Diagram 1

We are currently behaving like this is the world we live in – because if you are a finance person it is. The Dasgupta Report on the Economics of Biodiversity does nothing substantive to challenge this, despite a foreword from David Attenborough admitting “We are totally dependent upon the natural world”, other than putting a bigger number on the Sustainability portion (Natural Capital). John Kay mentioned in his talk, as part of the Dr Patrick Poon Presidential Speaker series on Finance in the Public Interest for the Institute and Faculty of Actuaries, the habit of actuaries in particular of often “attaching meaningless numbers to data”. There would seem to be great potential for doing precisely this in putting a number on Natural Capital.

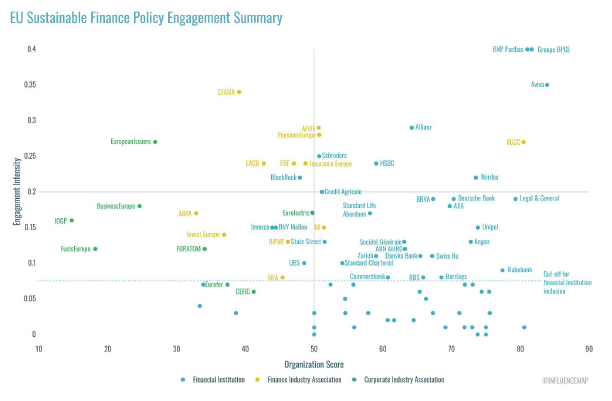

But it is worse than that. As the September 2020 InfluenceMap report on sustainability finance policy engagement makes clear, most financial institutions (bottom-right quadrant, in blue, below) have shown caution and, despite having made some high-level supportive comments, have tended not to engage in a detailed or intensive manner. A small number of financial institutions (top-right quadrant, blue) have been actively engaged in promoting sustainable finance policy. A few financial institutions (centre-left of the diagram, blue) appear to be more cautious about sustainable finance policy.

This chart plots the results of InfluenceMap’s analysis for the financial institutions and industry associations included in the analysis. Engagement Intensity refers to how actively the entity is engaging, while Organization Score measures the degree of support/opposition to policy.

Diagram 2

In the meantime, the IFRS Foundation is proposing to set up a Sustainability Standards Board with its own reporting standards. This is what Richard Murphy (who got me thinking about this in Venn diagram terms originally) is rightly complaining about as it would lead to this:

His sustainability cost accounting idea offers a plausible alternative approach in my view. As the introduction says:

…accounting has to change because we need a clear, audited, enforced and unambiguous indicator of the process of change that business must go through to support continued human life on this planet. Sustainable cost accounting can do that by indicating who can, and cannot, use capital to best effect in this changed environment. That is precisely why it is needed, however uncomfortable the consequences might be.

What is actually needed therefore is clearly an approach rooted in this:

Diagram 3

This is the long term position most working in sustainability would, I believe, like to see. However there are differences of opinion in how to get there.

Kate Raworth argues that you may need to talk within Diagram 1 to start with in order to engage the finance professionals, which of course includes the central bankers and treasury official who might limit the speed at which we could move to Diagram 3. Others disagree, saying once you start talking to finance professionals in their own language, you are condemned to a solution in Diagram 1.

What seem clear to me is that, if our arguments are between Diagram 1 and Diagram 3, perhaps we can dispense with Diagram 2.