The year is 2100. Earth is approaching a peak population of 9.5 billion people. Despite some notable progress in decarbonising our activities and more progress on carbon capture of various types than expected 80 years ago, overall we have not managed to shift much off the Intergovernmental Panel on Climate Change (IPCC) middle-of-the-road shared socioeconomic pathway (SSP2). Some countries have done much better than others, with income inequality a problem both within and between them. Carbon emissions stayed fairly level until 2050 before starting to fall, but net zero has still not been achieved.1

Temperatures have risen by 2.7 degrees compared to pre-industrial levels. Africa has split between a north which has seen a recovery of rainfall and a south which is no longer habitable for humans. The Indian monsoon rains have failed. The Himalayan glaciers providing the waters of the Indus, Ganges and Brahmaputra, the Mekong, Yangtze and Yellow rivers have reduced by 90% from their pre-industrial levels.

The Amazonian rain forest basin has dried out completely. In Brazil, Venezuela, Columbia, East Peru and Bolivia life has become increasingly difficult due to wild fires. Drought is now permanent in the sub-tropics and Central America. Australia has become the world’s driest nation.

In the US Gulf of Mexico high sea temperatures drive 180+ mph winds.2 Flooding is widespread with sea levels having risen by 0.6 metres on average compared to 2020.3 Many plant species have become extinct as they were unable to adapt to such a sudden change in climate.

Food prices continue to soar, with temperatures, droughts and the inundation of arable land adversely affecting many crops. Massive migrations have led to increasingly severe military and police responses from the most popular destination countries. There is fear that we have not yet seen the end of the terrible costs of climate change, with temperatures continuing to rise.

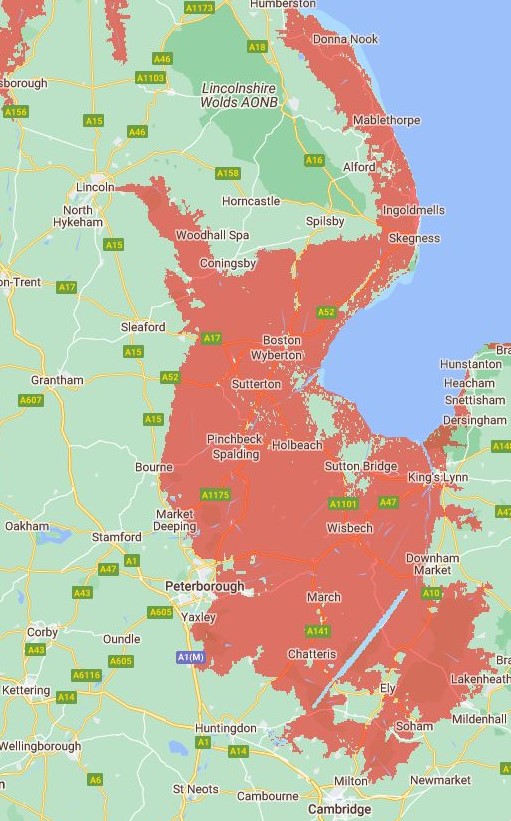

England has a new Eastern coastline, which became a certainty once the decision was taken that the cost benefit analysis did not justify the expense on the massive coastal defences which would have been required to prevent it. Sleaford is now a seaside town. Birmingham is the only major city which has not been significantly affected by sea level rise4 and there are calls for the capital to be moved there. However London hangs grimly on following the failure of the Thames Barrier in the 2040s. An Intertidal Property Pricing Index (IPPI) has sprung up, which sucks in money as investors bet on the development opportunities in the aftermath of the catastrophe.5

This, or something like it, is the future we are currently on track for but none of us wants. So let’s change the trajectory.

Notes:

The IPCC’s SSP2 narrative description.

Mark Lynas, Six Degrees: Our Future On A Hotter Planet, Harper Perennial, 2008 for the scientific consensus at the time on the consequences of 3 degrees warming

https://sealevel.nasa.gov/ipcc-ar6-sea-level-projection-tool?type=global (accessed 5 July 2023)

https://coastal.climatecentral.org/ (accessed 5 July 2023) for the maps of England following 2.7 degrees warming by 2100 following current trajectories

IPPI borrowed from Kim Stanley Robinson’s depiction of a future New York after two pulses totalling 15 metres (50 feet) of sea level rise in New York 2140, Orbit, 2018

For those of you who have ever bought or sold a house (and I realise that that is a dwindling proportion as we move down the age ranges), it occurred to me that the UK increasingly resembles the worst kind of vendor. The sort that removes the lightbulbs and the doorknobs before giving up possession.

Harold Macmillan referred to Margaret Thatcher’s Government “selling off the family silver” in response to the widespread privatisations of public assets at the time. This Government has gone further, denying funding to the health and social security safety net we all rely on to such an extent that, as Health Equity in England: The Marmot’s Review 10 Years On found in 2020:

people can expect to spend more of their lives in poor health;

improvements to life expectancy have stalled, and declined for women in the most deprived 10% of areas;

the health gap has grown between wealthy and deprived areas; and

living in a deprived area of the North East is worse for your health than living in a similarly deprived area in London, to the extent that life expectancy is nearly five years less.

However it is even worse than that. I once bought a house from a man who had done all of his own plumbing, despite being a telephone engineer. He proudly took me up to the airing cupboard, where the boiler room displayed piping of complexity which would not have been out of place on a nuclear submarine.

“Everything has its own stop cock.” He said. He might even have called them isolation valves. I just thought of how many different leaks were possible from what he had constructed.

And so it proved. We had a plumber on speed dial before long and, with every new job he undertook for us, most of which was to undo the “work” of which the former owner had been so proud, he used to intone “what a man”, more to himself than to us.

Brexit, even as its architects start to disavow it in the face of the increasingly overwhelming evidence of the bullet holes in our own feet, is our home-made plumbing. And I am sure that there are any number of people around the world, looking at us and intoning “what a man” to themselves. It no longer matters to most of us how much the Brexiteers think they have buffed up their sovereignty isolation valves. Every week brings a new story about another leak of what Macmillan endearingly referred to as our “treasure” that it has enabled.

On immigration, we are like that house on the street which noone from the area wants to go anywhere near. Neighbours only reluctantly enter into any kind of dispute about who should replace the shared fence. There is a huge-sounding dog which barks at you fiercely if you venture up the driveway, on which the only car is on bricks. It feels like, if we were to ultimately die as a nation, noone would notice for years until the smell coming from inside became too much for anyone to ignore any more.

Anyway, enough of all that. I am off to the Hay Festival tomorrow for my annual infusion of ideas, erudition and words just flowing all around me. And so I must leave you with a book recommendation. I will be taking The Golden Mole by Katherine Rundell with me, a brilliant beautifully illustrated book (illustrations by Talya Baldwin) with each chapter focused on a different endangered species. Sounds bleak? No! The writing is so good that you are soon just overwhelmed by the richness you hadn’t even been aware of and might otherwise never have been. I have been reading it very slowly as I really do not want it to end. As Katherine says about The Human at the end of the book, with a different take on treasure:

For what is the finest treasure? Life. It is everything that lives, and the earth upon which they depend: narwhal, spider, pangolin, swift, faulted and shining human. It calls out for more furious, more iron-willed treasuring.

I have this book because Katherine described it so compellingly in an interview at the Hay Winter Festival (a smaller one in November each year). She has also written a book about John Donne, the metaphysical poet, called Super-Infinite. I had not considered until now that I was remotely interested in John Donne, but I also cannot imagine that the week will pass without me buying this and reading it too.

I recently finished reading Chasm City by Alastair Reynolds, which I highly recommend. In it, sufficiently rich people have been able to buy a programme of treatments which make them immortal. Not that they can’t die, but they needn’t if they’re careful. Good science fiction, I thought.

Then I read Paul Kitson’s (the new UK Head of Pensions Consulting at EY) piece on LinkedIn where he wrote (bold mine):

Pension schemes, corporate sponsors, members – everyone, in fact – must now contend with a forward looking plan that (somehow!) considers on one side the possibility of future pandemic outbreaks shortening life expectancy, and on the other side the many £billions being spent on ‘regenerative medicine’ (AKA “the ending of ageing” or “escape velocity for death”!).

So perhaps not entirely, I thought.

In Chasm City, the immortals who live in “the Canopy” have two main problems:

Hanging on to their wealth and, if possible, increasing it, as forever is a long time to finance.

Boredom.

One particular group amuse themselves by hunting poor people in “the Mulch” (lower level where the poor live). Others indulge in increasingly dangerous pastimes to inject some urgency into the otherwise featureless expanse of their lives. No wealth moves from the Canopy to the Mulch, not even in a trickle.

I am just finishing Do Androids Dream of Electric Sheep by Philip K Dick (a classic, I know, but I hadn’t read it before, although I have seen Bladerunner). One of the features of the post-apocalyptic world of 1992 described are “mood organs” which allow you to dial up a given mood at any time, eg 481 is “awareness of the manifold possibilities open to me in the future” whereas 888 is the desire to watch TV, no matter what’s on it. Again, good science fiction, I thought.

Then I read a piece in this months’ Actuary magazine called Apt apps, about doctors being recommended by NICE to offer patients with insomnia the Sleepio app as an effective and cost-saving alternative to sleeping pills. So perhaps not entirely, I thought.

The first book was written in 2001 and the second in 1968, so it would seem that lead times are variable.

Both books deal with the fragility of identity, whether via memory implants and religious viruses in Reynolds’ book or how we go about separating androids from people from “chickenheads” in Dick’s. The divisions between the life experiences of the different groups are so stark, but it is the characteristics of the people in them which takes up everyone’s time and attention in both books, rather than the structure of the societies which create such extreme winners and losers. Which suddenly doesn’t feel like science fiction at all.

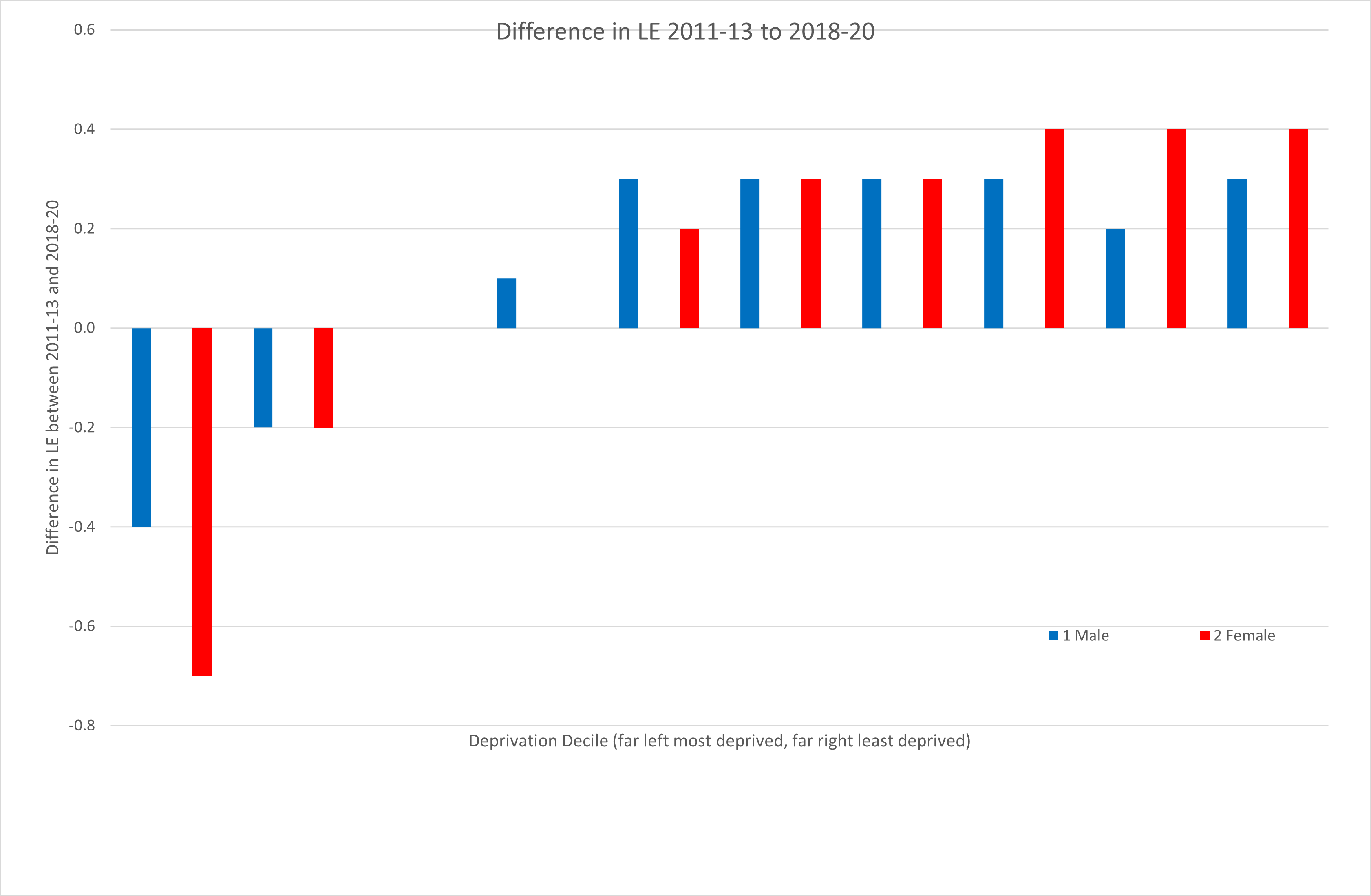

Meanwhile what has happened to England’s life expectancies by decile of deprivation in the last 10 years?

Source: ONS https://www.ons.gov.uk/peoplepopulationandcommunity/healthandsocialcare/healthinequalities/bulletins/healthstatelifeexpectanciesbyindexofmultipledeprivationimd/2018to2020#health-state-life-expectancies-data

So not quite immortality yet at the top, but inequality is clearly worsening in life expectancy. The Government Actuary’s Department gave an upbeat view last year on what the impact of the recent Levelling Up White Paper might be. Others are upbeat too.

However the Government’s track record is not good on inequality. Sir Michael Marmot produced the Marmot Review on health inequalities in the UK in 2010 and then followed this up with a review of what progress had been made 10 years later. As he points out in his recent interview in The Actuary:

Health spending fell from around 42% to 35% during the 2010s. He notes that this reduction was carried out in a regressive way: “There has been a 16% reduction in health spending for the most affluent, but a 32% reduction for the most deprived groups.” In addition, he says, while unemployment fell over the course of the decade, the income of employed people also went down – so the proportion of people living in poverty rose, as did child poverty.

These are the kinds of interventions that matter for most people rather than sleep apps or regenerative medicine to achieve escape velocity from death. And they are definitely not science fiction.

In each children spent hours preparing their own personal tributes to the focus of the weekend. Parents arranged accommodation. Face paints were in profusion. Cardboard constructions abounded. There were placards and banners and flags.

One got minute by minute coverage in hushed tones, with talking heads running out of things to say after 6 hours or so and then needing to start projecting what various people, having their every movement and facial tic filmed, might be betraying in a momentary expression. The other one was almost totally ignored, despite both events occupying almost exactly the same space in central London.

Imagine if the media priorities had been reversed:

“And, as the man with the giant mosquito on his head, slowly makes his way around Parliament Square, we reflect on how many hours must have gone into constructing that mighty insect. And now we see the scientists, garbed in their traditional white coats, making the point that no nature means no future. What a riot of colour it is and so many volunteers have given up their time, not only today but in the months of preparation for the Big One. So, Sir David, are you surprised by the number of children in the procession today?” “Not really, Huw…”

“Meanwhile in other news, police arrested a Mr Charles Windsor and his wife Camilla at their home. Police seized several crowns, an orb, sceptres, rings, some very large chairs and other paraphernalia which could be involved in coronation activity. Royalists claimed that the police had been ridiculously heavy-handed. The police said that their actions had been entirely proportionate.”

In Christopher Clark’s new book about the revolutions throughout Europe in 1848, Revolutionary Spring, he talks about the origins of radicals and liberals in opposition to the establishments of the day, divisions which still seem to be with us today. But it is our Government which is radical, prepared to do great violence to the status quo, the opposition which seems to be liberal, bogged down in endless arguments about tiny differences, and the BBC which appears to be left on its own representing what it sees as the current Establishment.

Now there will be many who say that journalists should not be involved in defending any status quo, and I can understand that. However it can also be argued that a state broadcaster like the BBC does have some responsibilities in this respect. But which status quo do you defend?

The Government’s agenda is problematic – it’s not just about the lying and the corruption, but the constant changing of position, the most obvious being the Kwarteng fiscal event in the autumn. Climate protesters are remarkably consistent by comparison, not surprisingly really as the limits imposed by physics are not changing with each quarter. And their focus of sustainability is surely the most critical part of any status quo which needs defending, ie the ability of the planet to support life in all of its forms.

Television is extremely good at focusing our attention on something, and away from something else. This is why companies spend so much on television advertising and why our televised sports halls and pitches and the combatants within them are festooned with logos and messages from a myriad of sponsors. However, the Communications Act 2003 prohibits political advertising, which includes campaigning for the purposes of influencing legislation or executive action by local or national (including foreign) governments. The BBC have interpreted this as not allowing any form of protest to be visible during televised sporting events (most recent example being the Just Stop Oil protest with the orange powder at the World Snooker Championship), an event for which the title sponsor is Cazoo, Europe’s leading online car retailer. Similarly, the police have said that one of the considerations in their level of policing response to the Republic demonstrations this weekend, including pre-arrests before the procession or any protest had taken place, had been the wall-to-wall television coverage of the event.

46% of the UK population are very or extremely worried about climate change, but the biggest demonstration in the UK in the climate movements’s history was not covered on television at all. 62% of the UK population support the monarchy and we get all the main channels turned over to coronation coverage. I think what I am calling for is a bit more balance here, something we used to think, with some pride, was a national characteristic.

Source: https://commons.wikimedia.org/wiki/File:Green_frog_(Pelophylax_esculentus_complex)_Danube_delta.jpg by Charles J. Sharp, CC BY-SA 4.0 https://creativecommons.org/licenses/by-sa/4.0, via Wikimedia Commons

However, my stand out book this year is none of these. I have often heard people say they wish they had written some book or other, and I have never understood it until now. This is the book I would hope that a better version of me might have written in a parallel universe. Fortunately for you, Simon Sharpe has written Five Times Faster in this universe, and I am so glad he has.

Five Times Faster is funny, constantly surprising and has reframed my entire attitude to the climate crisis and what can be done about it. Perhaps it had more intensity for me as I read most of it aboard the XR bus from Birmingham down to London last weekend, but it has given me more hope for what Kim Stanley Robinson calls “dodging the mass extinction event” than I have had for some time.

Amongst the many wonders of this book is to reframe the time-worn story of the frog sitting in water which is slowly coming to the boil as a series of conversations with its science adviser, its economics adviser and its diplomatic adviser. To do it full justice you will need to read the book, but the gist of it goes as follows:

First of all, the frog asks its science adviser to investigate whether the water really is getting warmer. The science adviser confirms that it is, and also predicts that, in 5 minutes’ time, it will be a further 2o warmer, plus or minus 1o. The frog says it didn’t want a prediction, it wanted a risk assessment. It takes a while to get the science adviser to understand what this is but then, when asked what’s the worst that could happen, the adviser blurts out “That’s easy. You could boil to death.” In response to the question of how likely that is to happen, the adviser says that it would be very unlikely after 5 minutes, more likely than not after 10 and after 15 a certainty. So the frog now realises it needs to jump out of the pot.

The frog now turns to its economics adviser to ask how it should go about it. The economics advisor does a cost benefit analysis by first calculating the energy cost per cm of moving up the pot away from the water, converting this first into food consumption and then money, and equating this with the frog’s willingness to pay for not being boiled, which is derived from its air conditioning bill. The most efficient solution turns out to be to climb 4.73 cm up the side of the pot. Worried that it would just be replacing the risk of being boiled with one of being steamed to death, the frog ignores its economics adviser and jumps out of the pot.

Finally the general problem of the frogs and the relentlessly boiling water is put to the negotiators for a diplomatic solution. The sides of the pot are too high by now for most of them to jump out. The negotiators tell them they just need to raise their ambition and that this is the only game in town. The consequences of not accepting that analysis and looking at alternative salientian strategies make up the final third of the book.

I cannot recommend it highly enough. If enough people read it and act upon it, perhaps we can avoid this:

In Simon Sharpe’s great new book Five Time Faster, he points out that, if we are going to decarbonise everything, “it’s not just the physical plumbing of the global economy that needs to be replaced, but the intellectual plumbing.” In a blog post from January, Three less visible battles to win, Simon mentions three targets in particular for this intellectual plumbing:

Infrastructure that makes sure heads of government know just how bad climate change could get;

Ideas in economics that exert a critical influence over governments’ policy decisions; and

Institutions in diplomacy that will get the job done.

The first one means targeting the Integrated Assessment Models which have informed so much of our hesitancy and inappropriate prioritisations over the last 20 years where climate is concerned. I have written about this several times before, and this is something actuaries can contribute to much more in the future.

And the third one will I believe become much more tractable once the intellectual tide starts to change.

I will be heading down with my banner to London tomorrow for Extinctions Rebellion’s Big One, alongside 90 other organisations united in demonstrating for a survivable future. Hope to see you there!

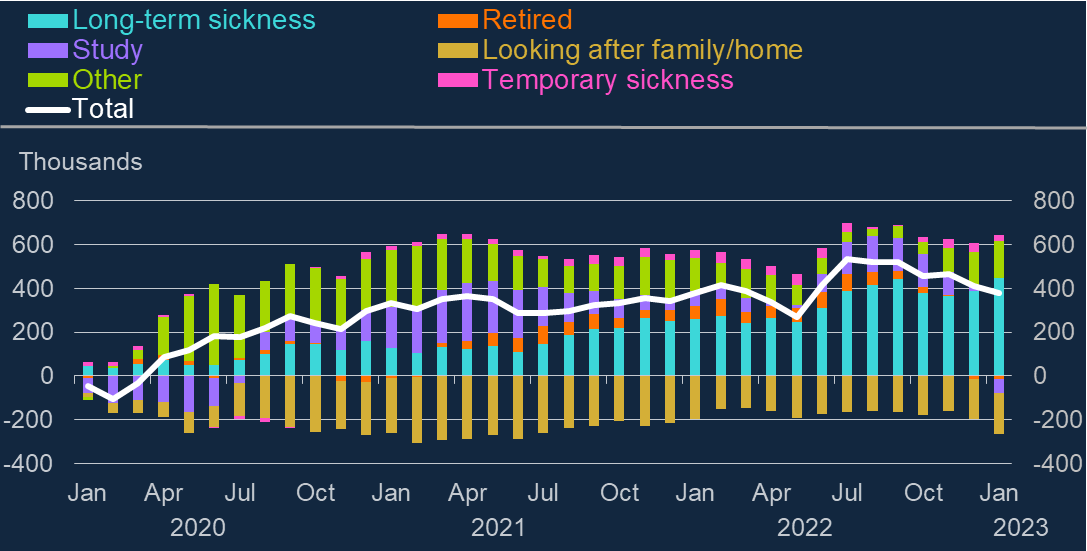

I am returning to the scene of my crimecartoon, which did not really deal with what the Governor of the Bank of England was saying as it was more a criticism about how he was saying it. However in response to a comment on my piece, I also realised that I was critical of what he was saying too. My criticism centres on the following graph:

“As you can see in blue…, long-term sickness has driven much of the persistent rise in inactivity amongst 16 to 64 year olds since the start of the pandemic. That is a striking fact.”

This is backed up by recent research carried out by LCP, whose conclusions included the following:

The rise in working age inactivity is not purely amongst those over 50; at the time of the Autumn Statement, nearly half the increase had come from the under 50s, with a big rise in the number of students a major factor;

Data on flows into and out of long-term sickness show that persistently high inflows into long-term sickness are a key problem; one growing group is those who flowed into long-term sickness having been previously categorised as ‘short-term sick’; this suggests that failure to address short-term sickness, including through clinical intervention, could have contributed to the increase in long-term sickness;

Amongst the entire economically inactive population of working age, very few of those who are retired say they ‘want a job’, whereas over 600,000 of the long-term sick say they would like to work if they could; this suggests that policies designed to help the long-term sick are ‘pushing at an open door’ in terms of supporting people who would actually go back to work given the right opportunities and treatment;

The “striking fact” for me is that the Governor of the Bank of England, faced with very similar data to LCP, instead concluded the following:

…the rise in economic inactivity is a change to the supply of labour, independent of demand, in particular by older workers. If those workers have accumulated enough savings to sustain a desired level of consumption much like the one they had before their early retirement, at least for a while, aggregate demand will not have fallen by as much as aggregate supply. We should expect this to put upward pressure on inflation in a way that would call for a higher level of interest rates to dampen demand.

But this is a comment on a dataset which shows most new inactivity is in the over 50s (which it isn’t) and that there is no large group of people currently economically active who wish to return to work given the right levels of support (there are 600,000 of the long-term sick in this category). What the LCP report concludes plausibly from the data is that policies designed to help the long-term sick who want to go back to work given the right opportunities and treatment and those designed to support the NHS to increase its capacity in primary care and mental health services in particular, would have much more impact on the number of people defined as economically inactive. As the LCP report says:

Clearly, a range of policy initiatives will be required to tackle economic inactivity, and these will include measures to reduce the ‘inflow’ into inactivity (eg people currently in work retiring or going off sick), but in terms of measures designed to increase the ‘outflow’ from inactivity, doing more for the long-term sick is likely to be far more effective than concentrating on those people who have already retired.

Meanwhile, the Governor of the Bank of England has an interest rate hammer for a tool and he therefore needs the problems he is addressing to look as much like a nail as possible (my explanations in non-italics):

So while population ageing is very likely to pull long-run R* down (this is the long-run average real equilibrium interest rate, net of inflation, averaged over the economic cycle), as I discussed earlier, the effects on shorter-run r* (which is the theoretical equilibrium rate of interest at a given point in the economic cycle) from a change in labour force participation are harder to assess. In the shorter run, by reducing the productive capacity of the economy, the rise in inactivity driven by early retirement (which is virtually non-existent as his own graph shows) seems likely to have contributed to a rise in cyclical r*. This is part of the reason why we have had to raise Bank Rate by as much as we have.

But what about a rise in inactivity caused by long-term sickness? Interestingly, Jonathan Haskel, another MPC member who also voted for the latest rate rise, recently presented some fascinating work with Josh Martin on long-term sickness and labour market outcomes. Amongst the implications of the rapid rise in long-term sick amongst the UK’s economically inactive population are: • Long-term sickness is more than just a reason for economic inactivity – many in-work are long-term sick; • The out of work long-term sick have high rates of wanting jobs, but less success in getting them, which suggests cultural or structural barriers.

Making their lives more difficult by interest rate rises which increase their living costs and reduce the security of any employment they may already have seems an odd way to solve either of these problems.

OK I am talking about satisfaction with the NHS a little bit, as it was all over the media yesterday. Just 29% satisfaction compared to 70% in 2010, with the chart above helpfully showing the precipitous decline since then. Does that remind you of another set of graphs I put up not too long ago?

It should. We stopped spending the same proportion of GDP that other similar countries do on their health services and our performance in terms of patient satisfaction plummets. Who would have thought it?

In fact this was only a headline as the Kings Fund and Nuffield Trust had just issued their analysis of the NHS-related bits of British Social Attitudes Survey Number 39, which had originally been published in October, and was itself based on data collected between September and October 2021. However it is an impressive survey overall, with 44,000 households taking part (you can find the full technical details of the survey here).

What is very clear is that the nation is changing fast. Some things are not – a slender majority in favour of increasing taxes and spending more on health, education and social benefits has remained almost static since pre pandemic and all of the averages conceal very polarised views between Brexiteers and Remainers, the different communities in Scotland and Northern Ireland, and particularly between Londoners and the rest of the UK.

This looks like it is beginning to be recognised, with a big increase in the proportion agreeing that working people do not get their fair share of the nation’s wealth (up to 67% compared to 57% in 2019) and, for the first time, a slim majority in favour of moving to proportional representation.

Only 17% say it is very important for being truly British to have been born in Britain, which is down from 48% in 1995, which feels like a sea change in attitudes towards immigration to me.

And then we turn to the environment. Rather echoing the Met Office research I highlighted recently, 45% view climate change as the most important environmental issue, compared with only 19% in 2010, with 40% of the population very concerned about the environment, compared with 22% in 2010.

Which brings us to two climate stories in quick succession.

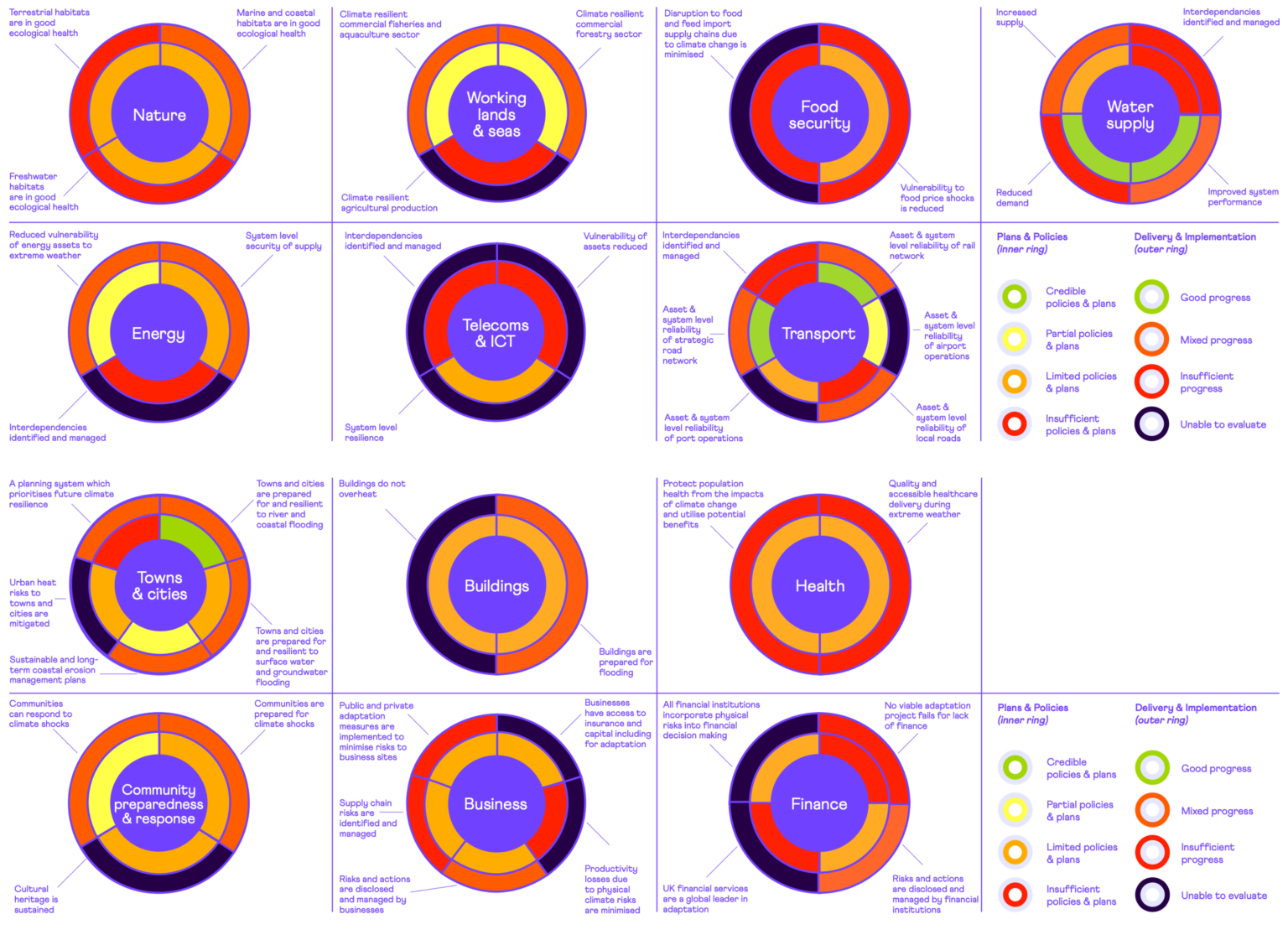

The first was yesterday, when the Committee for Climate Change, appointed to assess the Government’s progress against its own commitments on climate change, gave its 2023 report to Parliament on England’s progress in building climate resilience across the economy – and the extent of policies and delivery to meet them. It was not a positive assessment.

There is a striking lack of climate preparation from Government:

Policies and plans. Despite some evidence of improved sectoral planning by Government for key climate risks, ‘fully credible’ planning for climate change – where nearly all required policy milestones are in place – is only found for five of the 45 adaptation outcomes examined in this report.

Delivery and implementation. In none of the 45 adaptation outcomes was their sufficient evidence that reductions in climate exposure and vulnerability are happening at the rates required to manage risks appropriately. For around one-quarter of outcomes, available indicators show insufficient evidence of progress.

Baroness Brown, Chair of the Adaptation Committee, went further:

The Government’s lack of urgency on climate resilience is in sharp contrast to the recent experience of people in this country. People, nature and infrastructure face damaging impacts as climate change takes hold. These impacts will only intensify in the coming decades.

This has been a lost decade in preparing for and adapting to the known risks that we face from climate change. Each month that passes without action locks in more damaging impacts and threatens the delivery of other key Government objectives, including Net Zero. We have laid out a clear path for Government to improve the country’s climate resilience. They must step up.

By coincidence, today is the Government’s Energy Security Day, backed by a report called Powering Up Britain. This follows a High Court ruling last October which found that, when they signed off their carbon strategy, they didn’t have the legally required information on how carbon budgets would be met. The article went on to say:

Ten million tonnes of carbon could be illegally unleashed in the mid-2030s as a result. Doubt was also shed on the 95 per cent of the sixth carbon budget that was accounted for in the government’s estimates.

Mr Justice Holgate also ruled that the strategy breached the Climate Change Act by failing to provide enough detail on the emissions savings, leaving parliament and the public in the dark.

Originally called Green Day, but presumably dropped after Jeremy Hunt’s comments about not wanting to be an American Idiot, the Energy Security Day has highlighted the following Government priorities:

Energy security: setting the UK on a path to greater energy independence.

Consumer security: bringing bills down, and keeping them affordable, and making wholesale electricity prices among the cheapest in Europe.

Climate security: supporting industry to move away from expensive and dirty fossil fuels.

Economic security: playing our part in reducing inflation and boosting growth, delivering high skilled jobs for the future.

Further analysis at this stage has not been made easy by the way that the Government has released details. Chris Stark, the Chief Executive of the Committee for Climate Change has described it on Twitter as “government by press release”, ie

The government now adopts this communications strategy regularly: press release the night before – published documents later. It gives them two bites of the press coverage.

But it makes it hard for a statutory organisation like @theCCCuk, with legal duties, to comment.

Others have been less constrained in their response. The main criticisms are that many of the policies presented in the report have been announced previously, that there is no significant increase in support for home insulation and that the focus on carbon capture and storage (CCS) is out of all proportion given the long-standing difficulties of scaling up the technology.

The BBC quote Bob Ward, policy director at the Grantham Research Institute on Climate Change at LSE:

What does not make sense is to carry on with further development of new fossil fuel reserves on the assumption CCS will be available to mop up all the additional emissions.

I had an initial skim of the report looking for what was planned for heat pumps, which regular readers of this blog will know I have some history with. I found this:

The Government has an ambition to phase out all new and replacement natural gas boilers by 2035 at the latest and will further consider the recommendation from the Independent Review of Net Zero in relation to this. People’s homes will be heated by British electricity, not imported gas. The Heat Pump Investment Accelerator will mean heat pumps are manufactured in the UK at a scale never seen before. We want to make it as cheap to buy and run a heat pump as a gas boiler by extending the Boiler Upgrade Scheme by three years, and by rebalancing the costs of electricity and gas.

So reading between the hype, they are going to invest £30 million in heat pump manufacture in the UK, which they claim will attract £270 million of “private investment into manufacturing and associated supply chains”.

The other parts are:

Committing to extending the £5,000 grant for another three years (which is less than the difference between the cost of installing a heat pump and a gas boiler currently in many cases, although this may change if schemes like the recently announced Octopus pilot become more widely adopted).

The “Clean Heat Market Mechanism” which is supposed to encourage the installation of low carbon heating appliances.

A consultation to shift green levies off electricity and on to gas bills.

The country is changing fast. The Government needs to be more transformational than this to keep up. Or, in Baroness Brown’s words, step up!

The Governor of the Bank of England gave a very long speech (with the longest, quite technical, section in the middle about R* apparently aided by ChatGPT) at the LSE a couple of days ago. This had me wondering who he thought he was talking to and therefore, by extension, who he thinks he is representing with his policy choices.

I was looking through my old blog posts the other day and came across something I wasn’t looking for. Actuaries and Science Fiction told the story of a one-off visit I made to the Birmingham Science Fiction Group (BSFG), when the guest speaker had been the late great Brian Aldiss, who told the story of a time Kingsley Amis had had dinner with Margaret Thatcher. He told her what his book Russian Hide and Seek was about, to which she had responded that he needed to get himself another crystal ball.

By coincidence, I have just joined the BSFG nearly 10 years later (well I needed to think about it!), attending my first meeting online (Anna Stephens – really good about writing for Warhammer and Marvel in particular) and now very much looking forward to seeing Alastair Reynolds at my first in person meeting next month. I now have a bit more context for the Kingsley Amis story, as Andy Beckett has an account of a dinner Amis had at Thatcher’s Flood Street house in the late 70s (before she became Prime Minister). He wrote at the time:

I was rather overcome with the occasion and the fairly close propinquity of Mrs T…very much a new face to me as to most people, too much so to take in a lot about the fare except that it was properly unimaginative, and, as regards drink, ample enough. The hostess wore one of those outfits that seem to have more detail in them than is common, with, I particularly remember, finely embroidered gold-and-scarlet collar and cuffs to her blouse…[she was] one of the best-looking women I had ever met and for her age…remarkable.

And he also attributed the following quote to Thatcher herself:

People have always said that the next election is going to be crucial. But this one really will be, and if it doesn’t go the way Denis and I want then we’ll stay [in Britain], because we’ll always stay, but we’ll work very hard with the children to set them up with careers in Canada.

Anyway, back to Aldiss. He had told the story as he felt it showed how Thatcher (and he was not just picking on her as he felt this was a view held by many) misunderstood science fiction. It was not about prediction of the future, but for people who “liked the disorientation” of portraying an unfamiliar landscape.

Ursula K. Le Guin goes further in her introduction to The Left Hand of Darkness (just finished it and, if by any chance you haven’t read it already, it is an amazing piece of immersive world building which will leave you never feeling the same way about gender again). As she says:

Science fiction is not predictive; it is descriptive.

Predictions are offered by prophets (free of charge), by clairvoyants (who usually charge a fee, and are therefore more honoured in their day than prophets, and by futurologists (salaried). Prediction is the business of prophets, clairvoyants and futurologists. It is not the business of novelists. A novelist’s business is lying.

The weather bureau will tell you what next Tuesday will be like, and the Rand Corporation will tell you what the twenty-first century will be like. I don’t recommend that you turn to the writers of fiction for such information. It’s none of their business…All they can tell you is what they have seen and heard, in their time in this world, a third of it spent in sleep and dreaming, another third of it spent telling lies.

And, my favourite bit:

In reading a novel, any novel, we have to know perfectly well that the whole thing is nonsense, and then, while reading, believe every word of it. Finally, when we’re done with it, we may find – if it’s a good novel – that we’re a bit different from what we were before we read it, that we have changed a little, as if by having met a new face, crossed a street we never crossed before. But it’s very hard to say just what we learned, how we were changed.

The artist deals with what cannot be said in words.

The artist whose medium is fiction does this in words. The novelist says in words what cannot be said in words.

Who wouldn’t want to do that? It struck me while I was reading those words how the pandemic was something which changed all us survivors a little (and some a lot of course) and in ways that are often hard to put in words. But we are changed and there is work to do to try and understand how, even if that cannot be completely put in words.

The other thing from the introduction which has stayed with me is Le Guin’s contention that, while we read a novel, we are bonkers: believing in people who have never existed, hearing voices, perhaps even becoming other people. As she says:

Sanity returns (in most cases) when the book is closed.

But what about when you can’t close the book? Are we, to a greater extent, condemned to some level of future insanity? As William Faulkner said:

The past is never dead. It’s not even past.

In 2013 I tried to suggest that actuaries might also be about portraying an unfamiliar landscape and trying to work out what would hold true under different circumstances, and that they should therefore put themselves about a bit more, even if they sometimes made themselves look a bit foolish in the process. As William Hynes reminded me at yesterday’s excellent An introduction to alternative economic thinking event (recording available soon from the Institute and Faculty of Actuaries), the group of economists responding to the Queen’s question as to why noone saw the 2008 crisis coming, concluded:

In summary, Your Majesty, the failure to foresee the timing, extent and severity of the crisis and to head it off, while it had many causes, was principally a failure of the collective imagination of many bright people, both in this country and internationally, to understand the risks to the system as a whole.

If a failure of imagination is the main problem, I would suggest that science fiction must be at least a part of the solution. Looking a bit foolish at times is a bit of a speciality for me, so you probably won’t be surprised to hear that I am devoting most of my time from here on in to an almost certainly doomed attempt to write what Le Guin might regard as a good novel. I have been here before, way back in my pre-actuarial past, and have a nice back catalogue of unpublishable books and rejection letters to look at whenever I forget that I have no idea what I am doing. But if I find myself shouting to noone in particular that what I am trying to say cannot be said in words, I might dare to believe that I am on the right track.

{kind=link}