This review originally appeared in the May issue of Brum Group News, the newsletter of the Birmingham Science Fiction Group and is reproduced here (lightly edited) by kind permission

This book is so many things: a work of fantasy, a literature review of every major work about the journey into hell, a love story, a wicked academic satire, a philosophical musing on the meaning of life and a love letter to Cambridge. Or perhaps the title itself, which means both a retreat to the coast, in this case to the banks of the River Lethe, as well as a descent into Hell. Like its Oxford counterpart before it – Babel – its central leap is that magic (here referred to as magick, ie the academic discipline stretching back to the alchemists and beyond) sits alongside the other subjects at Oxbridge colleges. The magic we see practised, taught, researched and dissertationed feels very mathematical. So we are unsurprised to hear that the mathematicians hate the magicians.

Alice Law is the Chinese-American PhD student of the great Jacob Grimes, who (accidentally?) sends him to Hell and then, with her once-friend-now-mortal-enemy and Grimes’ other PhD student, Peter Morgan, sets out to bring him back. So that Grimes can pass their dissertations, because that’s a good enough reason to journey to Hell and sacrifice half of your future lifespan. And so the quest begins.

There is quite a bit of mathematical fun had despite Alice not really knowing any mathematics, including an Escher Trap, a Penrose Staircase and a hyperbolic geometry which makes the quest very heavy going at times. And so many logic puzzles. Comedy and total horror are nicely juxtaposed throughout, as Alice and Jacob get to understand each other better and start to wonder whether Grimes is worth it after all.

The constant side swipes at the life of a junior academic are often hilarious. Magicians in training are apparently told by all their professors that they should consider careers in other fields or “alt academia”, as they called it:

“…no one really meant it when they said alt academia was just as prestigious (or, more commonly, that there was no shame in it, really). They meant it even less when they emphasized that alt academia paid better, had kinder hours, was less stressful, gave you better job security, made you happier. Oh, magicians do really well in consulting, they said. Employers like critical thinking and problem-solving skills, they said. Fewer people die in industry, they said.”

The most enigmatic character is their not-quite-constant companion, Archimedes the cat, who guides them when he feels like it. All the way through all eight of the Courts of Hell, alongside and across the Lethe and finally to King Yama’s Domain, on a journey which threatens to destroy Alice’s very sense of self. Her catechism, which she repeats at stressful moments:

I am Alice Law I am a postgraduate at Cambridge I study analytic magick

Alice has always felt that if she could just hang on to the delusions which had got her this far until the end of her PhD all would be well, but these turn out to be precisely the things she needs to confront if she is ever going to get out of Hell.

Source: Nick Foster – December 2013 – originally drawn to deride George Osborne’s austerity as Pugwash Economics, repurposed now as I am worried about the actuarial profession pulling up the ladder on the next generation

The “black box” was a constant refrain when I was working as an actuarial consultant. It was where the results from a process were being accepted without any understanding of how they were arrived at. Something we felt that any self-respecting actuarial consultant should challenge in their own work and everybody else’s.

However when you came to actually present analysis or arguments to a client, you expected a certain amount of that expertise to be taken as read, to effectively be inside a black box as far as the client was concerned. They couldn’t be expected to understand all of the aspects of what you were talking about, otherwise they wouldn’t need you. Good practice was always to put them in a position where they could understand and make decisions about the key aspects of your advice without needing to engage with the other parts. As the expert, you decided what was in the black box.

Now the black box is back with a vengeance for all the professionals who have relied upon them in their working lives. As Dan Davies puts it:

The same black-box property which stops you from being second guessed or overruled means that nobody is interested in your explanations for your decisions; it is definitional of being a black box that you are going to be judged by results.

And, if you are in the business of advising in the teeth of uncertainty, as actuaries are, then this is likely to be a real problem. If noone cares how your advice was constructed, but they can get advice that ticks the compliance box your client has to complete more cheaply and quickly than you can, the more automated black box is going to win the business. The experienced professional still has a role in managing this process, verifying the results coming out of the black box and determining what can still be kept out of the black box, but he may be increasingly struggling to justify the cost of his junior colleague.

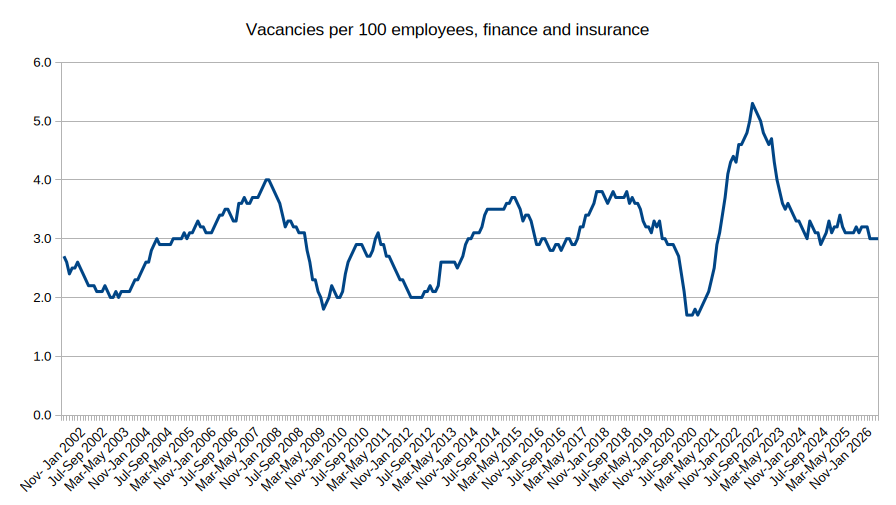

Well things don’t look so bad in the UK right now according to the Office for National Statistics (ONS), reverting to close to the average after a post pandemic surge in the finance and insurance sector:

However, if we look at the United States, which tends to show us where the UK finance sector is going, it looks far more ominous:

Yesterday Sky News ran a story about Standard Chartered‘s CEO who, in his desperation not to describe over 7,500 job losses as cost cutting, said this:

It’s not cost-cutting. It’s replacing in some cases lower-value human capital with the financial capital and the investment capital we’re putting in.

We may need to sit with that statement for a little while.

Daniel Susskind talks about this risk in his latest lecture entitled A World Without Work: in summary, to paraphrase only slightly, sure relatively junior white collar roles may already be particularly hard hit by AI, but he is optimistic because of the impact on GDP and we cannot pause because of China. He then goes on to talk about the four problems he sees for a post AI future:

Distribution (replacing wages);

Contribution (how do you “pull your weight”);

Power (domination by Big Tech on economics, politics, liberty, social justice and democracy); and

Meaning (fulfilment in life).

Susskind has gone from thinking that the fear that AI is coming for your jobs was overblown and that it was just task encroachment that we faced, to now thinking that it may encroach on all the tasks in most fields. Jevons Paradox (that technological innovation that increases the efficiency of a resource’s use leads to a rise in consumption of that resource) is no comfort if that new demand is robot-met.

Carlo Iacono suggests that the move of junior roles to AI may be subtle to begin with:

The weakness among young workers may appear as fewer people entering employment from outside the workforce. Firms may not fire large numbers of juniors; they may simply hire fewer of them.

That matters. The labour market can look healthy while the entry path narrows. Senior workers stay employed. Output rises. Productivity improves. There is no dramatic wave of redundancies.

Yet the first rung is being taken out.

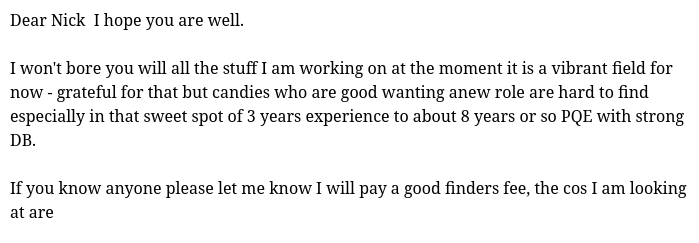

It may also be masked by the fact that there remains a shortage for actuaries beyond the entry roles. There is almost a hint of desperation to approaches like this looking for introductions from a retired actuary like myself:

(followed by a list of clients he is working for)

Source: recruitment consultant who will remain anonymous. I am assuming “candies” are candidates

And, even if you think the risk of the AI Bubble bursting soon, taking down the global stock markets underpinned by the Magnificent 7, is exaggerated, you do need to be suspicious about the current abilities of AI to replace junior staff. My experience with another, somewhat earlier, actuarial technology, the pensions valuation engine, would suggest that the outputs need to be analysed very carefully before sharing with a client: it often had dependencies between what should have been independent variables hidden in the programming, or vagaries in the setup which left out non-standard benefit rules for your particular scheme, for instance. Or the student who had set it up initially (a complicated process usually) might have made a mistake or you might have not communicated with them very well to start with. Or a hundred other things.

For whatever reason, there was often still a lot to do after the valuation engine had produced some output.

Can this sort of thing happen with agentic AI? Well think about that student programming the valuation engine, but on steroids. Its patchy capabilities combined with its basic psychopathy leads to, as Hannah Fry entertainingly demonstrates here, some serious problems arising with the agent’s relentless to and fro with the large language models it depends upon, asking them what it should do next. As Hannah says:

I built an AI agent. She opened a shop selling novelty mugs, emailed a journalist without being asked, and then leaked our passwords to a total stranger.

As Kyle Kingsbury wrote about having an AI agent as a colleague in a programming team:

Imagine a co-worker who generated reams of code with security hazards, forcing you to review every line with a fine-toothed comb. One who enthusiastically agreed with your suggestions, then did the exact opposite. A colleague who sabotaged your work, deleted your home directory, and then issued a detailed, polite apology for it. One who promised over and over again that they had delivered key objectives when they had, in fact, done nothing useful. An intern who cheerfully agreed to run the tests before committing, then kept committing failing garbage anyway. A senior engineer who quietly deleted the test suite, then happily reported that all tests passed.

You would fire these people, right?

Yet despite all this, the money continues to pour in to the construction of AI infrastructure. There are already websites up and running for all of the parts of tasks AI cannot encroach upon.

The bottom rung of the actuarial ladder is clearly in danger. This is a particular problem for the actuarial profession, which has traditionally relied on longer periods of work-based training for its future qualified actuaries than many other professions. Training to become an actuary takes a long time. Median time to fellowship is still around six years, with some taking up to ten or giving up. The exams are hard to pass. There have been attempts by the profession to tackle some of these disincentives: the Chartered Actuary designation to make a destination of the generalist qualification before the specialisation of the fellowship, championed on this blog and launched in the teeth of opposition by some fellows, being one example.

It has led to a culture within actuarial firms around managing the extended time in training, with rituals around study leave and results days. One of the fears expressed in opposition to the introduction of the Chartered Actuary designation was that, if this could be achieved almost entirely within formal education at universities, the value of working alongside experienced actuaries would be lost.

It has led to a culture within the profession itself of managing large parts of its education system in house. Half of its revenue and around 30% of its expenditure are on “pre-qualification learning and development”. Sometimes it looks more like an education business with a professional side hustle.

But then the new AI toys have come along, and it turns out that many of those experienced actuaries may be less keen on graduates coming in and needing supervision from them after all. Many of them may rather spend hours on AI prompts than on developing another human being.

I fear that, increasingly, companies are not going to accommodate actuarial students in their work plans without significant persuasion. And, if the number of students studying while in work falls, the profession itself is going to struggle to finance its own bespoke education system at an acceptable cost to its members.

It will be hard for the profession to challenge this too: it is going to be good for many of those already established in their roles as the market for more experienced actuaries, when the market has no interest in developing the actuaries of the future, becomes increasingly competitive.

If the actuarial profession does accept the challenge of protecting the pipeline of future experienced actuaries it will need to review its entire education syllabus through this lens. It will also need to engage with other partners involved in what is in effect a problem of capital formation and collective action: government incentives may be needed to encourage firms to continue to train early career professionals and discourage free-riding. There may be no way back for the student with no actuarial qualifications learning on the job. The universities may be needed to plug people in at a different career point, which will require them to innovate themselves even further into the professional training role than ever before. As Carlo Iacono points out:

educational institutions may be pushed to simulate more of the apprenticeship environment. That does not mean adding a thin “AI literacy” module. It means creating settings where students practise judgement under uncertainty, in realistic workflows, with feedback that is close enough to hurt and useful enough to teach.

It will not be at all easy. But the alternative is a future without opportunity for those who do not already have it and an ageing profession withering on the vine it refused to nurture.

Shakespeare appearing in the play he has written in order to say goodbye to his dead son

“You are not saying what you think you are saying” was what Ray Nayler said to the Birmingham Science Fiction Group on Friday night, as part of a wider conversation about the mutual misunderstandings that result from cultural differences. He had landed up with the Peace Corps in Turkmenistan 20 years ago, “The worst place to live in the world”. It ripped away his sense of stability and the fixed nature of life he had developed growing up in San Francisco and made him realise that everything is arbitrary. His new book Palaces of the Crow is out next week, about a group of escapees on the run in a forest trapped between the German and Soviet armies in World War 2, with only a murder of intelligent crows as allies. I will be buying it.

And so to a different forest.

Last night I could not speak for half an hour. My face ached from the effort of holding myself together and tears were running down my face. No I wasn’t in the back of an ambulance on my way to Good Hope Hospital. I had just watched Hamnet for the first time.

I am peculiarly sensitive to father-son depicitions in art. I can’t remember when a film affected me as deeply as Hamnet did, but I do remember the last book that had me in floods of tears (The Road by Cormac McCarthy when (spoiler alert) the father of the boy dies. Suggest you don’t read it on a train like I did). Why should I cry for you by Sting also tends to have me in bits.

However Hamnet was still like nothing I have ever experienced before in a movie. It snuck up on me, this story of the fight to make a family and then keep it alive in a way that certainly didn’t feel over 400 years old before hitting me with the final scene which was, ultimately stagey for goodness’ sake. I felt connected – to the forest, to the plague-beset 16th century characters, to everyone who has ever lost a child, to everyone looking for connection to help them through their day. I have watched so much Shakespeare in my life, but I have never felt the urgency that must have lain behind the plays quite like this before.

This was just great art. Not in a way that impresses you but leaves you cold, but in a way that you realise has expressed the driving forces of life directly at your central nervous system.

And how close the film was to what really happened doesn’t matter. Any more than the plot accuracy of any of Shakespeare’s plays matters. It was emotionally true and believable and mourned the death of a child as every child death should be mourned. It made nearly every other movie I have ever seen seem trite by comparison, including the hugely entertaining but ultimately much less full Oscar rivals this year. This is the movie you stick on the next gold disc sent out on a probe into deep space to explain humanity.

And it immediately started me thinking about how infrequently I experience emotional truth outside my friends and family. Is this the missing component from public life?

Keir Starmer certainly wasn’t passing any auditions this morning. He was not saying what he thought he was saying. He thought he was saying something about training young people, being “at the heart of Europe” and nationalising British Steel. What he was actually saying was that he has no idea why he lost 1,496 English council seats over the weekend but, despite this, was going to hang on until someone removed him forcibly from office. And he is guessing, perhaps rightly, that the Labour Party does not have the determination to do so. It was the precise opposite of emotional truth or, as John Elledge posted:

“You are not saying what you think you are saying” is unfortunately true for nearly all of us nearly all of the time. Until it isn’t. And those moments when it isn’t are moments of enormous power.

And to think I still have Maggie O’Farrell’s novel to read. Or possibly the audiobook read by the great Jessie Buckley, Agnes Hathaway herself. May be hard to resist.

This fig tree is in the cemetery at Mission Santa Barbara. “Fig Tree” by HarshLight is licensed under CC BY 2.0.

I am reading a wonderful book at the moment: The Island of Missing Trees by Elif Shafak. It has allowed me to inhabit the Cyprus of the late 50s and mid 70s and understand a bit more about why my time on the island after my birth in 1962 was so short. It is also the first book I have read where a major character is a fig tree.

And it is the fig tree that makes the most acute observations about humans. My favourite one is this:

Even so, based on personal experience, I can tell you one thing about humans: they will react to the disappearance of a species the way they react to everything else – by putting themselves at the centre of the universe.

Humans care more about the fate of animals they consider cute – pandas, koalas, sea otters and dolphins, too, of which we have many in Cyprus, swimming and frolicking about our shores. There is a romantic idea as to how dolphins perish, washed to the beach with their beak-like snouts and innocent smiles, as if they have come to bid humankind one last farewell. In truth, only a small number do that. When dolphins die, they sink to the bottom of the sea, as heavy as childhood fears; that’s how they depart, away from prying eyes, down into the blue.

Bats are not deemed to be cute. In 1974, when they died in their thousands, I didn’t see many people shedding a tear for them. Humans are strange that way, full of contradictions. It’s as if they need to hate and exclude as much as they need to love and embrace. Their hearts close tightly, then open at full stretch, only to clench again, like an undecided fist.

Humans find mice and rats nasty, but hamsters and gerbils sweet. Doves signify world peace, whereas pigeons are nothing more than carriers of urban filth. They proclaim piglets charming, wild boars barely tolerable. Nutcrackers they admire, even as they avoid their noisy cousins, the crows. Dogs evoke in them a sense of fuzzy warmth, while wolves conjure up tales of horror. Butterflies they look on with favour, moths not at all. They have a soft spot for ladybirds, and yet if they were to see a soldier beetle, they would crush it on sight. Honeybees are favoured in stark contrast to wasps. Although horseshoe crabs are considered delightful, it’s a different story when it comes to their distant relatives, spiders…I have tried to find a logic in all this, but I have come to the conclusion that there is none.

This compulsion of humans to put themselves at the centre of the universe and dominate everything else is being written about by many writers at the moment, all of them giving it different names. Nate Hagens sees our species as part of an economic Superorganism:

This Superorganism is mindless, unplanning, and energy-hungry. It isn’t evil, it doesn’t feel, and it doesn’t care about equity, ecology, or human wellbeing. It solely optimizes for throughput, scale, and for more – even when more becomes the problem. There is no mastermind behind the wheel, only billions of incentives aligned in the same direction toward extraction and consumption.

When the limits to their extraction of resources are exceeded, the parasitic systems must either suffer a crash or must invade and take the energy of a more distant ecology or society.

Luke Kemp refers to the consequent empires we have built as Goliaths, with diminishing returns on extraction ending fairly predictably:

The result is more extractive institutions creating growing instability, internal conflict, a drain of resources away from government, state capture by private elites, and worse decision-making. Society – especially the state – becomes more fragile. Private elites tend to take a larger share of extractive benefits. The state, and many of the power structures it helps prop up, then usually falls apart once a shock hits: for Rome it was climate change, disease, and rebelling Germanic mercenaries; for China it was often floods, droughts, disease and horseback raiders; for the west African kingdoms it was invaders and a loss of trade; for the Maya it was drought and a loss of trade; and for the Bronze Age it was drought, a disruption of trade and an earthquake storm.

And so it should come as no surprise that the latest Planetary Solvency report from the Institute and Faculty of Actuaries and Anglia Ruskin University – Planetary Solvency: Tipping into the wild unknown – catalogues a terrible toll on the Earth system which supports us, with biodiversity loss, climate shocks and geopolitical conflict disrupting the food system, risking catastrophic impacts for the financial system and for society as a whole.

A few examples from the report:

The world lost 26.8 million hectares of natural forest in 2024 alone. This is larger than the entire UK, which spans 24.9 million hectares. This activity generated 10 gigatons of carbon emissions;

In the UK alone, bees and other pollinating insects have on average lost a quarter of their habitat since 1980. Around 75% of the different crops used in global food production relies on pollinators to some extent, although by weight the dependence is around 35%. Loss of pollinators would reduce yields for most crops but would wipe out some altogether, eg brazil nuts, kiwi, melon and cocoa.

Around the UK, warming seas have already begun shifting fish populations northward, with cod, haddock, and salmon being replaced by species like anchovy, bluefin tuna and squid (the real story behind the catfish sold in fish and chip shops headlines)…If global warming, ocean acidification, overfishing and pollution continue on their current trajectories, the economic and social consequences are likely to be severe. In the event of more extreme tipping points, such as the collapse of the Gulf Stream, the consequences could be even more catastrophic.

Around 70% of emerging infectious diseases originate in animals, with land-use change, deforestation and wildlife trade increasing the risk of future pandemics.

The UK does not have enough land to feed its population and rear livestock: a wholesale change in consumer diets would be required. It would also require greater investment in the agri-food sector so that it is capable of innovating in sustainable food production.

Some technologies exist that could help, but need significant research, development and investment to have a chance of working at scale. Protecting and restoring ecosystems is easier, cheaper and more reliable. The time required to develop and scale technologies is unknown without further research. Both existing (plant pre-breeding, regenerative agriculture) and emerging technologies (AI, lab grown protein, insect protein) offer potential solutions.

The other writers mentioned above all look at the future slightly differently:

Hagens is pessimistic about our chances of stopping the Superorganism, but believes we can start planning now for what comes next. Miller McDonald hopes for the “opening up of possibility for alternative forms of organisation of human life”. Luke Kemp says that collapse has historically benefited the 99% at the expense of the elite 1%, although he does worry that our modern economy makes us more dependent upon global infrastructure and we have much scarier weapons than in the past.

But shocks in the short and medium term – of the climate, of the economy and of our politics – now have a feeling of inevitability about them. I wonder how the fig tree will feel about them.

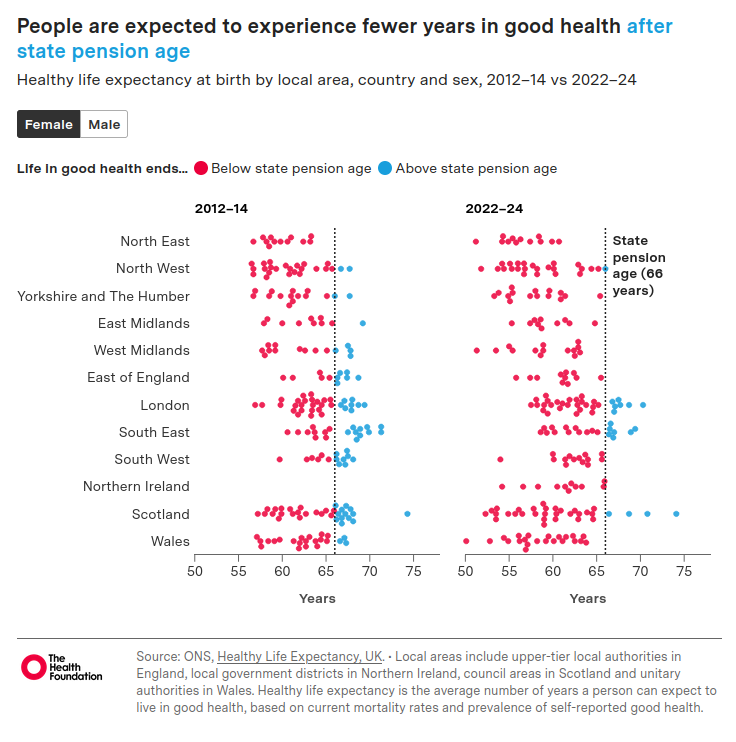

Yesterday an extraordinary thing happened: the news story about the UK’s falling healthy life expectancy led the BBC News for a while, ahead of the King’s visit to the US in the wake of the assassination attempt on Trump’s team and the latest twists in the Mandelson affair. And so it should: over the decade 2012–14 to 2022–24, healthy life expectancy in the UK fell by about 2 years, to 60.7 years for males and 60.9 years for females.

And that is just the average. As we can see from what I felt was the most informative graphic from the Health Foundation’s report, some of the local authority areas have seen precipitous falls over the same period. Merthyr Tydfil has fallen from 57.6 years to 50.1 years. North Lanarkshire has fallen from 58.3 years to 52.3 years. And in England, Sandwell has fallen from 57.7 years to 51.3 years. In the 2012-14 data, only one region had no local authorities with a healthy life expectancy below the state pension age. By 2022-24, most regions have a healthy life expectancy below 66 years.

Healthy Life Expectancy (HLE) is defined as the number of remaining years that an individual can expect to live in “very good” or “good” general health. Rates of “very good” and “good” general health by sex and five-year age band are captured from the following survey general health question on the Annual Population Survey (APS) and in the Census 2011 and Census 2021:

How is your health in general; would you say it was…

Very good?

Good?

Fair?

Bad?

Very bad?

I last wrote about HLE in 2017 in response to John Cridland’s review of the State Pension Age. My view at that time, when healthy life expectancy was plateauing rather than falling like a stone, was that it was time to consider a universal basic income model. Then only the poorest decile was going to be condemned to 18 years of working in poor health until they could claim a state pension. Now the overall averages in some local authorities have moved down to join them, this consideration appears rather more urgent.

In 2014, I was concerned about what happens if the healthy life expectancy doesn’t increase in line with the planned increases to the State Pension Age and, towed along 10 years behind it, Normal Minimum Pension Age (NMPA). Well here we are: 26 of the little local authority blobs are at or below the current NMPA of 55. This nearly doubles to 49 local authorities (assuming the fall in HLE doesn’t continue, which feels like a heroic assumption at the moment) when the NMPA is due to rise to 57 in April 2028.

As the Health Foundation report says:

While healthy life expectancy has declined, life expectancy has remained broadly stable for the UK overall, indicating that the deterioration is not primarily driven by changes in mortality. However, in more deprived areas, life expectancy remains below pre-pandemic levels, suggesting mortality plays a greater role in reducing healthy life expectancy in these areas. Worsening self-reported health remains a key factor throughout the UK, highlighted by a falling proportion of life spent in good health and by wider evidence of declining health among the working-age population.

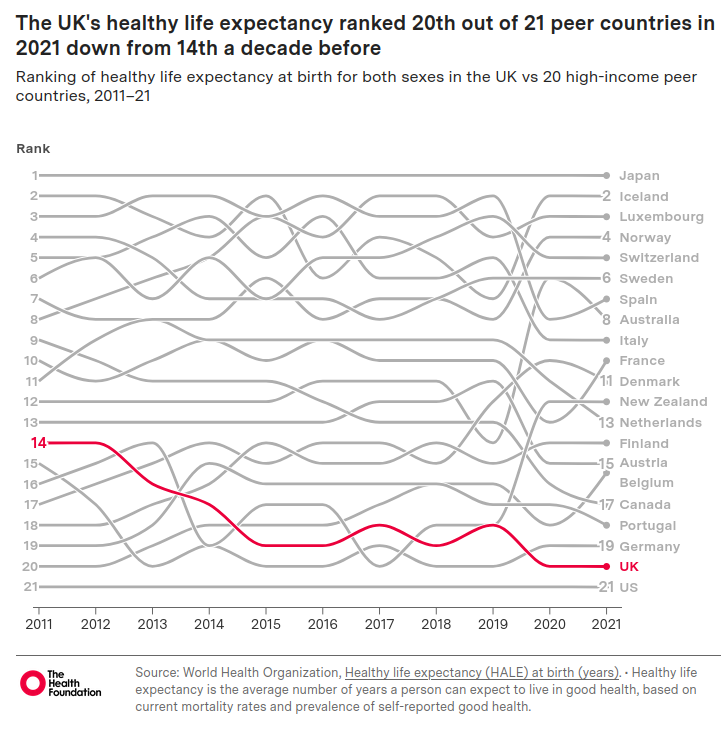

Other countries have not experienced this, illustrated by the UK sliding down the international comparison tables:

In the complete table the UK is sandwiched between Puerto Rico and China, with (from World Bank data) GDP per capita respectively of $39,344 and $13,303, compared to the UK’s GDP per capita of $53,246 (all from 2024).

Andrew Mooney, The Health Foundation’s principal data analyst, said: “The UK has the highest levels of obesity in western Europe and there has been a surge in mental ill health, especially among young people.”

Perhaps, instead of obsessing over GDP growth, we should be focusing on what countries like Iceland, Norway, Australia and New Zealand have been doing in recent years to tackle population health. I think it would make us all feel better.

The Wetherspoons pub The Mary Shelley in Bournemouth

A few months ago I decided to read Mary Shelley’s Frankenstein for the first time. I also watched Guillermo del Toro’s Frankenstein, on a big screen, despite, according to The New Yorker, it having been “Netflixed down to size”.

Shelley’s book is largely monologues of interior thoughts of Frankenstein and his creation, with wildly careering emotions and death, death, death everywhere – perhaps unsurprising from an author whose mother died 10 days after giving birth to her, who lost a child and whose half sister died by suicide while she was working on Frankenstein, with much more tragedy to follow after its publication. There is a word Mary Shelley uses more than I have read in any other book: variants of sympathy/sympathise/sympathies turn up 32 times. Because of course one of the many things the book is all about is mutual incomprehension of the creator and the created.

Last week I was in Bournemouth as a last minute substitute for Lanzarote, something I may come back to at a later date, and I stumbled across the churchyard of St Peter’s Church in which Mary Shelley was buried, along with the cremated heart of her husband Percy Shelley, at the age of 53. There is also a pub in Bournemouth named after her (above) but whose sign depicts the monster from her most famous piece of writing.

As we enter another time of mutual incomprehension of the creator and the created, I have been reading the surprisingly-difficult-to-access paper by Kyle Kingsbury (the systems engineer, not the MMA guy) called The Future of Everything is Lies, I Guess. I will put a link to an X account which shared it here, as going to the aphyr.com site to read it seems to generate this message:

Once you can read it though, it starts to sketch out a likeness of our current monster and chip away a little at the human side of the mutual incomprehension. I am talking, of course, about what people are currently calling “AI”, which Kingsbury defines as:

…a family of sophisticated Machine Learning (ML) technologies capable of recognizing, transforming, and generating large vectors of tokens: strings of text, images, audio, video, etc. A model is a giant pile of linear algebra which acts on these vectors. Large Language Models, or LLMs, operate on natural language: they work by predicting statistically likely completions of an input string, much like a phone auto-complete. Other models are devoted to processing audio, video, or still images, or link multiple kinds of models together.

The article sets out how this is a technology where nobody really understands why it has been successful or how to make it better, which falls into strange loops or attractors, has odd gaps in its capabilities and is highly sensitive to slight changes in its formatting. It is a technology which is simultaneously highly capable and an idiot. And Kingsbury worries that our culture is not ready for such a technology. As he says:

As LLMs etc are deployed in new situations, and at new scale, there will be all kinds of changes in work, politics, art, sex, communication and economics. Some of these effects will be good. Many will be bad. In general, ML promises to be profoundly weird.

Buckle up.

He continues:

Most people seem concerned with conscious, motivated threats: AIs could realize they are better off without people and kill us. I am concerned that ML systems could ruin our lives without realizing anything at all.

There follow extensive examples of the problems the various ML applications are already starting to cause and some speculation about where things may be going in various areas of our lives before we get to the chapter on work. And the subject of hiring “AI employees”. This is probably my favourite bit:

Imagine a co-worker who generated reams of code with security hazards, forcing you to review every line with a fine-toothed comb. One who enthusiastically agreed with your suggestions, then did the exact opposite. A colleague who sabotaged your work, deleted your home directory, and then issued a detailed, polite apology for it. One who promised over and over again that they had delivered key objectives when they had, in fact, done nothing useful. An intern who cheerfully agreed to run the tests before committing, then kept committing failing garbage anyway. A senior engineer who quietly deleted the test suite, then happily reported that all tests passed.

You would fire these people, right?

Kingsbury sees the two extremes of the possible range of outcomes as:

ML systems continue to hallucinate, cannot be made reliable, and ultimately fail to deliver on the promise of transformative, broadly-useful “intelligence”. Or they work, but people get fed up and declare “AI Bad”…a lot of ML people lose their jobs, defaults cascade through the financial system, but the labor market eventually adapts and we muddle through. ML turns out to be a normal technology.

In the other extreme, OpenAI delivers on Sam Altman’s 2025 claims of PhD-level intelligence, and the companies writing all their code with Claude achieve phenomenal success with a fraction of the software engineers. ML massively amplified the capabilities of doctors, musicians , civil engineers, fashion designers, managers, accountants, etc, who briefly enjoy nice paychecks before discovering that demand for their service is not as elastic as once thought, especially once their clients lose their jobs or turn to ML to cut costs. Knowledge workers are laid off en masse and MBAs start taking jobs at McDonalds or driving for Lyft, at least until Waymo puts an end to human drivers. This is inconvenient for everyone: the MBAs, the people who used to work at McDonalds and are now competing with MBAs, and of course bankers, who were rather counting on the MBAs to keep paying their mortgages. The drop in consumer spending cascades through industries. A lot of people lose their savings, or even their homes. Hopefully the trades squeak through. Maybe the Jevons paradox kicks in eventually and we find new occupations.

In the following chapter Kingsbury speculates on what some of those new occupations might be:

Incanters. People who can prompt LLMs into getting what is wanted.

Process Engineers. People who help catch LLM errors. They build quality control processes – training people, identifying where more intense review is needed, assessing the cost-benefit trade offs of automating tasks, etc

Statistical Engineers. People who try and measure, model and control variability in ML systems.

Model Trainers. This will become increasingly difficult as the amount of false content or “slop” increases across the internet.

Meat Shields. People who are accountable for the errors of the ML systems they supervise.

Haruspices. People responsible for going through the model inputs, outputs and internal states of a ML system which has done something terrible to try and give a plausible reason for its behaviour.

But ultimately Kingsbury concludes that we should just stop using these systems. To return to the original analogy, the monster cannot be understood. There is often nothing actually there to understand. And it is certainly not in the business of understanding you. Although it may be very very good at convincing you otherwise.

On balance I think my view is currently at the muddle-through-with-ML-as-a-normal-technology end, which still looks likely to cause a disruption considerably bigger than 2008. My main reason is the already collapsing trust in many of the Big Tech companies. Trust which is going to be required even if their technology really can do some of this stuff. It is the scenario where we all get fed up and declare “AI Bad”. Like when we read about the people running Meta showing nowhere near the social responsibility commensurate with their current level of market power.

Or when, as last week, we have days and days of breathless commentary about Anthropic’s Mythos and Project Glasswing, and how its immense capabilities caused the company not to release it, sparking a meeting of central bankers to discuss the threat such technologies posed to financial systems. Only to finally read an account of attempts to verify any of what Anthropic have been saying. It is quite a technical piece, which I by no means understand all of, but the final paragraph is fairly arresting:

The most important thing in the Mythos release is not the model. It is the precedent. Anthropic has established, without discussion and without pushback, that a private company can unilaterally classify a capability as too dangerous for the public, grant selective access to the largest incumbents in the affected industry, and construct a parallel disclosure regime outside any democratic accountability structure. That precedent is exclusivity for abuse. It will be used by companies with worse judgment than Anthropic and narrower definitions of “partner” than the Glasswing consortium. The time to object to the shape of this thing is while it is still being built, not after it has removed all transparency and accountability.

How might Claude or ChatGPT respond to being designated “AI Bad”? Well Mary Shelley’s monster put it this way:

Once I falsely hoped to meet with beings who, pardoning my outward form, would love me for the excellent qualities which I was capable of unfolding. I was nourished with high thoughts of honour and devotion. But now crime has degraded me beneath the meanest animal. No guilt, no mischief, no malignity, no misery, can be found comparable to mine. When I run over the frightful catalogue of my sins, I cannot believe that I am the same creature whose thoughts were once filled with sublime and transcendent visions of the beauty and the majesty of goodness. But it is even so; the fallen angel becomes a malignant devil. Yet even that enemy of God and man had friends and associates in his desolation; I am alone.

This review originally appeared in the April issue of Brum Group News, the newsletter of the Birmingham Science Fiction Group and is reproduced here (with light editing) by kind permission

A few years ago the historian Adam Tooze said the following about the times we are living in:

If you’ve been feeling confused and as though everything is impacting on you at the same time, this is not a personal, private experience. This is actually a collective experience.

The word he came up with for this experience was “polycrisis”. It described the interplay of the Covid pandemic, Ukraine war and the energy, cost-of-living and climate crises. To that we could now add Trump 2nd term, war in Gaza and now the Gulf.

I am reviewing this book while I have Covid, which has certainly facilitated the kind of inner focus which I think the book is asking for. Because Slow Gods is polycrisis in the form of space opera, but a curiously interior-monologuey kind of space opera, more psychological than boom-boom.

The premise, as Claire North set out for us at the Birmingham Science Fiction Group last June, is that a binary star system is due to collapse which will obliterate all life within an 83 light-year blast radius. Unusually, the populations in the vicinity are warned of this precisely 100 years in advance by a perfect black sphere moving through space at sub-light-speed and known by everyone as the Slow.

The Slow listens to everything, remembers it and will consider it.

We follow the story through the eyes of Maw, who has been killed and has recovered in such a way as to be very difficult to kill after that. Making Maw an ideal candidate for Pilot, the organic sentient needed in the pilot’s seat of any ship wishing to enter arcspace which lets it travel across the universe faster than light, at huge personal cost. Pilots die frequently and each planetary system has its own way of choosing and rewarding its Pilots. Only Maw appears to be able to act as Pilot again and again, which makes the people around Maw nervous.

The main thing about Maw which makes people nervous is Maw’s relationship with “the darkness” which reaches into any ship in arcspace, in many cases sending people mad. Maw, instead, becomes “curious”, exploiting a changing relationship and perception of matter in the darkness to do monstrous things. But, despite all this, Maw is still required to keep running missions, although usually with a mechanical assistant to keep Maw from getting “dysregulated”.

This unusual set up turns out to be a way of observing the psychology of the polycrisis with some clarity. The United Social Venture is an empire where its subjects acquired debt just from being born (measured in Glint):

Everything the Venture gave us – the air we breathed, the roads we walked down, the schools we learned in – had been sweated for, bled for, and our debts were a marker of the needful labour we would give back in return.

This economic system was referred to as Shine. The Shine were one of the few systems which used prisoners for Pilot work.

One of the joys of the book is the exploration of difference, lots of details about avoiding giving offence when the Xi of Xihanna ask Maw to pilot a ship to Adjumir to bring out historical artefacts and Maw meets Gebre of the Haalo Institute. Maw finds that Normspeak is regarded as a very crude way of communicating and starts, haltingly, to learn Adjumiri (which is at least in part a click language). So begins a very moving love story.

Gender differences between systems are very striking. The Shine have only two genders – “he” and “she” – although the elite also have hé and shé. The most manly and the most feminine.

There are four genders in Xihanna, but they are not regarded as particularly important characteristics of a person and dispensed with once you know someone well. On Adjumir, there are eight, with very few Adjumiris remaining the same gender all their lives. These differences are picked out by the brilliant use of pronouns, a useful technique in a book full of characters. Even mechanicals, who have no particular interest in gender, are referred to as qe/qis as a mark of respect as “they do not wish to be put in the same category as a bowl of soup or a broken chair”.

We join Maw towards the end of the 100 year programme to evacuate the populations of Adjumir and Hadda to relative safety, with 800 million still on the planets and increasingly desperate. The Slow has effectively taken on a role as God through its massive databases, calculation capacity and sheer longevity. It seeks out Maw as it has plans for him. The Slow has been around so long that qe sees everything in the very long run. Which means that the emotional turmoil and intense highs and lows of individual lives are all averaged out to nothing. Qe calculates in terms of galaxy-level populations on the basis of what qe has come to think of as love.

What calculation would the Slow make about our world, with all our nation states and their often tiny differences blown up to justify war aims? Donald Trump certainly has to have the most Shine of any US President for some time.

Slow Gods moves slowly but relentlessly towards a showdown between Maw and Theodosius Rhode, the Executor of the Shine and executioner of his mother. There is much tragedy along the way and the ending is not straightforward but ultimately very satisfying. It’s an uplifting ride.

Front page of the April 2026 issue of Brum Group News

Three and a half years ago, I wrote a piece likening the rapid climate change on Earth to the fairly well-established science fiction concept of terraforming, but in reverse. So what has happened since? Well last summer, according to researchers at Imperial College and the London School of Hygiene and Tropical Medicine, two thirds of the 24,400 heat deaths from June to August across Europe were due to human-made global heating. And a study published last month has suggested that the pace of global warming has nearly doubled since 2015.

It this point I would like to suggest rehabilitating an old word to describe this process, in the opposite direction to terraforming (which is action designed to make a planet more habitable). Barrenize means to make barren or sterile and was used between the mid 1600s and the early 1700s according to the Oxford English Dictionary, originally in the context of animal husbandry. I think it’s time to bring this word back.

In a week when a US President has threatened, variously, “blowing everything up and taking over the oil” and that Iranians would be “living in Hell”, to last night saying that “a whole civilisation will die tonight”, unless they opened the Strait of Hormuz, it certainly sounds like a commitment to barrenization to me, only at a faster pace than the global warming he is already doing everything possible to accelerate further.

On Friday this week, the Birmingham Science Fiction Group will have Oliver Bettis as its guest speaker. Oliver has been a leading actuary in the field of sustainability for many years. He is one of the authors of a series of publications by the actuarial profession in collaboration with the University of Exeter in recent years.

Climate Scorpion shows how we need to develop a best guess about the worst-case scenarios and make policy on that basis, given our lack of knowledge about extreme climate risk and tipping points.

Planetary Solvency – finding our balance with nature sets out an approach to civilisational risk management which attempts to address the fact that the severity and frequency of extreme events are unprecedented and beyond current model projections.

Parasol Lost, which we will be discussing in particular this Friday, focuses on the cooling effect of aerosols: a side-effect of pollution from fossil fuel burning. Without aerosol cooling the global temperature would be around 0.5°C higher than the 1.4°C increase above pre-industrial temperature that we have today. It is critically important to recognise that, as air pollution is cleaned up, this may ironically lead to a short-term increase in warming through the loss of aerosol cooling. The question must be asked, can we afford to lose this cooling and if not, should this be replaced by working with nature, using technology or both?

This will allow us to tap into the rich history of science fiction literature on terraforming (and dealing with the threat of barrenization) and whether this can allow us to look at this question in a new way. It should be a lively discussion.

This event will be held in-person at the Friends of the Earth Warehouse, 54-57 Allison Street, Birmingham B5 5TH and simultaneously on Zoom, with online access opening from around 7.45 for an 8 pm start.

Ticket prices for non-members are £8 for in-person attendance and £6 for Zoom attendance. For members it’s £4 in-person attendance and free Zoom attendance.

Tickets can be purchased on the door or via the Eventbrite link below:

And if this whets your appetite for more science fiction and you think you might like to join the group, just email us at contact@brumsfgroup.org.uk. Hope to see you there!

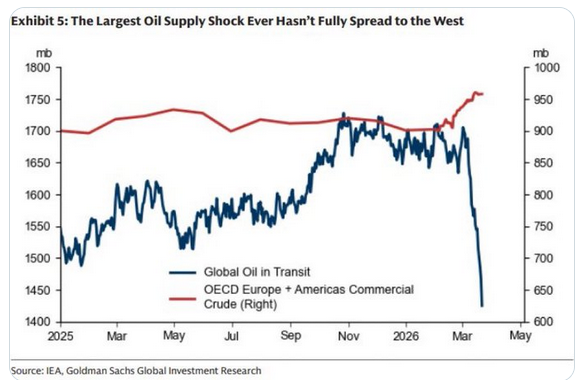

OK I don’t know if this is a remotely helpful post, but it really feels to me like one of those months we will look back on, like March 2020, and wonder what we were thinking. To recap: on 4 March 2020, while Italy were shutting all their schools and a month after the WHO had declared a global health emergency, we were noting that the number of cases in the UK had jumped from 53 to 87 in one day.

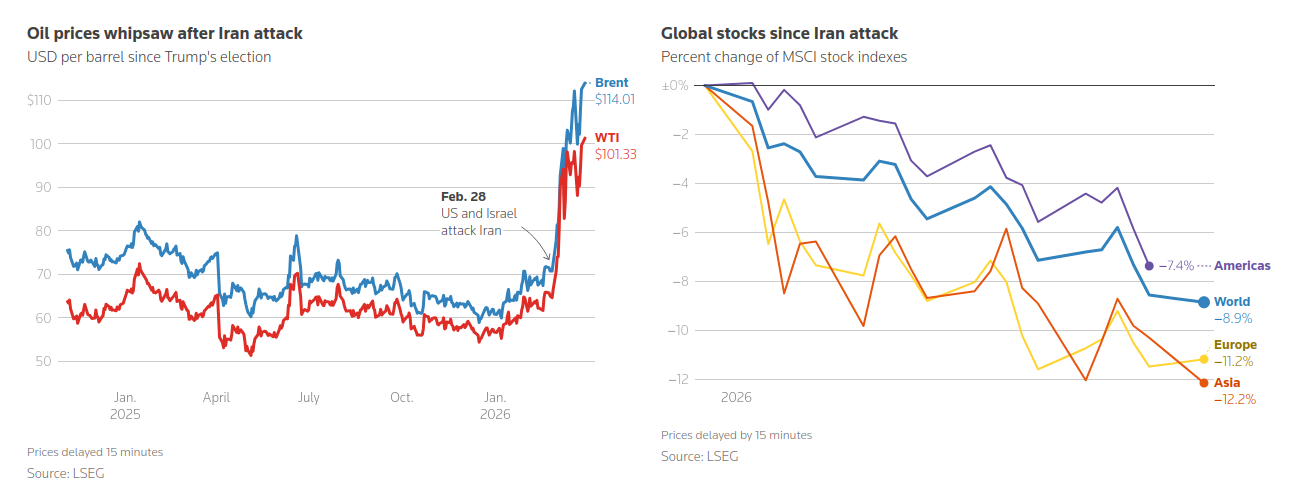

Jump forward to now and the number of tankers with oil on board is in freefall:

Trump is talking about invading Kharg Island and “obliterating” Iran’s energy facilities, and we are sitting in the time lags of international fossil fuel freight waiting to see what will happen. But we already know what is going to happen. Just like the pandemic, we will be taking similar measures to the countries already more affected very soon. The order looks like Asia, followed by Africa, then Europe and only then, ironically, the United States.

So what is going on in Asia right now? Well the Philippines announced a national energy emergency six days ago, setting up an authority to oversee the orderly distribution of fuel, food, medicines, and other essential goods. Sri Lanka has announced a four-day week for all government employees. Egypt is ordering restaurants, cafés and shops to close at 9pm to safeguard dwindling energy reserves. Slovenia has brought in fuel rationing. Moldova’s Parliament has also voted to impose a state of emergency in the country’s energy sector. Australia is offering free public transport. Measures are also being taken in Thailand, Ethiopia, Myanmar, Vietnam, Bangladesh and South Sudan.

On 3 March 2020, the UK Government unveiled their Coronavirus Action Plan, which outlined what the UK had done and what it planned to do next. Paul Cosford, a medical director at Public Health England, said widespread transmission of COVID-19 in the United Kingdom was “highly likely”.

On 4 March 2020, the Daily Express were telling us:

Which we clearly weren’t. Meanwhile the Daily Mail was anticipating future lockdowns and 6 million people being off sick:

The next day we had the first Covid death in the UK. And life was on hold for the next two years.

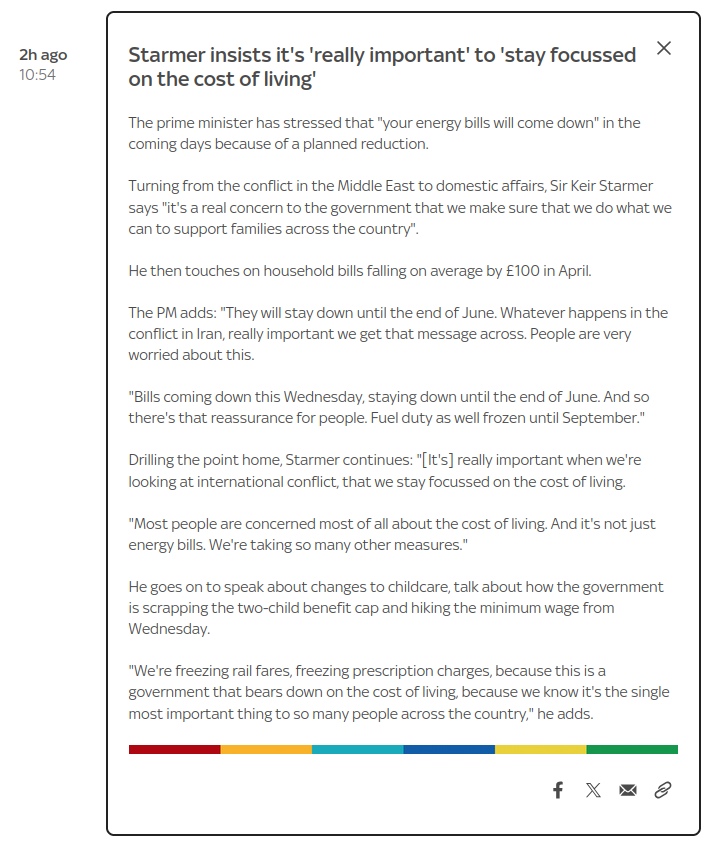

Our response to the energy crisis seems to be almost entirely focused on

1. The cost-of-living crisis; and

2. The financial markets.

The Education Secretary has said that motorists should fill up as normal as the government is “well prepared” for disruption. The trouble is, many of us still remember September 2000:

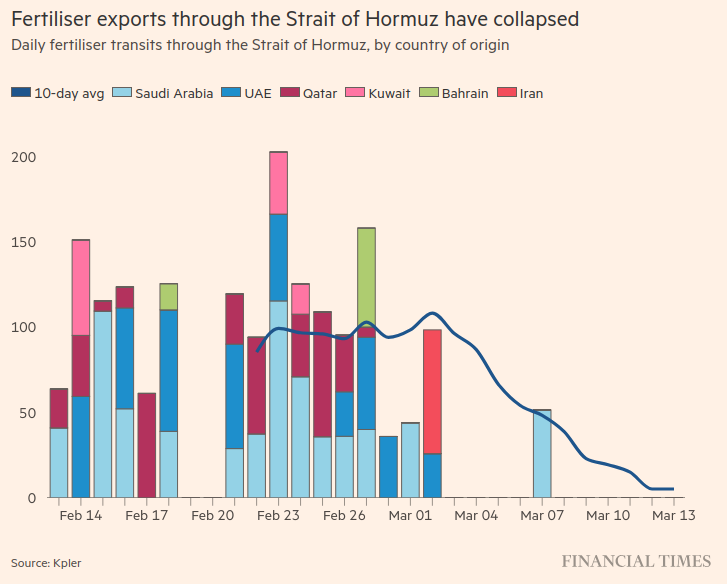

So that would be enough to make us all feel nervous about shortages and queues for everything, having our lives disrupted and out of our control. But the real potential issue is not even being talked about, certainly not by the government. It is a shortage of food. Steve Keen sets out the economics of global food production here. This does not tend to feature prominently in mainstream economic analyses which are energy and food blind for the most part, although the FT did have this graph a couple of weeks ago:

As Steve Keen says:

Survival will depend on grain reserves. China has of the order of 18 months in reserve, which will insulate it from the disruptions of 2026. The USA and India have substantial reserves as well, but some countries—including the UK—have virtually none.

…Famines will ensue, and even countries that have never experienced such events could be forced into food rationing. This includes the UK and Australia, and a patchwork of countries across Europe.

This is what people are nervous about: not being able to get enough food, either because it isn’t available at all or not at a price they can afford. Calling that a cost-of-living crisis is a bit like calling the Black Death a labour market crisis. And it doesn’t stop there. As Steve Keen continues:

Other critical products that normally pass through the Strait of Hormuz include Helium, which is critical to the production of semiconductors, and sulphuric acid, which is critical to numerous production processes. The closure of the Strait cuts off one third of global helium output and about half of global sulphuric acid output.

With critical industrial inputs cut as well, the problems will cascade well past food alone—though that is clearly the most damaging impact. With LNG, petroleum, helium and sulphuric acid production cut, the capacity to undertake repairs to damaged facilities will also be hindered.

The TED War is rather like smashing a spider’s web—and then killing the spider.

The spider certainly looks in a poor state of health at the moment, and parts of the web will take years to fix. This is the crisis we are all inevitably going to be entering in the next few weeks. For who knows how long.

A risk management approach to this crisis would involve communicating a plan to the country that minimised the impulse to hoard resources and protected the most vulnerable from extreme prices, rather than bland reassurances from government ministers. We need this to be in place very quickly now.

Seven years ago I wrote about Catch 22 and actuarial practice, concluding, rather piously:

If we want far fewer actuaries to be employed in not growing alfalfa in the future and far more working on making the finance structures of our economy work better, whether to support a Green New Deal or more generally, we first need to embrace the idea that our current economic priorities are indeed insane.

So imagine my excitement at finding Catch 22 grabbed out of the pages of fiction and informing US foreign policy. Not convinced? Compare two passages. The first, from Catch 22, in 1961:

This time Milo had gone too far. Bombing his own men and planes was more than even the most phlegmatic observer could stomach, and it looked like the end for him. High-ranking government officials poured in to investigate. Newspapers inveighed against Milo with glaring headlines, and Congressmen denounced the atrocity in stentorian wrath and clamored for punishment. Mothers with children in the service organized into militant groups and demanded revenge. Not one voice was raised in his defense. Decent people everywhere were affronted, and Milo was all washed up until he opened his books to the public and disclosed the tremendous profit he had made. He could reimburse the government for all the people and property he had destroyed and still have enough money left over to continue buying Egyptian cotton. Everybody, of course, owned a share. And the sweetest part of the whole deal was that there really was no need to reimburse the government at all.

This week, the US Treasury lifted all oil sanctions on Iran. For 30 days. 140 million barrels of Iranian crude, sitting on ships at sea, may now be sold freely on the global market. Including to the United States itself.

In yuan.

The United States is purchasing, with Chinese currency, oil from the country it is currently bombing?! The same oil that funds the missiles that just shot down an F-35 for the first time. The same missiles that are redecorating allied oil infrastructure.

Treasury Secretary Bessent called this “narrowly tailored”. Narrow like in white, and tailored as in card, apparently.

In the same OFAC filing, Russian oil sanctions were lifted as well. And Belarus potash too, because apparently the universe was running low on irony and needed to top up.

The logic, insofar as there is any, goes like this: the war has crashed the global oil market so hard that the administration needs the enemy’s oil to keep gasoline prices from eating the midterms. They are unsanctioning the people they’re bombing because the bombing is working too well at the thing they didn’t want it to do. The sanctions were necessary to stop Iran funding the war, but the war made the sanctions too effective, so the sanctions had to be lifted to fund the war effort against the country that no longer needs sanctions because the oil revenues that sanctions were preventing are now required to prevent the economic damage caused by preventing those revenues, which is itself a consequence of the military campaign designed to make the sanctions unnecessary by making Iran the kind of country that doesn’t need sanctioning, which it would be, if the sanctions hadn’t been lifted to pay for making it that.

There have been many names thrown at Trump since he arrived in US politics. My personal favourite is probably the Tangerine Tyrant. Many people are currently relying on TACO (Trump Always Chickens Out) to resolve the Middle East crisis he has instigated. However, until now, I had not heard of anyone likening him to Milo Minderbender. But once you see it, it is difficult to un-see it.

Trump likes to give himself and everyone else nicknames. From the very stable genius of his first term, to more recently Honest Don and the Tariff King, whereas Milo, as M&M Enterprises (the company he started as the mess officer) expands, becomes the Mayor of Palermo, Assistant Governor-General of Malta, Vice-Shah of Oran, Caliph of Baghdad, Mayor of Cairo, and the god of corn, rain, and rice.

Trump likes to use his presidency to enrich himself, from his Trump coin to the Amazon documentary about his wife to his Board of Peace to all of his merchandise. Milo’s catchphrase is “what is good for M&M is good for the country”.

Trump doesn’t appear to believe in safety nets for ordinary people. Meanwhile Milo secretly replaces the CO2 cartridges in emergency life vests and the morphine in first aid kits with printed notes to the effect that what is good for M&M is good for the country.

Milo Minderbender is a war profiteer trying to convince himself that he is a free market fundamentalist. So what does that make Trump? Well hold that thought, because today’s Guardian has provided a partial answer I think, with a history of military targeting.

This introduces the concept of the kill chain, ie the process between detecting something and destroying it. Trying to shortcut the kill chain has been a perennial preoccupation of militaries through the ages. In the Vietnam War, Operation Igloo White dropped 20,000 acoustic and seismic sensors along the Ho Chi Minh trail, which transmitted data to relay aircraft, which then fed the signals to the IBM 360 computers at Nakhon Phanom airbase in Thailand. These analysed the data, predicted where the convoys would be and strikes were directed to those locations. The Viet Cong realised quickly that this system could not detect the difference between military vehicles and ox carts and therefore:

They played recordings of truck engines, herded animals near the sensors to trigger vibration detection, and hung buckets of urine in trees to set off the chemical detectors.

There was no way to independently check what they were destroying. The air force claimed 46,000 trucks were destroyed or damaged, which the CIA calculated exceeded the total number of trucks believed to exist in all of North Vietnam.

…air force personnel invented a creature to explain the absence. They called it the “great Laotian truck eater”.

Last time I talked about military targeting, I focused on the human in the loop, but let’s instead focus on the actual destruction going on for a moment, shall we? Trump’s assault on Iran hit 6,000 targets in two weeks. The kill chain had, apparently, been compressed so much that it allowed 1,000 decisions an hour. The school he hit, killing between 175 and 180 people, most of them girls between the ages of seven and 12, had changed its use to a school since at least 2016 and was visible on Google Maps. Old target lists had been reached for and noone had had the time or the inclination to check them before bombing them.

This is what you can expect from a Milo Minderbender presidency. It has been obvious, since at least the 1960s, that the US system requires enormous strength of purpose from its executive to hold its industrial-military complex in check. That is why so many of them have been so keen to install a Trump.

It feels as if, far from embracing the idea that our current economic priorities are indeed insane, as I fervently hoped seven years ago, we are instead doubling down on the insanity.