In October 2009, while working as a pensions actuary in Birmingham, I attended the Institute and Faculty of Actuaries’ Joining Forces in Mortality and Longevity multidisciplinary conference at the Royal College of Physicians in Edinburgh. The canapés were excellent and, of the plenary speakers, I particularly remember Rudi Westendorp from Leiden University who, in response to the question of whether it was nature or nurture that was responsible for longevity, said it was both.

It was also the first and last time I have used a sleeper train. I had a trustee meeting on the Friday morning south of London and decided that it would be a good idea to get the sleeper from Edinburgh to London on the Thursday night. I hadn’t really researched it in advance and I suppose I was expecting a cabin to myself, but it turned out I was in fact sharing with a German guy who looked like he rode the overnight trains of Europe all the time. There was a set of bunk beds which took up most of the cabin and my memories of that night were of my being thrown around every time the train took a bend down the East Coast mainline, not sleeping a wink while my room-mate snored soundly throughout and then of his taking an annoying amount of time to brush his teeth in the morning. The trustees did not get me at my best.

But I digress. The session from the conference which has stayed with me ever since was by Eugene Milne from Newcastle University. As the blurb for his session A new model of mortality and survival stated:

A new mathematical model mimics patterns of mortality in species from nematodes to humans. Net risk, it suggests, arises from two components, an interactive element accounting for historical falls in human mortality, and redundant decay which shapes lifelong risk. This suggests “intrinsic ageing” is unrelated to the slope of the mortality curve, and is unlikely to have altered for humans in recent centuries.

Eugene Milne went on to become Director of Public Health for Newcastle and took them through the pandemic. The full paper in the British Actuarial Journal from 2009 is here.

At a time where actuarial mortality modelling consisted either of projecting observed trends into the future (with no real explanatory power for observed features like cohort effects) or attempted to project a range of causes of mortality based on the likely progress in treating them (which is limited by the quality of information on death certificates), Milne’s model stood out for starting from a biological model of gradually diminishing redundancy within the body. He recognised its limitations, as he said at the time:

As a bridge between actuarial and biological approaches to ageing it falls, as yet, between two stools. The examples in this paper are generated by probabilistic computer modelling. This is clearly not adequate for

actuarial use and the model needs to be developed further to provide a form that will serve that purpose. On the other hand, it describes (as noted in section 4) a biology that would be ‘needed’ in order to construct organismal risk as it is observed. This it does well, providing a coherent account of why mortality patterns appear as they do. Yet its theoretical ‘biology’ is at odds with currently favoured theories of ageing. If the biological quantity described in the NBM [nested binomial model] as redundancy exists, we do not yet know what it is, nor why it should appear to act in so sequestered and consistent a fashion.

But the idea stayed with me, and perhaps that made me particularly receptive to Richard Murphy’s recent article about allostatis, which he describes as “the way living organisms survive by continually adapting to the changing world around them”. As Murphy points out:

If something breaks, a wealthy person can simply have it repaired or replaced. If travel arrangements fail, alternatives can be found. If income is interrupted, there are savings to draw upon. Problems remain, because they always will, but they rarely threaten the stability of everyday life for a wealthy person. In other words, the amount of adaptation required of them is reduced.

There have been a number of attempts over the years to draw attention to how your level of income affects your ability to adapt to your environment.

In George Orwell’s Down and Out in Paris and London, he describes the effect of poverty:

For, when you are approaching poverty, you make one discovery which outweighs some of the others. You discover boredom and mean complications and the beginnings of hunger, but you also discover the great redeeming feature of poverty: the fact that it annihilates the future.

However Orwell has been criticised, as the temporary tramp that he was, for deciding that meant the end of anxiety. More recently, Jack Monroe used Terry Pratchett’s example of Captain Vimes’ boots, to illustrate how what life costs depended on how much you already had:

A really good pair of leather boots, the sort that would last years and years, cost fifty dollars. This was beyond his pocket and the most he could hope for was an affordable pair of boots costing ten dollars, which might with luck last a year or so before he would need to resort to makeshift cardboard insoles so as to prolong the moment of shelling out another ten dollars.

Therefore over a period of ten years, he might have paid out a hundred dollars on boots, twice as much as the man who could afford fifty dollars up front ten years before. And he would still have wet feet.

Jack developed the Vimes Boots Index to highlight inflation in basic food products, which then persuaded the ONS to launch a shopping prices comparison tool.

But to return to the idea of redundancy: it is clear that if you have, say, redundant money which can be brought in to play when things go wrong, then things generally go much better for you. But imagine if you have used up any redundancy quite some time ago and therefore any reverse is a potential crisis. Your stress levels will be much higher all of the time, as your body tenses for the battles it knows lie ahead about anything from a car that won’t start to a boiler that packs up to a hike in the price of bus fares or the basic food products on the Vimes Boots Index. Day in, day out.

At the moment one of the differentials in redundancy is around heat stress. Housing which cannot be cooled without electricity which cannot be afforded. Day in, day out, for much of the summer so far. But in winter the same housing will need far more heating because its occupants cannot afford capital investment like insulation.

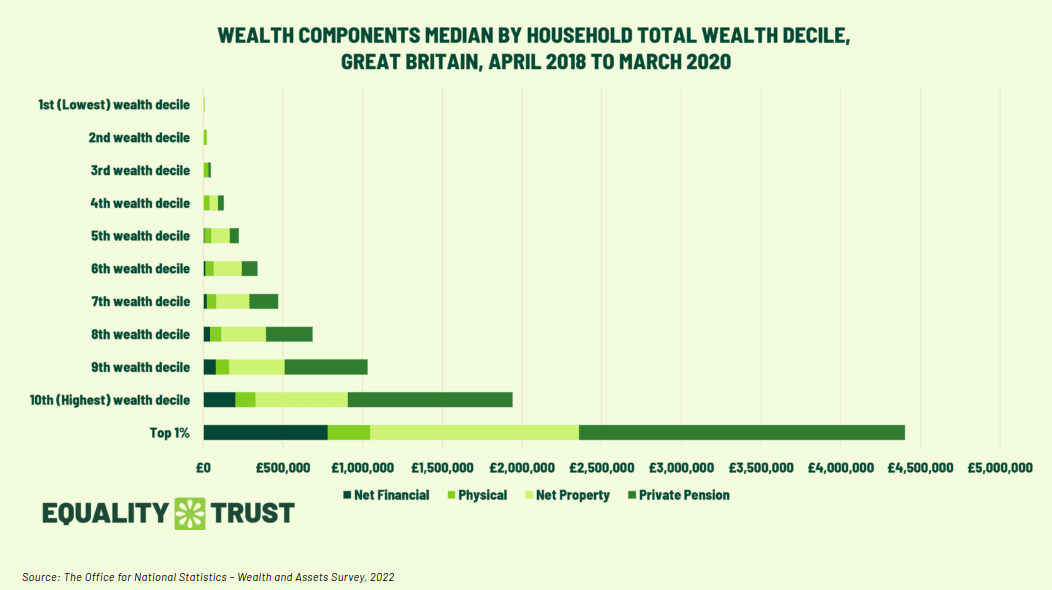

And the reason for this enormous inequality in the level of redundancy, is of course wealth and income inequality. The Equality Trust sets out the statistics as follows:

The UK has very high inequality of income compared to other developed countries; the 9th most unequal incomes of 38 OECD countries (OECD, 2022).

The UK’s wealth inequality is much more severe than income inequality, with the top fifth taking 36% of the country’s income and 63% of the country’s wealth, while the bottom fifth have only 8% of the income and only 0.5% of the wealth according to the Office for National Statistics.

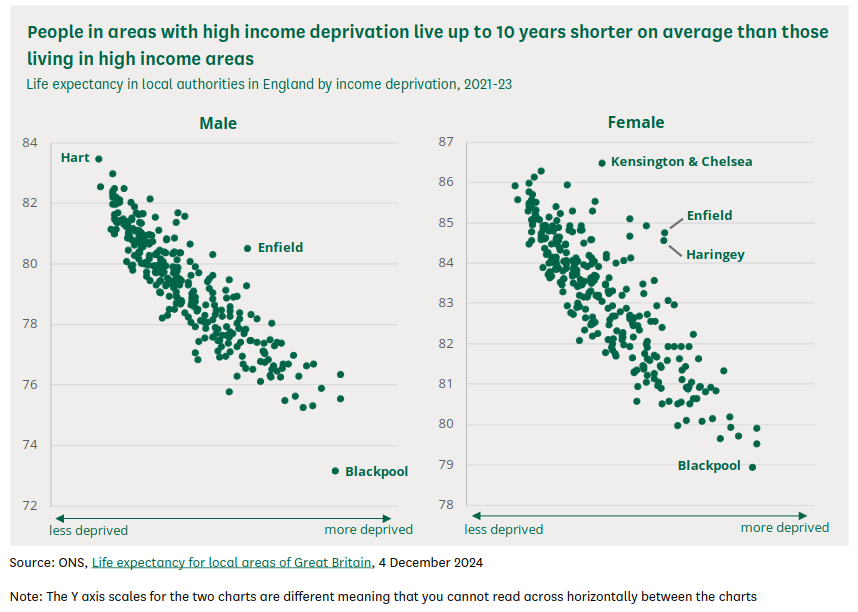

And this stress, day in, day out, means that people also die earlier, as shown below in the House of Commons Library research briefing on Inequalities in life expectancy, using ONS figures (and honestly they’re not picking on Blackpool):

And yet the most likely way for you to hear the word redundancy is when some company is planning to get rid of some of its workforce.

The trouble with people is that you don’t need them until you do, as Jonn Elledge has written here:

There are substantial differences between the US military and the NHS: but what both have in common is that, when they need something, they really do need it. The entire notion of “efficiency” is misplaced.

Similarly, in Nate Hagens’ latest interview, with biologist and biophysicist Olivier Hamant, they explore:

…how cheap, abundant energy allowed human societies to substitute the “safety net” of resource abundance for the safety net that living systems actually rely on: diversity, redundancy, and cooperation.

Until the resources stopped being so abundant.

And then there is the kind of workplace sustained redundancy programmes create, as Seth Godin says in a recent blog post:

“How few people can we get away with?” That’s a question many bosses think hard about. Automate. Streamline. Improve productivity and take humans out of as many tasks as possible. It’s a time-tested way to create profits and to increase a certain kind of reliability. Claude Code is popular with many organizations for precisely this reason.

“How can we include more people into this process?” is a less popular but often more valid way to create value. In an organization that is in the business of bringing insights, humanity and care to problems, more involvement from people creates better outcomes. The challenges make it far more valuable.

Which sort of organization would you like to work for?

And what sort of society do we want to have? One that supports the people in the bottom quintile with no redundant capital, so that they might have the resources available to maintain the stability of everyday life and reduce the adaptation required of them? Or one which keeps demanding more and more from those it allocates less and less of national wealth to. To quote from another Orwell book, Nineteen Eighty-Four, from the mouth of O’Brien, Big Brother’s Grand Inquisitor:

If you want a picture of the future, imagine a boot stamping on a human face—for ever.

I think we can all come up with better pictures of the future than that one.