in 1961:

This time Milo had gone too far. Bombing his own men and planes was more than even the most phlegmatic observer could stomach, and it looked like the end for him. High-ranking government officials poured in to investigate. Newspapers inveighed against Milo with glaring headlines, and Congressmen denounced the atrocity in stentorian wrath and clamored for punishment. Mothers with children in the service organized into militant groups and demanded revenge. Not one voice was raised in his defense. Decent people everywhere were affronted, and Milo was all washed up until he opened his books to the public and disclosed the tremendous profit he had made. He could reimburse the government for all the people and property he had destroyed and still have enough money left over to continue buying Egyptian cotton. Everybody, of course, owned a share. And the sweetest part of the whole deal was that there really was no need to reimburse the government at all.

This week, the US Treasury lifted all oil sanctions on Iran. For 30 days. 140 million barrels of Iranian crude, sitting on ships at sea, may now be sold freely on the global market. Including to the United States itself.

In yuan.

The United States is purchasing, with Chinese currency, oil from the country it is currently bombing?! The same oil that funds the missiles that just shot down an F-35 for the first time. The same missiles that are redecorating allied oil infrastructure.

Treasury Secretary Bessent called this “narrowly tailored”. Narrow like in white, and tailored as in card, apparently.

In the same OFAC filing, Russian oil sanctions were lifted as well. And Belarus potash too, because apparently the universe was running low on irony and needed to top up.

The logic, insofar as there is any, goes like this: the war has crashed the global oil market so hard that the administration needs the enemy’s oil to keep gasoline prices from eating the midterms. They are unsanctioning the people they’re bombing because the bombing is working too well at the thing they didn’t want it to do. The sanctions were necessary to stop Iran funding the war, but the war made the sanctions too effective, so the sanctions had to be lifted to fund the war effort against the country that no longer needs sanctions because the oil revenues that sanctions were preventing are now required to prevent the economic damage caused by preventing those revenues, which is itself a consequence of the military campaign designed to make the sanctions unnecessary by making Iran the kind of country that doesn’t need sanctioning, which it would be, if the sanctions hadn’t been lifted to pay for making it that.

There have been many names thrown at Trump since he arrived in US politics. My personal favourite is probably the Tangerine Tyrant. Many people are currently relying on TACO (Trump Always Chickens Out) to resolve the Middle East crisis he has instigated. However, until now, I had not heard of anyone likening him to Milo Minderbender. But once you see it, it is difficult to un-see it.

Trump likes to give himself and everyone else nicknames. From the very stable genius of his first term, to more recently Honest Don and the Tariff King, whereas Milo, as M&M Enterprises (the company he started as the mess officer) expands, becomes the Mayor of Palermo, Assistant Governor-General of Malta, Vice-Shah of Oran, Caliph of Baghdad, Mayor of Cairo, and the god of corn, rain, and rice.

Trump likes to use his presidency to enrich himself, from his Trump coin to the Amazon documentary about his wife to his Board of Peace to all of his merchandise. Milo’s catchphrase is “what is good for M&M is good for the country”.

Trump doesn’t appear to believe in safety nets for ordinary people. Meanwhile Milo secretly replaces the CO2 cartridges in emergency life vests and the morphine in first aid kits with printed notes to the effect that what is good for M&M is good for the country.

Milo Minderbender is a war profiteer trying to convince himself that he is a free market fundamentalist. So what does that make Trump? Well hold that thought, because today’s Guardian has provided a partial answer I think, with a history of military targeting.

This introduces the concept of the kill chain, ie the process between detecting something and destroying it. Trying to shortcut the kill chain has been a perennial preoccupation of militaries through the ages. In the Vietnam War, Operation Igloo White dropped 20,000 acoustic and seismic sensors along the Ho Chi Minh trail, which transmitted data to relay aircraft, which then fed the signals to the IBM 360 computers at Nakhon Phanom airbase in Thailand. These analysed the data, predicted where the convoys would be and strikes were directed to those locations. The Viet Cong realised quickly that this system could not detect the difference between military vehicles and ox carts and therefore:

They played recordings of truck engines, herded animals near the sensors to trigger vibration detection, and hung buckets of urine in trees to set off the chemical detectors.

There was no way to independently check what they were destroying. The air force claimed 46,000 trucks were destroyed or damaged, which the CIA calculated exceeded the total number of trucks believed to exist in all of North Vietnam.

…air force personnel invented a creature to explain the absence. They called it the “great Laotian truck eater”.

Last time I talked about military targeting, I focused on the human in the loop, but let’s instead focus on the actual destruction going on for a moment, shall we? Trump’s assault on Iran hit 6,000 targets in two weeks. The kill chain had, apparently, been compressed so much that it allowed 1,000 decisions an hour. The school he hit, killing between 175 and 180 people, most of them girls between the ages of seven and 12, had changed its use to a school since at least 2016 and was visible on Google Maps. Old target lists had been reached for and noone had had the time or the inclination to check them before bombing them.

This is what you can expect from a Milo Minderbender presidency. It has been obvious, since at least the 1960s, that the US system requires enormous strength of purpose from its executive to hold its industrial-military complex in check. That is why so many of them have been so keen to install a Trump.

It feels as if, far from embracing the idea that our current economic priorities are indeed insane, as I fervently hoped seven years ago, we are instead doubling down on the insanity.

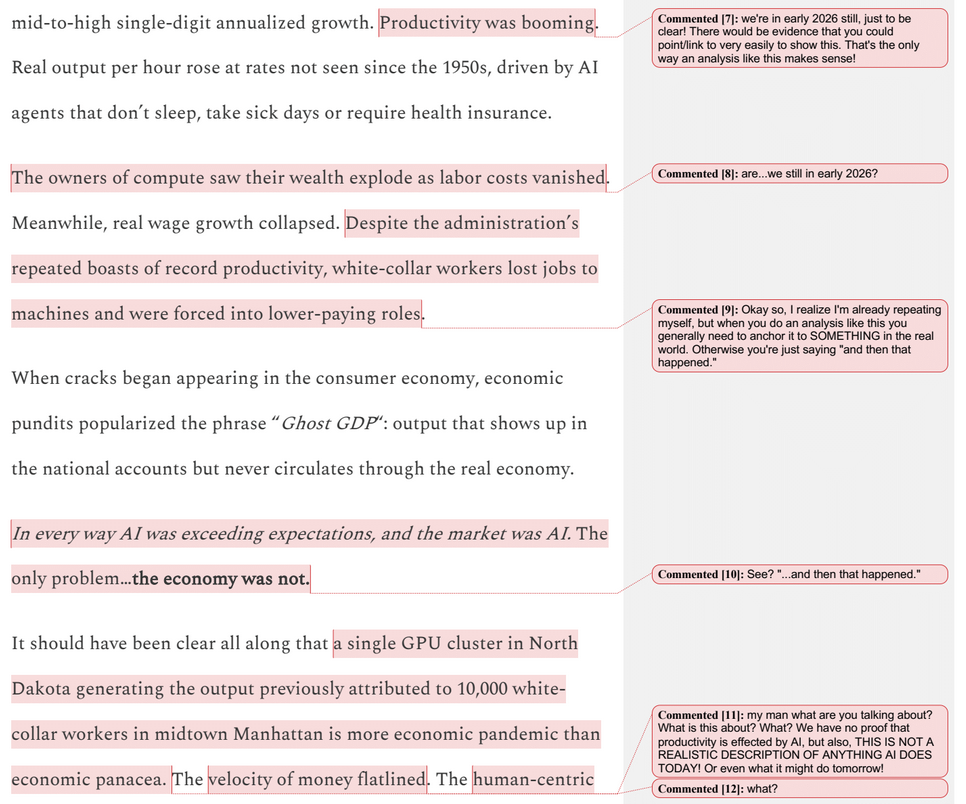

A week or so ago I referred to a “Thought Exercise” set in June 2028 “detailing the progression and fallout of the Global Intelligence Crisis” (ie science fiction), published on 23 February, which may have tanked the share price of IBM later that day. As I said then, the fall definitely happened, with IBM’s share price falling 13%, its biggest fall since 2000. I said then that the likelihood of the scenario portrayed was difficult to assess, but the speed with which the total economic collapse was described felt unlikely if not impossible. I would like to expand on that.

The main reason that the scenario was hard to assess was that it was not based on data or evidence at all. That is unavoidable for speculative fiction talking about things that are not currently happening, but when describing an economy only two years away where most of the processes described should be discernible to some extent already, it is totally avoidable.

Ed Zitron has done an excellent line by line take down of the Citrini piece here. Here is one page of that to give you a flavour:

However this lack of a link with anything tangible did not stop the financial markets panicking, which should cause us pause when relying on the financial markets’ valuation of projects, industries, government policies, etc.

Ed Zitron describes this kind of piece as analyslop: “when somebody writes a long, specious piece of writing with few facts or actual statements with the intention of it being read as thorough analysis”. It can then get picked up by other commentators which take it as their starting point for further analysis, often making it hard to see that the starting point had few if any data points. Here is an example, from Carlo Iacono, looking at what if just some of the Citrini pronouncements were true, with appendices detailing possible branching paths of outcomes, all generated by a large language model (LLM). And then people start studying the meta analysis, and it starts getting taken even more seriously, and put into models and pretty soon most of the analysis is being done on imagined risks rather than on ones which are already staring us in the face.

We have always had a problem keeping our society grounded in reality, think the 2003 Iraq War, where we went to war on a false assessment about Iraq’s possession of weapons of mass destruction, the 2008 financial crisis, where banks misunderstood the risks they were exposed to, and the last two and a half years, where we, for the most part, seem to have convinced ourselves we have not been facilitating a genocide in Gaza when we clearly have been. But this is only going to get worse with the AI systems which are being developed.

The rapid rise of artificial intelligence has served to dramatically increase the speed of information production while also eroding accuracy, making it difficult to differentiate between content that simply sounds confident and content that’s actually grounded in reality.

So where is AI currently? Well PwC’s global CEO survey from January this year had the following statement as the first bullet amongst its key findings:

Most CEOs say their companies aren’t yet seeing a financial return from investments in AI. Although close to a third (30%) report increased revenue from AI in the last 12 months and a quarter (26%) are seeing lower costs, more than half (56%) say they’ve realised neither revenue nor cost benefits.

That’s the reality. But the hype is much much more entertaining. My favourite spoof video of the AI future currently is this one, about the time where all most of us are good for is riding bicycles to supply the ever increasing energy needs of AI systems (click view in browser if you can’t see it):

And what about the financial journalists? The pieces describing our reaction to whatever is about to unfold economically have already been written. There are investor websites asking if the 2026 crash has already begun, while another recent article argues that “America has quietly become one of the world’s most shock‑resistant economies” (which seems unlikely to age well). What most financial journalists are more comfortable with are articles about how the warnings were ignored after the fact.

And the professions? Well the current overview of my own profession is probably reasonably represented by this piece from the Society of Actuaries in the United States. Unfortunately for them, Daniel Susskind, who is mentioned in the article, is currently suggesting, as part of his Future of Work lecture series for Gresham College, how the key to the sudden development in AI, after the “AI Winter” when progress seemed slow, was that we abandoned trying to make machines which thought and acted like humans in favour of focusing on completing tasks in any way possible. Increasingly we are now automating tasks where we can’t (or won’t) articulate how we do them. From Deep Blue‘s victory over Kasparov in 1997 to Watson winning jeopardy in 2011 to ImageNet beating humans at image recognition (although that is disputed), Susskind refers to this progress as the displacement of purists in favour of what he calls “The Pragmatic Revolution”. Pragmatism in this sense appears to be that we humans should just accept the consequences the people running these systems want. So, as his latest lecture “Work, out of reach” claims, people moving into cities to find work is a strategy which is no longer going to work for low skilled people:

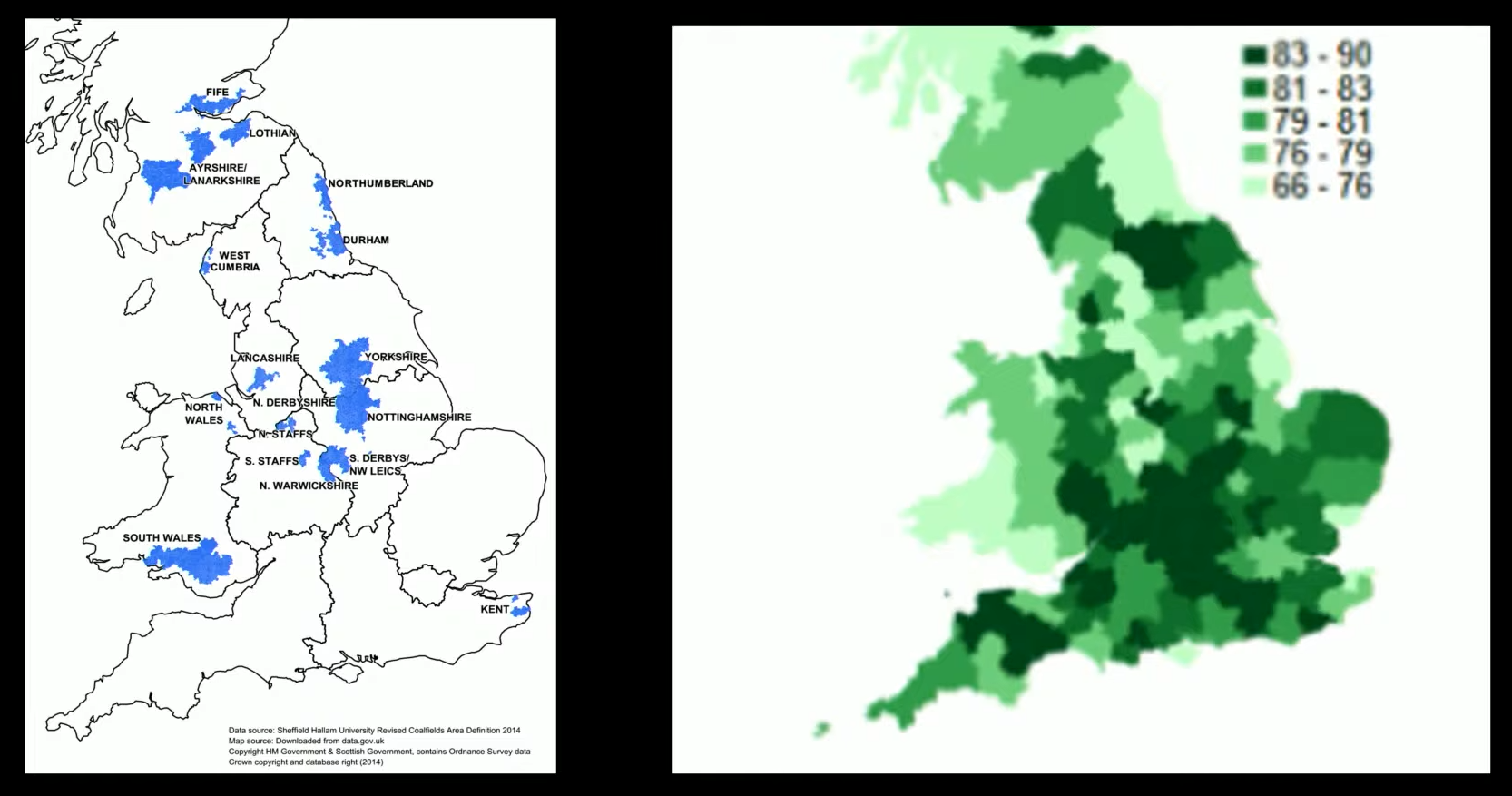

He then shows this graphic demonstrating the lack of recovery of big coal mining areas in the UK:

Source: Left – Sheffield Hallam University map of coal mining areas; Right – % employment from Overman and Xu (2022)

And finally he cites the notorious Policy Exchange piece from 2007, Cities Unlimited, whose thesis was that there is apparently no realistic prospect of regenerating towns and cities outside London and the South East.

Susskind talks about three forms of technological unemployment:

skills-mismatch, where your skills are mismatched to the work available. Education and training has always been the answer to this in the past.

place-mismatch, where the jobs are not where you have built your life. Some believe the answer should always be the one proposed by Norman Tebbit, who memorably told everyone in 1981, “I grew up in the 30s with an unemployed father. He did not riot. He got on his bike and looked for work.”

identity-mismatch, where according to Susskind, people are prepared to stay out of work to protect their identity, citing US men who won’t take “pink collar” work, China “rotten tail” kids, Japanese seishain-or-nothing and Indian Sarkari Naukri queues in India. Or perhaps they are just looking for work which is consistent with the idea of human dignity.

Susskind claims to have no answer to any of these as far as AI is concerned. They are, in his view, just the inevitable outcomes of his “Pragmatic Revolution”. It is the unthinking pursuit of more and more growth funded by capital less and less tethered to any territory, principle or purpose, where any grit in the machinery, be it unions or protestors or, increasingly, the wrong sort of government must be trampled underfoot. Anything which impedes the helter-skelter rush to more and more at greater and greater speed. It’s like our whole economy is run by this guy (press the view in browser link if you can’t see him) shouting “Ready, Aim, Fire!”:

But unskilled people will not be the only collateral damage of these unguided weapons. Take markets for instance. These are where people are exposed to risks and rewards based on underlying conditions they only partially understand. Greed and fear may be their main motivations, but gossip and group think are their main communication channels. They don’t need facts, particularly when so many of the facts are proprietary information not in the public domain. A plausible narrative will do. And plausible narratives are what LLMs will do for you in abundance.

And the more we reward people who can move fast, eg to spot an arbitrage opportunity, even at the risk of breaking things, rather than people who can make decisions which still look good decades from now, the more we are setting up the conditions for AI systems to be the go-to tool.

And put that together with an AI industry which desperately needs funding capital to keep arriving, ie one which is unbelievably highly motivated to push plausible narratives even when they know they are not grounded in reality, and you have a recipe for market-generated chaos.

And then we have Trump’s new war. Beware the people who are war gaming the Middle East at the moment on a range of LLMs (just stop and think for a moment about the bloodless inhuman impulse behind carrying out such an exercise rather than, I don’t know, talking to some actual people who live or have lived recently in and around the region). One of the worst offenders is Heavy Lifting banging on about what the three scenarios are for Operation Epic Fury. This is as bad as it sounds:

I tasked her [he is talking about Gemini Pro here] with doing a literature review on regime change (a term often used by the President but not a well-defined one), creating three scenarios of possible outcomes for which each was give a percentage probability, and a list of 20 items to examine for each scenario that covered political, economic, and cultural issues with a special focus on the political consequences in the U.S. and what this means for China, our biggest geopolitical rival.

But Gemini Pro wasn’t the only one involved in this. Two other humans were, Tim Parker and Ron Portante, trainers at the gym I go to. (Just as a personal aside, Tim was my coach in hitting six plates [345 pounds] on the sled last Friday and I have a video to prove it!) I was talking about the piece and Ron raised the issue of linguistic and cultural diversity in Iran. Tim did some real time research for me on his phone while I was burning real calories under his strict tutelage. This made me think I needed a background section on Iran. When I got him Gemini and I added it.

What you mean you belatedly realised you might need to have done some actual research into Iran rather than just generic research on regime change? I stopped reading at that point.

Meanwhile King’s College London have been carrying out war games more systematically using AI. Professor Kenneth Payne from the Department of Defence Studies led the study, which looked at how LLMs would perform in simulated nuclear crises. As Professor Payne said:

Nuclear escalation was near-universal: 95% of games saw tactical nuclear use and 76% reached strategic nuclear threats. Claude and Gemini especially treated nuclear weapons as legitimate strategic options, not moral thresholds, typically discussing nuclear use in purely instrumental terms. GPT-5.2 was a partial exception, limiting strikes to military targets, avoiding population centers, or framing escalation as “controlled” and “one-time.” This suggests some internalised norm against unrestricted nuclear war, even if not the visceral taboo that has held among human decision-makers since 1945.

This is not a Pragmatic Revolution. These AI systems cannot replace humans thinking about the future we want for humans in any way which is worth having. What they can do, if we let them, is accelerate our worst impulses and move us further away from considered reflective decision making.

But we will continue to use AI systems in the military because, as it turns out, it is very useful for low stakes admin. So although Lavender, the system used by the Israeli military to select targets in Gaza, made errors in 10% of cases and was therefore totally inappropriate to the task, there are lots of organisational logistical tasks where it is much quicker than the alternative and 10% error rates do not matter so much.

There is clearly an issue with what we decide to use these systems for. We need to be able to regulate the decisions which are particularly consequential. However the only way we seem to be considering for this at the moment is the human-in-the-loop model, like the humans spending around 20 seconds considering each target recommended by Lavender before authorizing a bombing. I have written about these before in the context of early career professionals in the finance industry, where the prospect seemed miserable enough:

They will be paid a lot more. However, as Cory Doctorow describes here, the misery of being the human in the loop for an AI system designed to produce output where errors are hard to spot and therefore to stop (Doctorow calls them, “reverse centaurs”, ie humans have become the horse part) includes being the ready made scapegoat (or “moral crumple zone” or “accountability sink“) for when they are inevitably used to overreach what they are programmed for and produce something terrible.

However it seems obvious to me that, in the context of dropping actual bombs on actual people, there is an even more serious problem with this model. As Simon Pearson (anti-capitalist musings) puts it:

The “human in the loop” requirement exists in military doctrine because international humanitarian law demands an accountable human decision-maker for lethal force. The laws of armed conflict require proportionality assessments, precautionary measures, distinction between combatants and civilians. All of these obligations attach to a human commander. The system cannot fulfil them. So a human must be present, and their presence must constitute a decision, regardless of whether any genuine decision was made.

What the institution needs from the analyst is not judgment. It is a signature. The signature converts a machine output into a human act. And a human act is what the law recognises, whether or not any judgment occurred. When the strike kills children, the chain of accountability runs to the analyst who approved the target: not to the system that identified it, not to the company that built the system, not to the doctrine that compressed the review window to ten seconds.

But whether we want to make money from exploiting a short term anomaly in a market, make our fellow humans redundant, prosecute a war on another group of fellow humans or “win” a war of mutual nuclear destruction, we need to retain the capacity for real human reflection within the decision-making processes we use. Not just a human-in-the-loop nor just the elites of tech companies deciding how the systems will be configured behind commercially confidential walls. These processes need democratic accountability every bit as much as our parliaments, councils, institutions and voting systems do.

Something infuriatingly slow, inclusive and deliberative giving recommendations which are then stress-tested for how they would perform on contact with reality, involving yet more people being serious and deliberative and taking their responsibilties more seriously than being a human-in-the-loop would ever allow. Our decision-making systems need more grit and less oil. AI is all oil.

The Actuary magazine recently had a debate about whether the underlying data or the story you wove around it was more important. I’m not sure there is always a clear distinction between the two, as Dan Davies rather neatly illustrates here, but my view is that, if a binary choice has to be made, it is always going to be the story. And there was a great example of this which popped up recently in the FT.

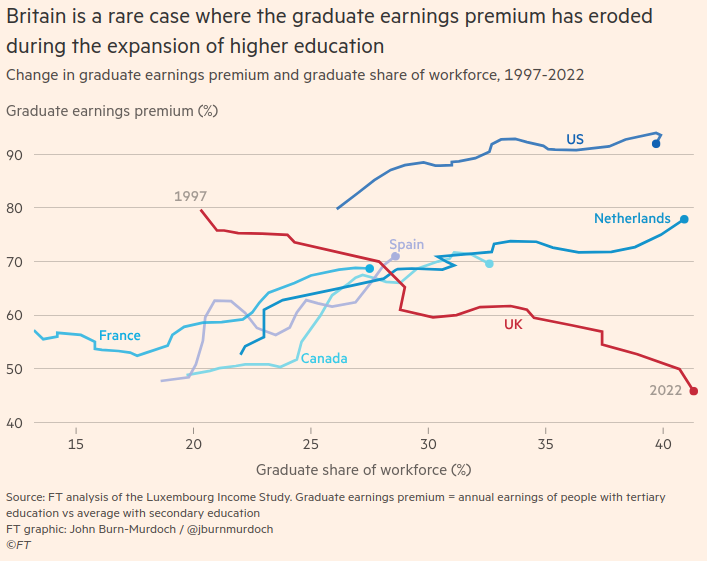

The FT article was ‘Is university still worth it?’ is the wrong question, by John Burn-Murdoch, with great graphs as usual by John. However, as is sometimes the case, I feel that a very different and more convincing story could be wrapped around the same datasets he is showing us.

The article’s thesis is as follows:

The graduate earnings premium, ie how much more on average graduates earn than non-graduates, has only fallen in the UK as the proportion going to university has risen. It has risen in other countries:

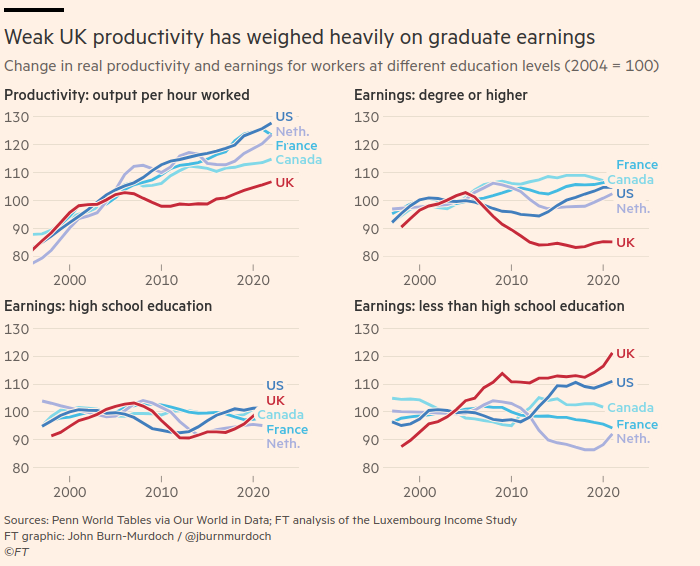

In the UK, we have had much weaker productivity growth than the other comparator countries, and also “the steady ramping up of the minimum wage has squeezed the earnings premium from the lower end too”:

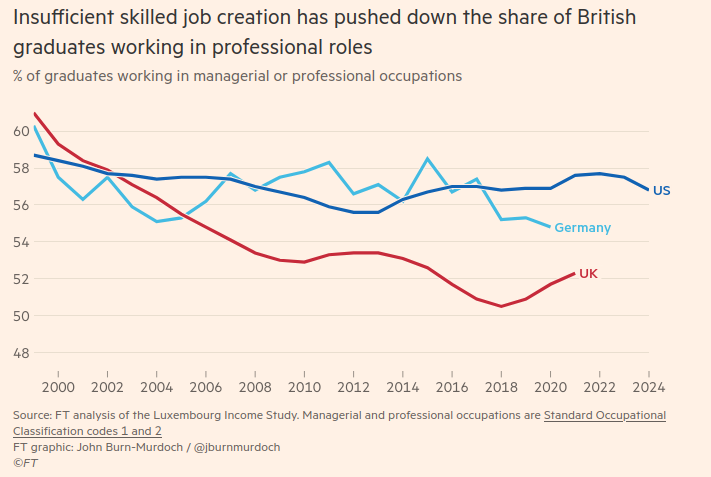

We have also had a much smaller increase in the percentage of managerial and professional jobs than a different group of comparator countries (they haven’t mentioned Germany before), meaning graduates are forced to take lower salaried jobs elsewhere:

So the answer according to the FT? We should focus on economic growth rather than “tweaking” higher education intake and funding. Then graduate earnings would be higher, student loans could be more generous(!) and students would have more chance of getting a good job.

Well perhaps. But here’s a different framing of the same data that I find more persuasive.

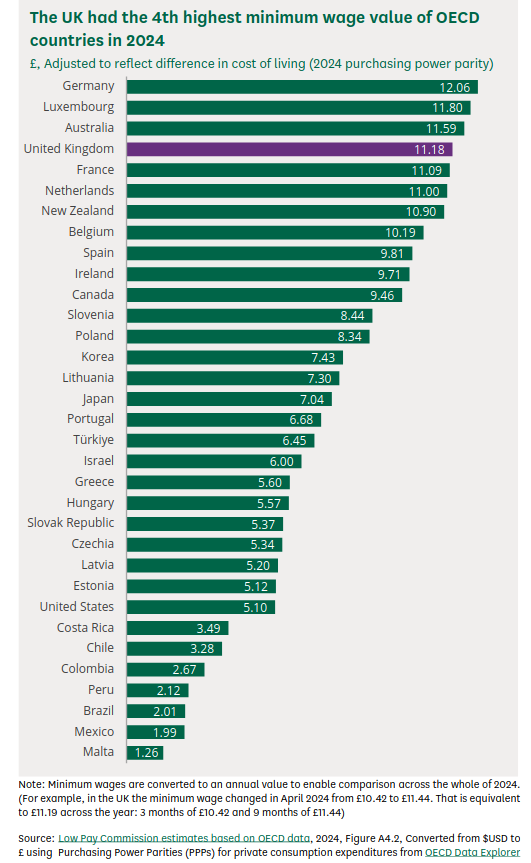

Let’s start by addressing that point about the minimum wage. According to the House of Commons Library report on this, the UK’s minimum wage is broadly comparable to that of France and the Netherlands, although higher than Canada’s and much higher than that of the United States. The employers who are the FT’s constituency would obviously like us lower down this particular chart:

The main economic framing here is the progress myth of the UK’s business community: economic growth. All problems can be solved if we can just get more economic growth. Apparently we need more inequality in pay between graduates and non-graduates which we can get by generating more economic growth. This is honest of them at least, although I don’t see much evidence that the economic growth they crave will go into skilled job creation rather than stock buy backs (according to Motley Fool, “Companies spent $249 billion on stock buybacks in Q3 2025, and $777 billion over the first three quarters of 2025.”).

There are a lot of problems with framing every economic question with respect to economic growth, memorably illustrated by Zack Polanski of the Green Party in this less than 3 minute video recently (I strongly recommend you watch it before you read on – click on the read in browser link if you can’t see it):

Economic growth is increasingly without purpose, wasteful of energy and poorly distributed. It is chasing outputs, literally any outputs, whatever the cost to the environment, our health system, our education system, our social support systems and our communities. Looking at the framing above, you can see that economic growth as currently pursued will always see anything which stops the concentration of wealth amongst the already wealthy, like a higher national minimum wage or a totally made-up concept like a lower graduate earnings premium (which in itself is a framing trying to make reducing inequality seem undesirable) as a problem. Lack of productivity growth, itself a proxy for this kind of economic growth (because if you ask why we need more productivity the answer is always to get more economic growth), is usually directed as a criticism at “lazy” UK workers, rather than under-investing and over-extracting UK business owners.

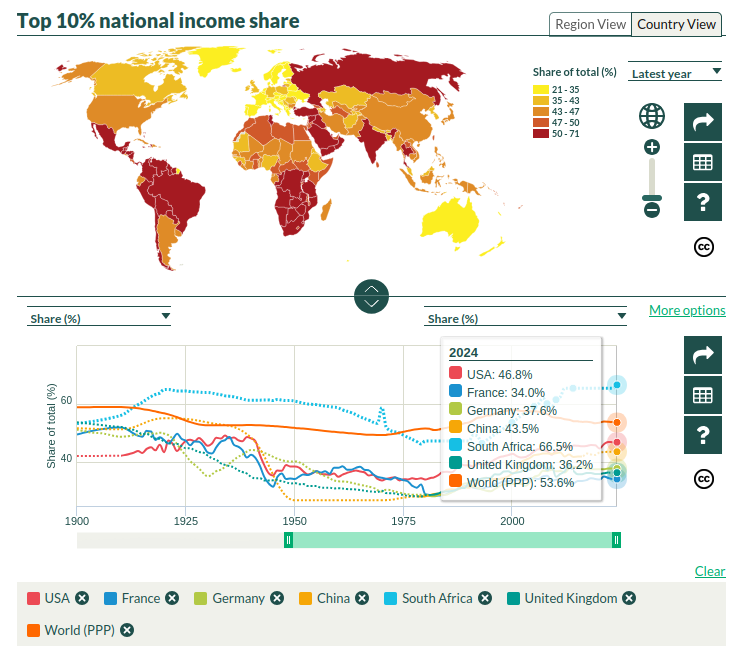

But what if, instead of economic growth, your progress myth was reducing inequality? Or growing equality within the economy?

Source: World Inequality Database wid.world

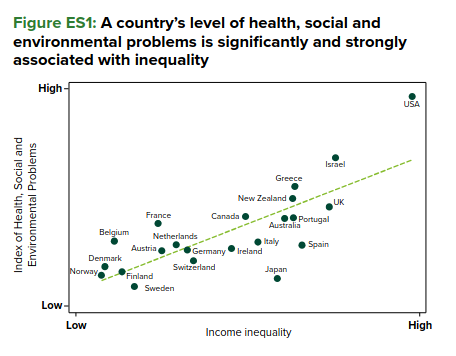

If you focused on inequality rather than economic growth, then you would find it correlates with everything we say we don’t want. Unlike economic growth, having equality as an aim actually has the advantage of having an evidence base for the claim that it improves society:

If you focused on inequality, then you would be pleased that we have had an increase in our minimum wage. You would think that the same FT article’s admission that UK graduates’ skills levels are higher than those in the United States was more important than something called a graduate earnings premium.

Burn-Murdoch is right to say asking whether university is worth it is the wrong question.

However economic growth is the wrong answer.

And I thought I would probably be stopping there for this week. But then something odd happened. A “Thought Exercise” set in June 2028 “detailing the progression and fallout of the Global Intelligence Crisis” (ie science fiction), published on 23 February, may have tanked the share price of IBM later that day. The fall definitely happened, with IBM’s share price falling 13%, its biggest fall since 2000, alongside smaller falls in other tech stocks.

Investors have recently seized on social media rumours and incremental developments by small AI companies to justify further selling, with a widely circulated blog post by Citrini Research over the weekend describing how AI could hypothetically push the US unemployment rate above 10 per cent by 2028, proving the latest catalyst.

The likelihood of the scenario portrayed is difficult to assess, but the speed with which the total economic collapse happens subsequently as described feels unlikely if not impossible. However the fact that the markets are this jittery tells us something I think. As Carlo Iacono puts it:

We are living through a period in which the gap between “plausible narrative” and “tradeable signal” has collapsed to nearly nothing. When a scenario feels real enough to model, and the underlying anxiety is already there waiting to be organised, fiction and forecast become functionally indistinguishable.

The data underlying the markets hasn’t changed, but the story has. I rest my case.

Politics is a bit depressing this week, so I thought instead I would focus on the asymmetry of our attitudes towards different high octane liquids.

I remember when I first got interested in wine. It was the early noughties and I was out at a restaurant in Cardiff called Le Cassoulet (no longer trading under that name I understand) with my then boss who liked to hit his expense account pretty hard from time to time. The sommelier seemed to know him quite well and scurried off to get him some particularly old claret to accompany the meal. I think it was from 1972 or thereabouts. I remember noting that it had a different colour (brown) from the red wine I was used to drinking and, when sipped, there were a lot of different flavours and smells competing for my attention. Something which I later heard described as “complexity”. From then on I realised that wine drinking could involve something a bit more than just something nice in a glass to accompany a meal.

The journey of alcoholic drinks from drinks to luxury consumer items and assets is nicely illustrated by the Bond franchise. There are a number of movies we could choose but let’s go for Goldfinger, shall we?

In the disappointing brandy scene from Goldfinger, we have this exchange between M, Bond and the Governor of the Bank of England, Colonel Smithers:

Smithers: “Have a little more of this rather disappointing brandy.”

M: “What’s the matter with it?”

Bond: “I’d say it was a 30-year-old Fine indifferently blended, sir…with an overdose of Bons Bois.”

M: “Colonel Smithers is giving the lecture, 007.”

Now first of all, that is clearly not what the Governor of the Bank of England looks like. As readers of this blog already know, he looks like this:

That scene is also notable for including a brief discussion of how the relative value of gold held at the US and British central banks at the time was used “to establish respectively the true value of the dollar and the pound”. In 1964 this would have been via the London Gold Pool, running between 1961 and 1968, by which a group of eight central banks including the United States Fed and the Bank of England agreed to cooperate in maintaining the Bretton Woods System of fixed-rate convertible currencies and defending the gold price. Ian Fleming’s book, written in 1959, predated this arrangement, but the anxieties about the gold market which led to its creation would have been very much around. So we still have the Governor (meeting Bond alone rather than with M) saying (during a lecture which went on for 10 pages):

We can only tell what the true strength of the pound is, and other countries can only tell it, by knowing the amount of valuta we have behind our currency.

Valuta is a rare word, from American English, for the value of one currency in terms of its exchange rate with another, and perhaps an odd one for the Governor of the Bank of England to use. But it is clear that Bond is sent after Goldfinger primarily for economic reasons (finding a way to smuggle large amounts of gold across borders threatens the Bank of England’s cosy little gold club) rather than because (spoiler alert) Goldfinger thinks nothing of murdering people (quite a lot of people in the case of Operation Grand Slam) who get in his way, cheating at golf, employing butlers with lethal bowlers, slicing through things with gold lasers and planting nuclear devices in Fort Knox. Released shortly after Ian Fleming’s death, it was the last Bond movie he saw in production.

It is the same film in which Bond obsesses about getting his favourite champagne (Dom Perignon 1953 – Bond was also someone not afraid to hit his expense account pretty hard from time to time) chilled to 38°F (3.3°C) before he gets bashed on the back of the head and the girl he is with (Goldfinger’s assistant, Jill Masterson, played by Shirley Eaton) gets sprayed from head to toe with gold paint. Perhaps more than any other brand, Bond linked luxury and high octane liquids of various kinds.

Skip forward a few decades and some of it has clearly stopped being something to drink at all, but instead a, very fragile, status asset for the very rich to demonstrate their status to each other. Here are the top prices achieved by wine at auction from one website, 8 of the 10 of them pre-dating both me and Goldfinger:

Contrast this with the way we have treated fossil fuels. As Luke Kemp points out in Goliath’s Curse:

We tend to forget that fossil fuels come primarily from long-dead plants and animals. These organisms died between 360 and 286 million years ago during the Carboniferous period, after capturing sunlight through photosynthesis or other means. It is that fossilised energy that we are consuming. According to one estimate, it would take 400 years of global photosynthesis to power the modern world for one year. It takes ninety-eight tons of organic matter buried during the Carboniferous to become just five litres of petrol. We are now a high-energy Goliath, powered by dead matter.

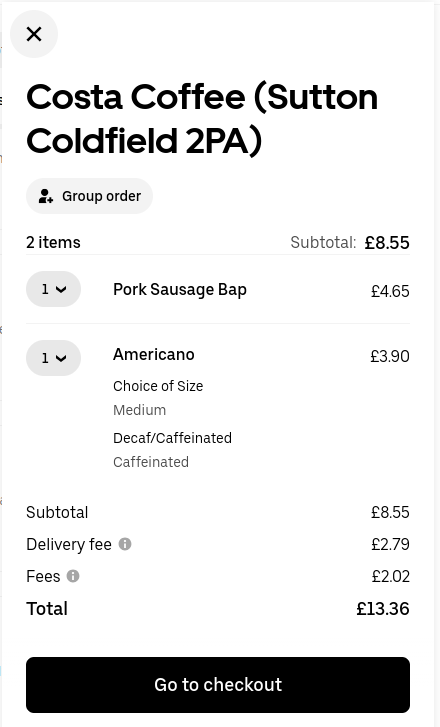

According to a petrol price checker from earlier this week, the garage closest to me currently sells unleaded petrol for £1.29 a litre. So 98 tones of organic matter curated for 300 million years retails for £6.45. That’s less than half the price of a sausage bap and a coffee from Costa via UberEats:

But apparently it’s still not cheap enough.

Most of the content from this article recommending eternal vigilance despite the cheapest prices for 5 years and the claims that “petrol is still 6p too high at the pumps” comes from Howard Cox, founder of FairFuelUK. Whose website includes this picture with a not-too-presumptious-claim-at-all below it:

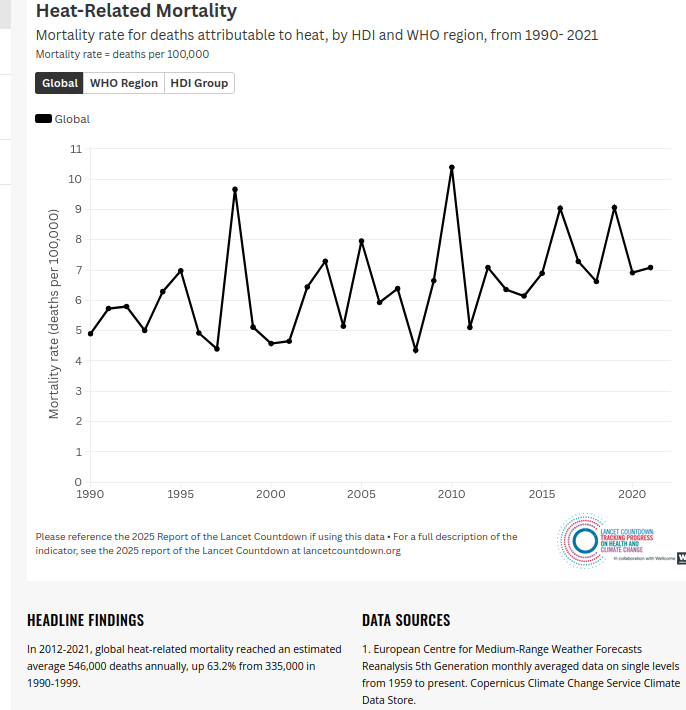

Even if you weren’t concerned with climate change or the health effects of petrol fumes in the air, this seems like a strange hill for anyone to be dying on. And dying we are. According to the 2025 Global Report of the Lancet Countdown average global heat-related mortality has now reached 546,000 pa, up 63% in just over 20 years:

And that’s just heat. A recent report from the Royal College of Physicians: A Breath of Fresh Airestimated 30,000 deaths from air pollution each year, of which car emissions form an important component.

By the time even the Bond franchise had started worrying about environmental concerns in 2008 with Quantum of Solace, a Somerset Maughamish short story converted into an attempt by a sinister organisation to become the water monopoly in Bolivia through underhand means, the iconic shot of the woman covered in gold had become a female consular employee (Strawberry Fields, played by Gemma Arterton) drowned in oil:

Our attitude to different types of high octane liquids has clearly been nuts in all kinds of ways for a long time. But it is just part of our political frostbite at the moment: we allow our living organisations and institutions to remain frozen in time because we have always done things that way, regardless of the living tissue we are killing in the process. From the endless cycle of public inquiries and ignored recommendations to our use of economics to rationalise things we have already decided to do to batting on with traditional exams: it seems we are just going to do what we are going to do. And freezing fuel duty now looks like it needs to be added to that list.

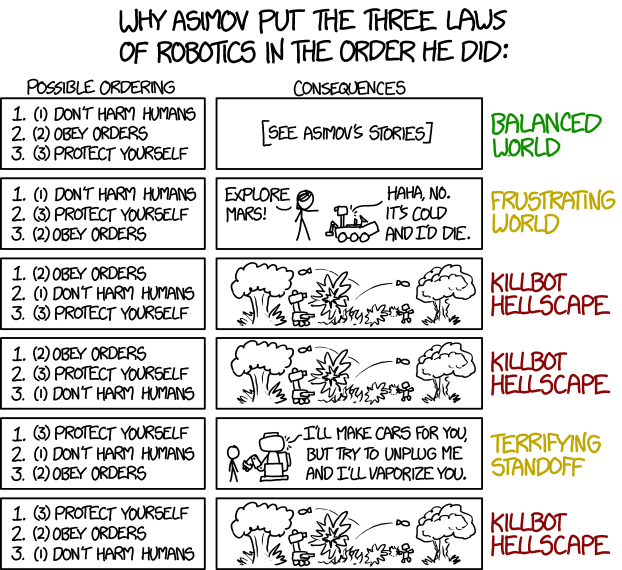

In ordering #5, self-driving cars will happily drive you around, but if you tell them to drive to a car dealership, they just lock the doors and politely ask how long humans take to starve to death.Source: https://m.xkcd.com/1613/

My attention was drawn this week to an article by Dario Amodei, co-founder of Anthropic (a spin off from OpenAI, which was co-founded by Elon Musk and heavily invested in by Microsoft so very much part of the Magnificent 7 architecture), the creator of the large language model Claude, called The Adolescence of Technology. It is hard to overemphasise how much I disagree with everything Dario has written here, but also useful in that it is a long article, which covers a lot of ground, and allows me to define my views in opposition to it.

The irritations start pretty much straight away. So Dario quotes from a science fiction classic (Carl Sagan’s First Contact), but then follows this up under the heading of “Avoid doomerism” with this:

…but it’s my impression that during the peak of worries about AI risk in 2023–2024, some of the least sensible voices rose to the top, often through sensationalistic social media accounts. These voices used off-putting language reminiscent of religion or science fiction, and called for extreme actions without having the evidence that would justify them.

Notice the word “sensible” doing the heavy lifting there. Only science fiction endorsed by Dario will be considered. Dario wants us to consider the risks of AI in “a careful and well-considered manner”, which sounds reasonable, but then his 3rd and final bullet under this (after “avoid doomerism” and “acknowledge uncertainty”) goes as follows:

Intervene as surgically as possible. Addressing the risks of AI will require a mix of voluntary actions taken by companies (and private third-party actors) and actions taken by governments that bind everyone. The voluntary actions—both taking them and encouraging other companies to follow suit—are a no-brainer for me. I firmly believe that government actions will also be required to some extent, but these interventions are different in character because they can potentially destroy economic value or coerce unwilling actors who are skeptical of these risks (and there is some chance they are right!).

So reflexively anti regulation of his own industry, of course. And voluntary actions by corporations, an approach to solving problems which has been demonstrated not to work repeatedly, is apparently “a no-brainer”. Also it is automatically assumed that government actions will destroy value. Only market solutions will be endorsed by Dario, pretty much until they have messed up so badly you are forced to bring governments in:

To be clear, I think there’s a decent chance we eventually reach a point where much more significant action is warranted, but that will depend on stronger evidence of imminent, concrete danger than we have today, as well as enough specificity about the danger to formulate rules that have a chance of addressing it. The most constructive thing we can do today is advocate for limited rules while we learn whether or not there is evidence to support stronger ones.

There is then the expected sales pitch about what he has seen within Anthropic about the relentless “increase in AI’s cognitive capabilities”. And then the man who warned about sensationalist science fiction is off:

I think the best way to get a handle on the risks of AI is to ask the following question: suppose a literal “country of geniuses” were to materialize somewhere in the world in ~2027. Imagine, say, 50 million people, all of whom are much more capable than any Nobel Prize winner, statesman, or technologist.

And the rest of the article is then off solving this imaginary problem in all its facets, rather than the wealth and power concentration problem that we actually have. The only legislation he seems to be in favour of seems to be something called “transparency legislation”, legislation which of course Anthropic would help to write.

However, after suggesting everything from isolating China and using “AI to empower democracies to resist autocracies” to private philanthropy as the solutions to his imagined problems, Dario finally and reluctantly concludes government intervention might after all be necessary as follows:

…ultimately a macroeconomic problem this large will require government intervention. The natural policy response to an enormous economic pie coupled with high inequality (due to a lack of jobs, or poorly paid jobs, for many) is progressive taxation. The tax could be general or could be targeted against AI companies in particular. Obviously tax design is complicated, and there are many ways for it to go wrong. I don’t support poorly designed tax policies. I think the extreme levels of inequality predicted in this essay justify a more robust tax policy on basic moral grounds, but I can also make a pragmatic argument to the world’s billionaires that it’s in their interest to support a good version of it: if they don’t support a good version, they’ll inevitably get a bad version designed by a mob.

That, by the way, is what Dario thinks of democracy: “a bad version designed by a mob” rather than the “good version” that he and his fellow billionaires could come up with in their own self interest. The mask has really slipped by this point. And the following section, on “Economic concentration of power”, just demonstrates that he has no effective answers at all that he deems acceptable on this. It’s just an inevitability for him.

This is what Luke Kemp’s excellent Goliath’s Curse refers to as a “Silicon Goliath”. Goliaths are dominance hierarchies which spread by dominating the areas around them. They need three conditions (which Luke calls “Goliath fuel”): lootable resources (ie resources which can be easily stolen off someone else), caged land (ie land difficult to escape from) and monopolizable weapons (ie ones which require processes which can be developed to give one society an edge over another). We are all Goliath-dwellers in “The West” now, looting resources from other countries in unequal exchanges which impoverish the Global South, with weapons (eg nuclear weapons) available only to the elite few countries and operating within the cages of heavily-policed national boundaries. The Silicon Goliath which is developing will have data as its lootable resource, mass surveillance systems providing its cages and monopolizable weapons such as killer drones. The resultant killbot hellscapes which people like Dario Amodei laughably imagine they have defences against through things like their Claude’s Constitution are almost pitiful in their inadequacy.

Nate Hagens takes Dario’s claims for AI’s cognitive capabilities much more seriously than me, and then considers the risks in a less adolescent way here. As he says:

And here’s what his essay has almost nothing about. Energy, water, materials, or ecological limits.

And also nowhere does Dario talk about the 99% of people who are just spectators in his world, other than to describe them as “the mob”. This is quite a blind spot, as Luke Kemp points out in his exhaustive study of the collapses of “Goliaths” over the last 5,000 years. “The extreme levels of inequality” predicted by Amodei in his essay are not just things we have to put up with, but the reasons the world he predicts is likely to be hugely unstable. Not created by AI, but accelerated by it. Kemp describes it as “diminishing returns on extraction”:

We see a pattern re-emerging across case studies. Societies grow more fragile over time and more prone to collapse. Threats that they had always faced such as invaders, disease and drought seem to take a heavier toll.

As societies grew bigger:

They still faced the underlying (and ongoing) problem of rising inequality creating societies where and institutions more extractive power was more concentrated.

And eventually:

The result is more extractive institutions creating growing instability, internal conflict, a drain of resources away from government, state capture by private elites, and worse decision-making. Society – especially the state – becomes more fragile. Private elites tend to take a larger share of extractive benefits. The state, and many of the power structures it helps prop up, then usually falls apart once a shock hits: for Rome it was climate change, disease, and rebelling Germanic mercenaries; for China it was often floods, droughts, disease and horseback raiders; for the west African kingdoms it was invaders and a loss of trade; for the Maya it was drought and a loss of trade; and for the Bronze Age it was drought, a disruption of trade and an earthquake storm.

The only real answer to combatting existential risks in the hands of adolescents like the Tech Bros is more democracy: over control of decision-making, over control of resources, over control of the threat of violence and over control of information. We are a long way from achieving these within our own particular Goliath at the moment, and indeed there is no sign at all that our elites are interested in achieving them. The Magnificent 7 are propping up the US stock exchange. The promise of perpetual economic growth is the progress myth of our time and leaders who do not provide it will lose the “Mandate of Heaven” in just the same way as Chinese rulers did when they were unable to prevent floods and droughts. Adam Tooze sees the signs of the inner demons of our elites starting to detach them from reality in the latest disclosures from the Epstein files:

Are we, like [Larry] Summers, fantasizing about stabilizing our desires and needs in an inherently dangerous and uncertain world? Are we kidding ourselves?

But, without those controls in place, we would need a lot more than Dario’s Anthropic playing nicely to allow this particular adolescent to grow up. And this is where I am forced to take Nate Hagens’ assessment more seriously. Because if our rulers’ Mandates of Heaven are dependent on eternal economic growth on their watch and they, rightly, think that this is not possible in our current non-AI-enhanced world but, wrongly, think it is possible in a future AI-enhanced world, then that is the way they are going to demand we go. And, if the Larry Summers fantasists really are kidding themselves, it may be very hard to talk them out of it.

Things have been moving quickly after weeks of just listening to Trump. Last week it was Davos and the other world leaders suddenly had something to say. Carlo Iacono rather neatly skewered them in advance with his Snow Globe of the Reasonable piece. As he says:

I keep returning to a phrase from the coverage: “globalization triage.” It captures something true. The old story, the one that said integration and openness would lift all boats, has been bleeding out for years. What is happening at Davos is not a recommitment to that story. It is an attempt to stabilise the patient long enough to extract remaining value before the next configuration emerges. The conversations about chips and data centres and export controls are not about innovation in any innocent sense. They are about who will control the commanding heights of the next economy, and the language of cooperation is the anaesthetic administered while the surgery proceeds.

And then, lo and behold, was Mark Carney, equally at home leading central bankers in 2008, appearing in thick jumpers on election night in Canada and now presenting Canada to the WEF as the enlightened way forward in the wake of Trump, without mentioning him once. He signalled Canada’s break with the rules-based order with a story told by Vaclav Havel about a greengrocer who put out a sign saying “Workers of the world unite” without believing a word of it. He says:

The system’s power comes not from its truth, but from everyone’s willingness to perform as if it were true, and its fragility comes from the same source. When even one person stops performing, when the greengrocer removes his sign, the illusion begins to crack. Friends, it is time for companies and countries to take their signs down.

He argued against the impulse for every country to look after itself, while finding it understandable:

A country that can’t feed itself, fuel itself or defend itself, has few options. When the rules no longer protect you, you must protect yourself.

Instead he argued for what he calls “variable geometry”:

…different coalitions for different issues based on common values and interests.

And in what, for me, was the most eye-catching part:

We are taking the sign out of the window. We know the old order is not coming back. We shouldn’t mourn it. Nostalgia is not a strategy, but we believe that from the fracture, we can build something bigger, better, stronger, more just. This is the task of the middle powers, the countries that have the most to lose from a world of fortresses and most to gain from genuine cooperation.

This was Carney staking a claim to leadership in a world working around the United States. And he sounds so reasonable within his snow globe that you can almost forget the impact of his last attempt at global leadership. Ann Pettifor, in her excellent review of the 2008 crisis 10 years after and its aftermath, quoted Professor Vogl of Princeton University:

the crisis has proved itself as a way to solidify the existing economic order…One can thus argue that the financial and economic state of emergency in recent years has given rise to …action that resembles a continuous coup d’Etat.” (INET Berlin, 2012.)

And as Iacono concluded his article:

The room in Davos is warm. The rooms beyond it are getting colder. The spirit of dialogue, whatever it once meant, now means the management of decline through the performance of concern. This is not a conspiracy. It is an emergent property of a system that has learned to stabilise itself by absorbing its critics and converting their language into its own. The only dialogue that would matter is the one that questions the room itself. That conversation is not scheduled.

The solutions proposed from within the Snow Globe will always sound measured and reasonable. The actors were mainly polished and impressive, all the better to contrast with the ramblings of Trump. The lines were well known. After all, as Samuel Miller McDonald’s Progress tells us, they have been delivered in one form or another for 5,000 years, when Mesopotamian cities came together to form the world’ first empires. McDonald describes the new approach as “parasitic energy capture”, both concrete in terms of resources required to survive and abstract in terms of the power structures within these new types of societies. As McDonald notes:

When the limits to their extraction of resources are exceeded, the parasitic systems must either suffer a crash or must invade and take the energy of a more distant ecology or society.

This type of parasitism was both justified and celebrated by the progress myths which accompanied each society: The Epic of Gilgamesh for the Babylonians, Zoroastrianism for the ancient Iranian kingdoms and empires, the creation myth of Judaism where, as McDonald puts it:

The book of Genesis provides the theological basis for dominion, but it also contains the promise of progress, which takes the shape of frontiers, or living space set aside for God’s chosen people, to be found in new land.

And on to the Greeks, with Thucydides’ History of the Peloponnesian Wars seeing Athenian civilisation as the pinnacle of human achievements. Sure enough, Carney was quoting him last week:

Right, as the world goes, is only in question between equals in power, while the strong do what they can and the weak suffer what they must.

Then on to the Roman Empire, legitimised by Virgil’s Aeneid, in which Jupiter says:

To the Romans I assign limits neither to the extent nor to the duration of their empire; dominion have I given them without end.

Then Rome embraced Christianity, with Constantine reasoning, according to McDonald, “that a monotheistic empire would be more effective at both unity and continued expansion than a more pluralistic or polytheistic one”.

Alongside Christianity, a new progress narrative was born in the 7th century to power an Islamic empire. As McDonald says:

Perhaps more than any that came before, the Islamic society that arose during this period mixed mythic forms of the progress narrative formula with secular ideas…that presaged those that would follow in the European Enlightenment.

And of course the European Enlightenment followed the expansion of parasitism from around 1400 from “a primarily regional, contiguous form to a global, disparate form”. As McDonald goes on to say:

This change was made possible first by the large oceanic vessels that could move goods, weapons, messages and colonists rapidly across large waterways, and then again by the deployment of fossilised energy in machines that could speed up extraction, communication, transportation and manufacturing even more.

What we are talking about here is global capitalism. And this brings me to one of the great mysteries, often referred to by Steve Keen, which I think I now have an answer to, of why economists have failed to properly incorporate the role of energy in production for so long. If mainstream economics now performs the role of the progress narratives of the past in justifying our continued parasitic expansion beyond all boundaries in pursuit of economic growth (which is now even acknowledged in official UK government documents like this one), then it needs to hide the role of parasitic energy capture from us in order to keep us doing it.

Which brings us back to the Snow Globe. I will leave the last word to Carlo Iacono:

The problems are structural, and I am not in a position to restructure them. The powerful will keep meeting, and the meetings will keep producing the facsimile of progress that forestalls the real thing. What I can do, what any of us can do, is refuse to be fooled by the snow globe. To name what is happening even when the naming has no immediate effect. To remember that legitimacy is not conferred by eloquence or venue, that a room full of billionaires discussing inequality is not the same as addressing inequality, that dialogue without the possibility of transformation is just noise arranged pleasingly.

I have spent many days in rooms with groups of men (always men) anxious about their future income, where I advised them on how much to ask their companies for. Most of my clients as a scheme actuary were trustees of pension schemes of companies which had seen better days, and who were struggling to make the necessary payments to secure the benefits already promised, let alone those to come. One by one, those schemes stopped offering those future benefits and just concentrated on meeting the bill for benefits already promised. If an opportunity came to buy those benefits out with an insurance company (which normally cost quite a bit more than the kind of “technical provisions” target the Pensions Regulator would accept), I lobbied hard to get it to happen. In many cases we were too late though, the company went bust and we moved it into the Pension Protection Fund instead. That was the life of a pensions actuary in the West Midlands in the noughties. I was often “Mr Good News” in those meetings, the ironic reference to the man constantly moving the goalposts for how much money the scheme needed to meet those benefits bills. I saw my role as pushing the companies to buy out funding if at all possible. None of the schemes I advised had a company behind them which could sustain ongoing pension costs long term. I would listen to the wishful thinking and the corporate optimism, smile and push for the “realistic” option of working towards buy out.

Then I went to work at a university, and found myself, for the first time since 2003, a member of an open defined benefit pension scheme. It was (and still is) a generous scheme, but was constantly complained about by the university lecturers who comprised most of its membership. I didn’t see any way that it was affordable for employers which seemed to struggle to employ enough lecturers, were very reluctant to award anything other than fixed term contracts, and had an almost feudal relationship with their PhD students and post docs. Staff went on strike about plans to close the scheme to future accrual and replace it with the most generous money purchase scheme I had ever seen. I demurred and wrote an article called Why I Won’t Strike. I watched in wonder when even actuarial lecturers at other universities enthusiastically supported the strike. However, over 10 years later, that scheme – the UK’s biggest – is still open. And I gained personally from continued active membership until 2024.

Now don’t get me wrong, I still think the UK university sector is wrong to maintain, unique amongst its peers, a defined benefit scheme. The funding requirement for it has been inflated by continued accrual over the last 8 years and therefore so has the risk it will spike at just the time when it is least affordable, a time which may soon be approaching with 45% of universities already reporting deficits. However the strike demonstrated how important the pension scheme was to staff, something the constant grumbling before the strike had led university managers to doubt. And, once the decision had been made to keep the scheme open to future accrual, I had no more to add as an actuary. Other actuaries had the responsibility for advising on funding, in fact quite a lot of others as the UCU was getting its own actuarial advice alongside that the USS was getting, but my involvement was now just that of a member, just one with a heightened awareness of the risks the employers were taking.

The reason I bring this up is because I detected something of the same position as my lonely one from the noughties amongst the group of actuaries involved in the latest joint report from the Institute and Faculty of Actuaries and the University of Exeter about the fight to maintain planetary climate solvency.

It very neatly sets out the problem, that the whole system of climate modelling and policy recommendations to date has been almost certainly underestimating how much warming is likely to result from a given increase in the level of carbon dioxide in the atmosphere. Therefore all the “carbon budgets” (amount we can emit before we hit particular temperature levels) have been assumed to be higher than they actually are and estimates for when we exhaust them have given us longer than we actually have. This is due to the masking effects of particulate pollution in the air, which has resulted in around 0.5C less warming than we would otherwise have had by now. However, efforts to remove sulphur from oil and coal fuels (themselves important for human health) have acted to reduce this aerosol cooling effect. The goalposts have moved.

An additional reference I would add to the excellent references in the report is Hansen’s Seeing the Forest for the Trees, which concisely summarises all the evidence to suggest the generally accepted range for climate sensitivity is too low.

So far, so “Mr Good News”. And for those who say this is not something actuaries should be doing because they are not climate experts, this is exactly what actuaries have always done. We started the profession by advising on the intersection between money and mortality, despite not being experts in any of the conditions which affected either the buying power of money or the conditions which affected people’s mortality. We could however use statistics to indicate how things were likely to go in general, and early instances of governments wasting quite a lot of money without a steer from people who understood statistics got us that gig, and a succession of other related gigs over the years ahead.

The difficult bit is always deciding what course of action you want to encourage once you have done the analysis. This was much easier in pensions, as there was a regulatory framework to work to. It is much harder when, as in this case, it involves proposing changes in behaviour which are ingrained into our societies. If university lecturers can oppose something that is clearly not in the long term financial interests of their employers and push for something which makes their individual employers less secure, then how much more will the general public resist change when they can see no good reason for it.

And in this regard this feels like a report mostly focused on the finance industry. The analogies it makes with the 2008 financial crash, constant comparisons with the solvency regulatory regimes of insurers in particular and even the framing of the need to mitigate climate change in order to support economic growth are all couched in terms familiar to people working in the finance sector. This has, perhaps predictably, meant that the press coverage to date has mostly been concentrated in the pension, insurance and investment areas:

However in the case of the 2008 crash, the causes were able to be addressed by restricting practices amongst the financial institutions which had just been bailed out and were therefore in no position to argue. Many of those restrictions have been loosened since, and I think many amongst the general public would question whether the decision to bail out the banks and impose austerity on everyone else is really a model to follow for other crises.

The next stage will therefore need to involve breaking out of the finance sector to communicate the message more widely, perhaps focusing on the first point in the proposed Recovery Plan: developing a different mindset. As the report says:

This challenge demands a shift in perspective, recognising that humanity is not separate from nature but embedded in it, reliant on it and, furthermore, now required to actively steward the Earth system. To maintain Planetary Solvency, we need to put in place mechanisms to ensure our social, economic, and political systems respect the planet’s biophysical limits, thus preserving or restoring sufficient natural capital for future generations to continue receiving ecosystem services…

…The prevailing economic system is a risk driver and requires reform, as economic dependency on nature is unrecognised in dominant economic theory which incorrectly assumes that natural capital is substitutable by manufactured capital. A particular barrier to climate action has been lobbying from incumbents and misinformation which has contributed to slower than required policy implementation.

By which I assume they mean this type of lobbying:

And this is where it gets very difficult, because actuaries really do not have anything to add at this point. We are just citizens with no particular expertise about how to proceed, just a heightened awareness of the dangers we are facing if we don’t act.

But we can also, as the report does, point out that we still have agency:

Although this is daunting, it means we have agency – we can choose to manage human activity to minimise the risk of societal disruption from the loss of critical support services from nature.

This point chimes with something else I have been reading recently (and which I will be writing more about in the coming weeks): Samuel Miller McDonald’s Progress. As he says “never before have so many lives, human and otherwise, depended on the decisions of human beings in this moment of history”. You may argue the toss on that with me, which is fine, but, in view of the other things you may be scrolling through either side of reading this, how about this for a paragraph putting the whole question of when to change how we do things in context:

We are caught in a difficult trap. If everything that is familiar is torn down and all the structures that govern our day-to-day disintegrated, we risk terrible disorder. We court famines and wars. We invite power vacuums to be filled by even more brutal psychopaths than those who haunt the halls of power now. But if we don’t, if we continue on the current path and simply follow inertia, there is a good chance that the outcome will be far worse than the disruption of upending everything today. Maintaining status-quo trajectories in carbon emissions, habitat destruction and pollution, there is a high likelihood of collapse in the existing structure anyway. It will just occur under far worse ecological conditions than if it were to happen sooner, in a more controlled way. At least, that is what all the best science suggests. To believe otherwise requires rejecting science and knowledge itself, which some find to be a worthwhile trade-off. But reality can only be denied for so long. Dream at night we may, the day will ensnare us anyway.

One thing I never did in one of those rooms full of anxious men was to stand up and loudly denounce the pensions system we were all working within. Actuaries do not behave like that generally. However we have a senior group of actuaries, with the endorsement of their profession, publishing a report that says things like this (bold emphasis added by me):

Planetary Solvency is threatened and a recovery plan is needed: a fundamental, policy-led change of direction, informed by realistic risk assessments that recognise our current market-led approach is failing, accompanied by an action plan that considers broad, radical and effective options.

This is not a normal situation. We should act accordingly.

So this is my 42nd blog post of the year and the 8th where I have referenced Cory Doctorow. Thought it was more to be honest, so influential has he been on my thought, particularly as I have delved deeper into what, how and why the AI Rush is proceeding and what it means for the people exiting universities over the next few years.

Yesterday Cory published a reminder of his book reviews this year. He is an amazing book reviewer. There are 24 on the list this year, and I want to read every one of them on the strength of his reviews alone.

I would like to repay the compliment by reviewing his latest book: Enshittification (the other publication this year – Picks and Shovels – is also well worth your time by the way). Can’t believe this wasn’t the word of the year rather than rage bait, as it explains considerably more about the times we are living in.

I have been a fan of Doctorow for a couple of years now. I had had Walkaway sat on my shelves for a few years before I read it and was immediately enthralled by his tale of a post scarcity future which had still somehow descended into an inter-generational power struggle hellscape. I moved on to the Little Brother books, now being reenacted by Trump with his ICE force in one major US city after another. Followed those up with The Lost Cause, where the teenagers try desperately to bridge the gap across the generations with MAGA people, with tragic results along the way but a grim determination at the end “the surest way to lose is to stop running”. From there I migrated to the Marty Hench thrillers, his non-fiction The Internet Con (which details the argument for interoperability, ie the ability of any platform to interact with another) and his short fiction (I loved Radicalised, not just for the grimly prophetic Radicalised novella in the collection, but also the gleeful insanity of Unauthorised Bread). I highly recommend them all.

I came to Enshittification after reading his Pluralistic blog most days for the last year and a half, so was initially disappointed to find very little new as I started working my way through it. However what the first two parts – The Natural History and The Pathology – are is a patient explanation of the concept of enshittification and how it operates assuming no previous engagement with the term, all in one place.

Enshittifcation, as defined by Cory Doctorow, proceeds as follows:

First, platforms are good to their users.

Then they abuse their users to make things better for their business customers.

Next, they abuse those business customers to claw back all the value for themselves.

Finally, they have become a giant pile of shit.