There’s certainly a great deal of uncertainty about.

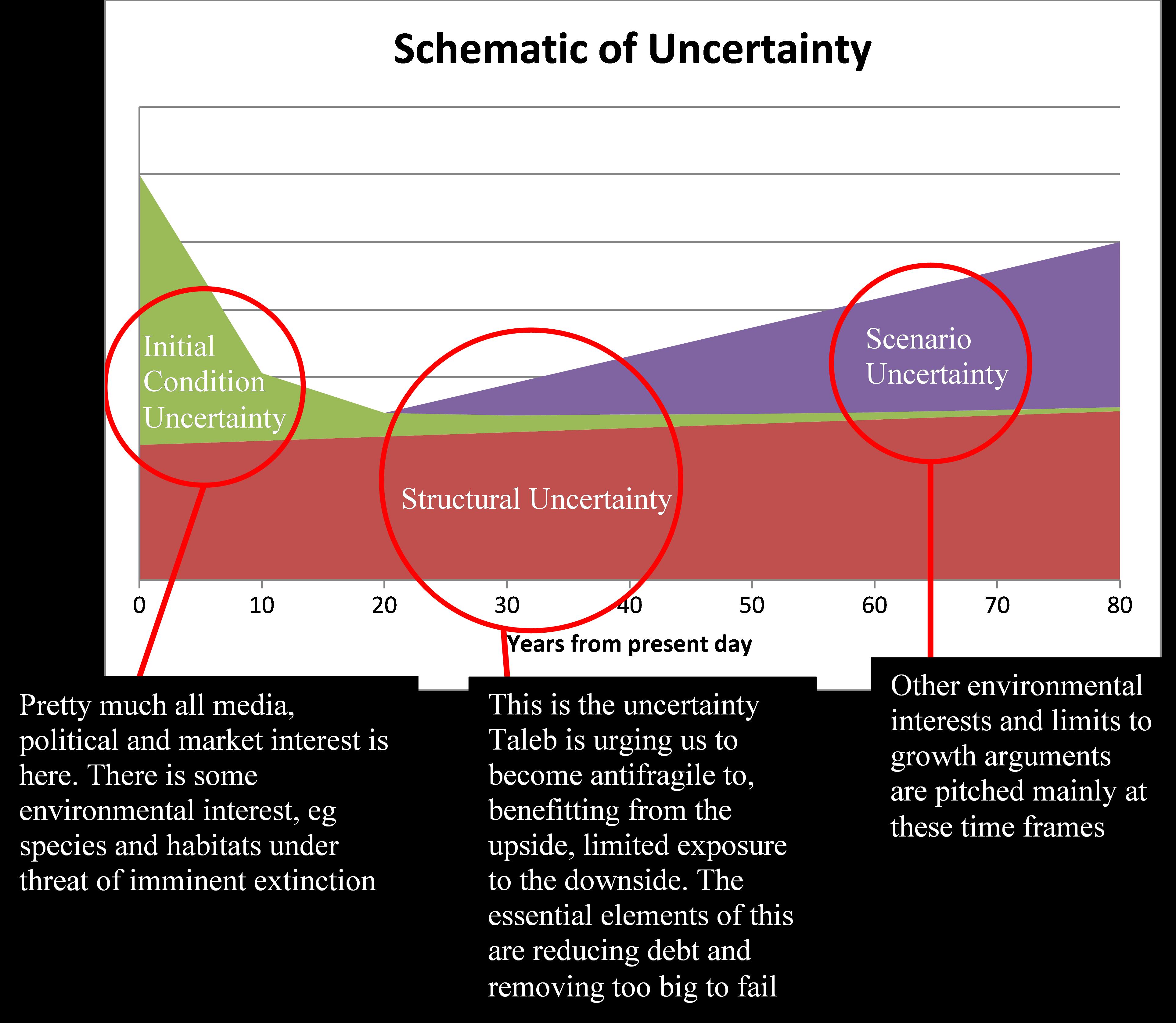

In Nate Silver’s book, The Signal and the Noise, there is a chapter on climate change (which has come in for some criticism – see Michael Mann’s blog on this) which contains a diagram on uncertainty supposedly sketched for him on a cocktail napkin by Gavin Schmidt. It occurred to me that this pattern of uncertainty at different timescales was more generally applicable (it describes very well, for instance, the different types of uncertainty in any projections of future mortality rates). In particular, I think it provides a good framework for considering the current arguments about economic growth, debt and austerity. Some of these arguments look to be at cross-purposes because they are focused on different timeframes.

In the short term, looking less than 10 years ahead, initial condition uncertainty dominates. This means that in the short term we do not really understand what is currently going on (all our knowledge is to some extent historical) and trends which might seem obvious in a few years are anything but now. Politics operates in this sphere (long term thinking tends to look two parliaments ahead at most, ie 10 years). However, the market traders who by their activities move the markets and market indices on which we tend to base our forecasts and our economic policies are also working in the short term, the very short term (ie less than 3 months to close off a position and be able to compare your performance with your peers), even if they are trading in long term investments.

In the short term, looking less than 10 years ahead, initial condition uncertainty dominates. This means that in the short term we do not really understand what is currently going on (all our knowledge is to some extent historical) and trends which might seem obvious in a few years are anything but now. Politics operates in this sphere (long term thinking tends to look two parliaments ahead at most, ie 10 years). However, the market traders who by their activities move the markets and market indices on which we tend to base our forecasts and our economic policies are also working in the short term, the very short term (ie less than 3 months to close off a position and be able to compare your performance with your peers), even if they are trading in long term investments.

So both the politics and economics is very short term in its focus, and this is therefore where the debate about growth and austerity tends to be waged. The Austerians (which include the UK Government) claim to believe that debt deters growth, and that cutting spending in real terms is the only possible Plan A policy option. The Keynesians believe that, in a recession, and when interest rates cannot go any lower, demand can only be revived by Government spending. This argument is now well rehearsed, and is in my view shifting towards the Keynesians, but in the meantime austerian policies (with all the economic destruction they inevitably cause) continue in the UK.

However, there are other groups seemingly supportive of the UK Government’s position in this argument for altogether different reasons. Nassim Nicholas Taleb argues that high levels of debt increase an economy’s fragility to the inevitable large devastating economic events which will happen in the future and which we cannot predict in advance. He therefore dismisses the Keynesians as fragilistas, ie people who transfer more fragility onto the rest of us by their influence on policy. These concerns are focused on the structural uncertainty which is always with us and is difficult to reduce significantly. It is therefore important to reduce (or, if possible, reverse) your fragility to it.

At the longer term end are the groups who believe that we need to restrict future economic growth voluntarily before it is done for us, catastrophically rapidly, by a planet whose limits in many areas may now be very close to being reached. They are therefore implacably opposed to any policy which aims to promote economic growth. These concerns are focused where there are many possible future scenarios (ie scenario uncertainty), some of which involve apocalyptic levels of resource depletion and land degradation.

These different groups are tackling different problems. I do not believe that those concerned with the structural fragility of the economy really believe that the people paying for the restructure should be the disabled or those on minimum wage. Similarly, there is a big difference between encouraging people to consume less and move to more sustainable lifestyles and recalibrating down what is meant by a subsistence level of existence for those already there.

We do need to worry about too big to fail. Our economy houses too many institutions which appear to be too large to regulate effectively. We do need to reduce levels of debt when economic activity has returned to more normal levels. We will need to restructure our economy entirely for it to make long-term sense in a world where long term limits to growth seem inevitable. But none of these are our immediate concern. We need to save the economy first.