In Simon Sharpe’s great new book Five Time Faster, he points out that, if we are going to decarbonise everything, “it’s not just the physical plumbing of the global economy that needs to be replaced, but the intellectual plumbing.” In a blog post from January, Three less visible battles to win, Simon mentions three targets in particular for this intellectual plumbing:

Infrastructure that makes sure heads of government know just how bad climate change could get;

Ideas in economics that exert a critical influence over governments’ policy decisions; and

Institutions in diplomacy that will get the job done.

The first one means targeting the Integrated Assessment Models which have informed so much of our hesitancy and inappropriate prioritisations over the last 20 years where climate is concerned. I have written about this several times before, and this is something actuaries can contribute to much more in the future.

And the third one will I believe become much more tractable once the intellectual tide starts to change.

I will be heading down with my banner to London tomorrow for Extinctions Rebellion’s Big One, alongside 90 other organisations united in demonstrating for a survivable future. Hope to see you there!

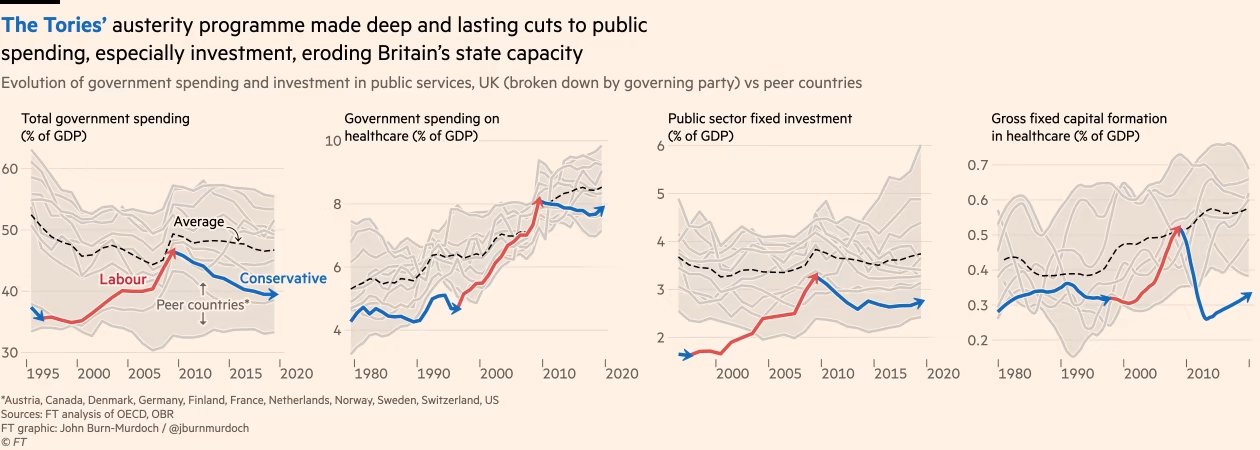

OK I am talking about satisfaction with the NHS a little bit, as it was all over the media yesterday. Just 29% satisfaction compared to 70% in 2010, with the chart above helpfully showing the precipitous decline since then. Does that remind you of another set of graphs I put up not too long ago?

It should. We stopped spending the same proportion of GDP that other similar countries do on their health services and our performance in terms of patient satisfaction plummets. Who would have thought it?

In fact this was only a headline as the Kings Fund and Nuffield Trust had just issued their analysis of the NHS-related bits of British Social Attitudes Survey Number 39, which had originally been published in October, and was itself based on data collected between September and October 2021. However it is an impressive survey overall, with 44,000 households taking part (you can find the full technical details of the survey here).

What is very clear is that the nation is changing fast. Some things are not – a slender majority in favour of increasing taxes and spending more on health, education and social benefits has remained almost static since pre pandemic and all of the averages conceal very polarised views between Brexiteers and Remainers, the different communities in Scotland and Northern Ireland, and particularly between Londoners and the rest of the UK.

This looks like it is beginning to be recognised, with a big increase in the proportion agreeing that working people do not get their fair share of the nation’s wealth (up to 67% compared to 57% in 2019) and, for the first time, a slim majority in favour of moving to proportional representation.

Only 17% say it is very important for being truly British to have been born in Britain, which is down from 48% in 1995, which feels like a sea change in attitudes towards immigration to me.

And then we turn to the environment. Rather echoing the Met Office research I highlighted recently, 45% view climate change as the most important environmental issue, compared with only 19% in 2010, with 40% of the population very concerned about the environment, compared with 22% in 2010.

Which brings us to two climate stories in quick succession.

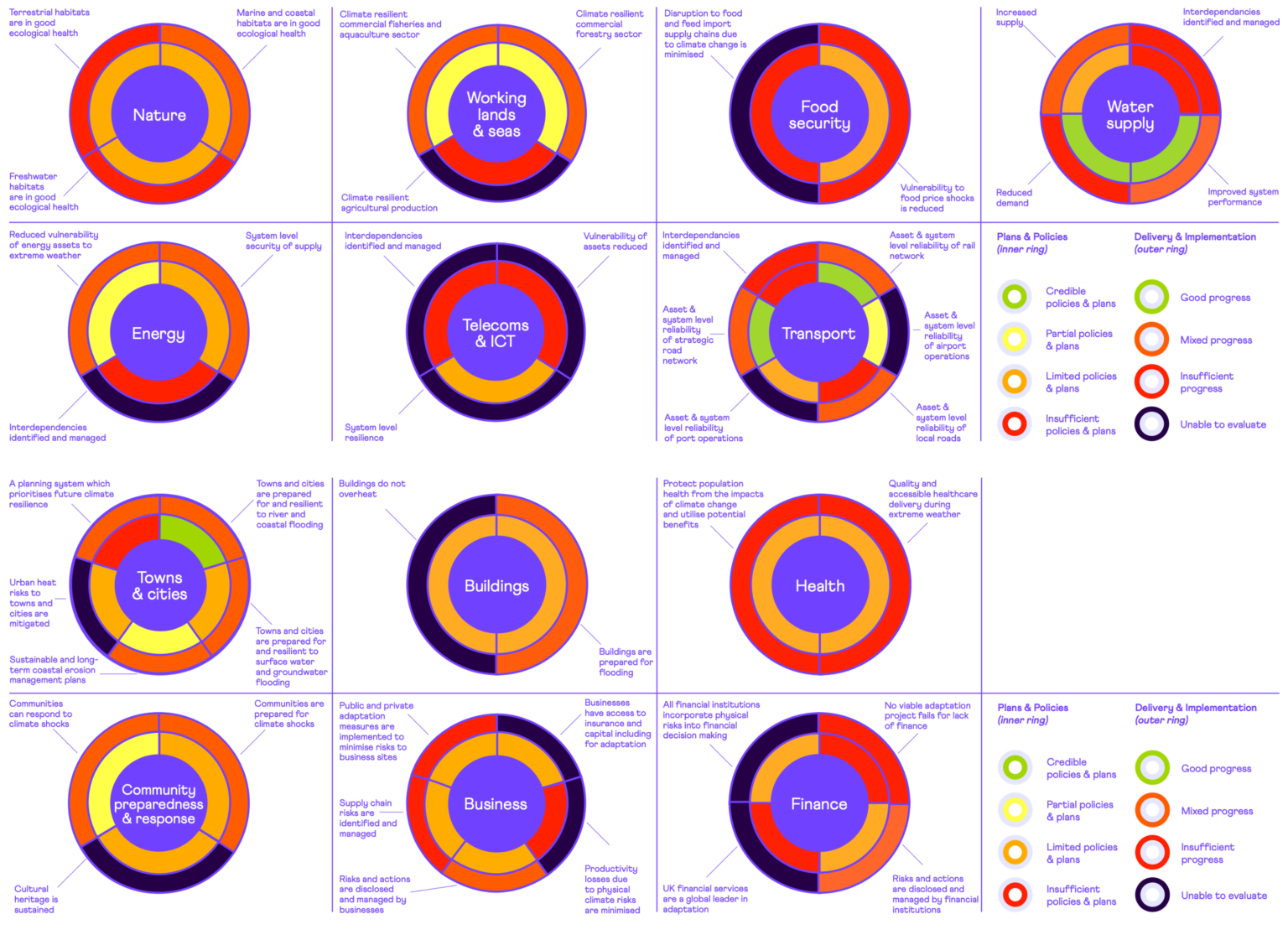

The first was yesterday, when the Committee for Climate Change, appointed to assess the Government’s progress against its own commitments on climate change, gave its 2023 report to Parliament on England’s progress in building climate resilience across the economy – and the extent of policies and delivery to meet them. It was not a positive assessment.

There is a striking lack of climate preparation from Government:

Policies and plans. Despite some evidence of improved sectoral planning by Government for key climate risks, ‘fully credible’ planning for climate change – where nearly all required policy milestones are in place – is only found for five of the 45 adaptation outcomes examined in this report.

Delivery and implementation. In none of the 45 adaptation outcomes was their sufficient evidence that reductions in climate exposure and vulnerability are happening at the rates required to manage risks appropriately. For around one-quarter of outcomes, available indicators show insufficient evidence of progress.

Baroness Brown, Chair of the Adaptation Committee, went further:

The Government’s lack of urgency on climate resilience is in sharp contrast to the recent experience of people in this country. People, nature and infrastructure face damaging impacts as climate change takes hold. These impacts will only intensify in the coming decades.

This has been a lost decade in preparing for and adapting to the known risks that we face from climate change. Each month that passes without action locks in more damaging impacts and threatens the delivery of other key Government objectives, including Net Zero. We have laid out a clear path for Government to improve the country’s climate resilience. They must step up.

By coincidence, today is the Government’s Energy Security Day, backed by a report called Powering Up Britain. This follows a High Court ruling last October which found that, when they signed off their carbon strategy, they didn’t have the legally required information on how carbon budgets would be met. The article went on to say:

Ten million tonnes of carbon could be illegally unleashed in the mid-2030s as a result. Doubt was also shed on the 95 per cent of the sixth carbon budget that was accounted for in the government’s estimates.

Mr Justice Holgate also ruled that the strategy breached the Climate Change Act by failing to provide enough detail on the emissions savings, leaving parliament and the public in the dark.

Originally called Green Day, but presumably dropped after Jeremy Hunt’s comments about not wanting to be an American Idiot, the Energy Security Day has highlighted the following Government priorities:

Energy security: setting the UK on a path to greater energy independence.

Consumer security: bringing bills down, and keeping them affordable, and making wholesale electricity prices among the cheapest in Europe.

Climate security: supporting industry to move away from expensive and dirty fossil fuels.

Economic security: playing our part in reducing inflation and boosting growth, delivering high skilled jobs for the future.

Further analysis at this stage has not been made easy by the way that the Government has released details. Chris Stark, the Chief Executive of the Committee for Climate Change has described it on Twitter as “government by press release”, ie

The government now adopts this communications strategy regularly: press release the night before – published documents later. It gives them two bites of the press coverage.

But it makes it hard for a statutory organisation like @theCCCuk, with legal duties, to comment.

Others have been less constrained in their response. The main criticisms are that many of the policies presented in the report have been announced previously, that there is no significant increase in support for home insulation and that the focus on carbon capture and storage (CCS) is out of all proportion given the long-standing difficulties of scaling up the technology.

The BBC quote Bob Ward, policy director at the Grantham Research Institute on Climate Change at LSE:

What does not make sense is to carry on with further development of new fossil fuel reserves on the assumption CCS will be available to mop up all the additional emissions.

I had an initial skim of the report looking for what was planned for heat pumps, which regular readers of this blog will know I have some history with. I found this:

The Government has an ambition to phase out all new and replacement natural gas boilers by 2035 at the latest and will further consider the recommendation from the Independent Review of Net Zero in relation to this. People’s homes will be heated by British electricity, not imported gas. The Heat Pump Investment Accelerator will mean heat pumps are manufactured in the UK at a scale never seen before. We want to make it as cheap to buy and run a heat pump as a gas boiler by extending the Boiler Upgrade Scheme by three years, and by rebalancing the costs of electricity and gas.

So reading between the hype, they are going to invest £30 million in heat pump manufacture in the UK, which they claim will attract £270 million of “private investment into manufacturing and associated supply chains”.

The other parts are:

Committing to extending the £5,000 grant for another three years (which is less than the difference between the cost of installing a heat pump and a gas boiler currently in many cases, although this may change if schemes like the recently announced Octopus pilot become more widely adopted).

The “Clean Heat Market Mechanism” which is supposed to encourage the installation of low carbon heating appliances.

A consultation to shift green levies off electricity and on to gas bills.

The country is changing fast. The Government needs to be more transformational than this to keep up. Or, in Baroness Brown’s words, step up!

I was looking through my old blog posts the other day and came across something I wasn’t looking for. Actuaries and Science Fiction told the story of a one-off visit I made to the Birmingham Science Fiction Group (BSFG), when the guest speaker had been the late great Brian Aldiss, who told the story of a time Kingsley Amis had had dinner with Margaret Thatcher. He told her what his book Russian Hide and Seek was about, to which she had responded that he needed to get himself another crystal ball.

By coincidence, I have just joined the BSFG nearly 10 years later (well I needed to think about it!), attending my first meeting online (Anna Stephens – really good about writing for Warhammer and Marvel in particular) and now very much looking forward to seeing Alastair Reynolds at my first in person meeting next month. I now have a bit more context for the Kingsley Amis story, as Andy Beckett has an account of a dinner Amis had at Thatcher’s Flood Street house in the late 70s (before she became Prime Minister). He wrote at the time:

I was rather overcome with the occasion and the fairly close propinquity of Mrs T…very much a new face to me as to most people, too much so to take in a lot about the fare except that it was properly unimaginative, and, as regards drink, ample enough. The hostess wore one of those outfits that seem to have more detail in them than is common, with, I particularly remember, finely embroidered gold-and-scarlet collar and cuffs to her blouse…[she was] one of the best-looking women I had ever met and for her age…remarkable.

And he also attributed the following quote to Thatcher herself:

People have always said that the next election is going to be crucial. But this one really will be, and if it doesn’t go the way Denis and I want then we’ll stay [in Britain], because we’ll always stay, but we’ll work very hard with the children to set them up with careers in Canada.

Anyway, back to Aldiss. He had told the story as he felt it showed how Thatcher (and he was not just picking on her as he felt this was a view held by many) misunderstood science fiction. It was not about prediction of the future, but for people who “liked the disorientation” of portraying an unfamiliar landscape.

Ursula K. Le Guin goes further in her introduction to The Left Hand of Darkness (just finished it and, if by any chance you haven’t read it already, it is an amazing piece of immersive world building which will leave you never feeling the same way about gender again). As she says:

Science fiction is not predictive; it is descriptive.

Predictions are offered by prophets (free of charge), by clairvoyants (who usually charge a fee, and are therefore more honoured in their day than prophets, and by futurologists (salaried). Prediction is the business of prophets, clairvoyants and futurologists. It is not the business of novelists. A novelist’s business is lying.

The weather bureau will tell you what next Tuesday will be like, and the Rand Corporation will tell you what the twenty-first century will be like. I don’t recommend that you turn to the writers of fiction for such information. It’s none of their business…All they can tell you is what they have seen and heard, in their time in this world, a third of it spent in sleep and dreaming, another third of it spent telling lies.

And, my favourite bit:

In reading a novel, any novel, we have to know perfectly well that the whole thing is nonsense, and then, while reading, believe every word of it. Finally, when we’re done with it, we may find – if it’s a good novel – that we’re a bit different from what we were before we read it, that we have changed a little, as if by having met a new face, crossed a street we never crossed before. But it’s very hard to say just what we learned, how we were changed.

The artist deals with what cannot be said in words.

The artist whose medium is fiction does this in words. The novelist says in words what cannot be said in words.

Who wouldn’t want to do that? It struck me while I was reading those words how the pandemic was something which changed all us survivors a little (and some a lot of course) and in ways that are often hard to put in words. But we are changed and there is work to do to try and understand how, even if that cannot be completely put in words.

The other thing from the introduction which has stayed with me is Le Guin’s contention that, while we read a novel, we are bonkers: believing in people who have never existed, hearing voices, perhaps even becoming other people. As she says:

Sanity returns (in most cases) when the book is closed.

But what about when you can’t close the book? Are we, to a greater extent, condemned to some level of future insanity? As William Faulkner said:

The past is never dead. It’s not even past.

In 2013 I tried to suggest that actuaries might also be about portraying an unfamiliar landscape and trying to work out what would hold true under different circumstances, and that they should therefore put themselves about a bit more, even if they sometimes made themselves look a bit foolish in the process. As William Hynes reminded me at yesterday’s excellent An introduction to alternative economic thinking event (recording available soon from the Institute and Faculty of Actuaries), the group of economists responding to the Queen’s question as to why noone saw the 2008 crisis coming, concluded:

In summary, Your Majesty, the failure to foresee the timing, extent and severity of the crisis and to head it off, while it had many causes, was principally a failure of the collective imagination of many bright people, both in this country and internationally, to understand the risks to the system as a whole.

If a failure of imagination is the main problem, I would suggest that science fiction must be at least a part of the solution. Looking a bit foolish at times is a bit of a speciality for me, so you probably won’t be surprised to hear that I am devoting most of my time from here on in to an almost certainly doomed attempt to write what Le Guin might regard as a good novel. I have been here before, way back in my pre-actuarial past, and have a nice back catalogue of unpublishable books and rejection letters to look at whenever I forget that I have no idea what I am doing. But if I find myself shouting to noone in particular that what I am trying to say cannot be said in words, I might dare to believe that I am on the right track.

I feel like I have at least three reasons to be cheerful this morning:

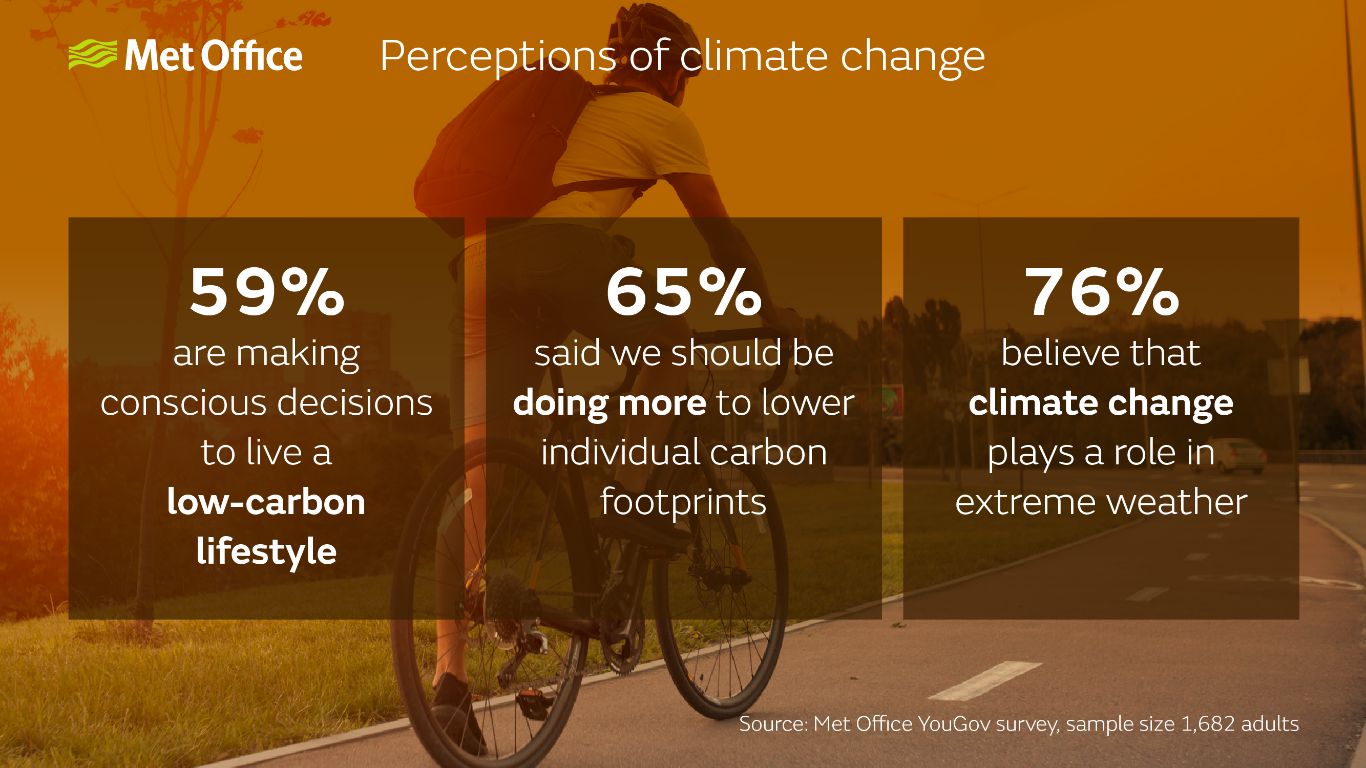

Firstly, the Met Office has released the results of their latest survey (see above) on our attitudes to reducing our carbon footprint and they are very heartening. It seems that most of us are looking up after all.

Secondly, it is also encouraging within the context of Extinction Rebellion’s wider strategy to mobilise 3.5% of the population into campaigning to end the fossil fuel economy and replace it with something better which works for everyone.

On 21 April we will be arriving in London to test out the level of support we now have. My third reason to be cheerful is that an impressive list of other organisations will be joining the demonstration, including Greenpeace, Friends of the Earth, Earth Day, NHS Workers Say No, Greener Practice, Global Justice Now, Black Lives Matter local groups, Don’t Pay UK, CND and the PCS Union.

Meanwhile the Bank of England is pondering whether to raise interest rates even further in response to a vegetable shortage and panicking when the inevitable fall in inflation (which is bound to happen once the comparisons used to calculate it are post the initial price shock) does not coincide with the smooth curves in their models.

And the Government? A reminder of their top 5 priorities:

It becomes easy to see why the XR UK Strategy 2022 document says:

Those in power are neither willing nor capable of acting on the climate and ecological crisis. They lack the courage, conviction and creativity to do what is required.

So it looks like, once again, it is up to the rest of us to do what we have already understood needs to be done.

Seth Godin claims that all successful cultural change has a very simple two step loop to it: of awareness followed by tension and then further awareness, etc.

It does not look like the awareness is so much the issue any more, but what about the tension, ie why should we take action? I think the Government are providing the tension in buckets at the moment.

He summarises with a 3 point plan:

Tell 10 people.

Create tension among the 10 so they take action.

The action causes each of them to tell 10 people.

So this is me creating tension apparently. My wife would say I do that every time I open my mouth. And if 10 of you turn up on 21 April to wave a banner with me I will have a fourth reason to be cheerful!

Photo from the Climate Strike and march in Pittsburgh on 9/24/21. Link from: https://www.flickr.com/photos/9602574@N02/51512352257/. Photo taken by Mark Dixon(https://www.flickr.com/people/9602574@N02). This file is licensed under the Creative CommonsAttribution 2.0 Generic license.

Mark Blyth wrote a great book about how it was a dangerous idea; Simon Wren Lewis described it as a con; Stephanie Kelton defined it as the “deliberate infliction of harm upon society in the presence of alternatives”; Frances Coppola wrote about its terrible price; Steve Keen described it as naive; Mariana Mazzucato, Robert Skidelsky, Ann Pettifor, David Blanchflower and others wrote in the New Statesman on why the UK should not impose it in response to higher debt following the pandemic; and Richard Murphy gave the possible reasons for imposing it as “ignorance, dogmatism and spite”.

What are all of these economists talking about? Austerity. And nearly all of the criticism thrown at this “dangerous” idea is that it does not work economically (ie it will not bring down government debt levels or boost economic growth, the usual justifications given for pursuing it): a criticism for which there is a large and ever growing data set in support.

Now there are any number of Four Yorkshiremen out there to say that this thing we’re calling austerity is luxury and that we are all snowflakes to complain about it, so let’s be clear about what is meant here. Clara Mattei, in her excellent new bookThe Capital Order, describes the three forms of austerity policies: fiscal, monetary and industrial, usually used in combination. Fiscal austerity (reducing public spending, particularly on health, education and benefits and increasing the burden of taxation) and monetary austerity (reductions in the money supply and increases in interest rates) are familiar to most of us and normally the only elements of austerity discussed in the media. To these Mattei adds the idea of industrial austerity, which includes (often described as supply side policies, with the connotation of getting the economy fit to compete in world markets) policies aimed at reducing the negotiating power of workers, from anti-union legislation, to reductions in unemployment benefits, minimum wage levels and wage levels and job security within the public sector.

The contention of The Capital Order is that the reason that austerity has been used again and again in the last 100 years, despite repeatedly failing to achieve the economic goals used to justify it, is that its goals have not been economic but political. The political goal of austerity policies is to defend capitalism whenever events make it seem likely that people will look for alternatives (think World War I or the socialism following World War II or the 2008 crash, or now, the pandemic). Whenever government intervention in the economy has been needed on a sufficient scale to demonstrate that economies can strike a different balance between capital accumulation and labour power, austerity has been brought out immediately afterwards to put labour power back in its box, by making nearly everyone too poor, too busy and too regulated to be able to protest about it.

If this premise is accepted, and I think Mattei makes a convincing case in her analysis of post-World War I austerity policies in Italy and the UK, then the implications are profound. Rather than repeated wrong-headed economic policies by people who do not understand economics, we would instead have deliberate political policies by people who completely understand what they are trying to achieve by them.

The other part of the strategy, via the first international financial conferences in Brussels and then Genoa, in 1920 and 1922 respectively, was to establish an international consensus for policies where “individuals had to work harder, consume less, expect less from the government as a social actor, and renounce any from of labour action that would impede the flow of production.” Lord Chalmers, former permanent secretary at the UK Treasury, summarised this approach as: “work hard, live hard, save hard”. The aim was to return to a pre World War I economic orthodoxy and therefore remove what would be very painful economic measures for most people from the political sphere and into the sphere of “economic science”.

A quotation from the League of Nations in 1920 sums up the how important it was that such a consensus be achieved, to make it extremely difficult for any country to stand against it:

This principle must be clearly brought home to the peoples of all countries; for it will be impossible otherwise to arouse them from a dream of false hopes and illusions to the recognition of hard facts.

These “hard facts” then become the justification for sticking with economic policies, however discredited they might be economically, and buttress them: against alternative economic views (the effective shutdown of the New Approaches to Economic Challenges (NAEC) unit of the OECD being the most recent high profile example) and against popular pressure to change course (eg through such measures as central bank independence from government control over monetary austerity or proposed legislation to limit the scope of political protest).

And of course this effective outlawing of alternative schools of economic thought has other implications too. For example, as Steve Keen has shown, the potential impact of climate change in economic models to date has been disastrously underestimated, allowing fossil fuel lobbyists to delay climate action as a result.

We have all three types of austerity in play at the moment in the UK: monetary, fiscal and industrial. We can either believe that this is designed to force our compliance with the mantra to “work hard, live hard, save hard” even if we do not want to, or that it is for the economic reasons given. The former option requires us to believe that the elites in nearly every government in the world are committed to defending capitalism at all costs and that, if we want to contest this, we will have the political battle of our lives on our hands with the odds steadily more stacked against us with every new piece of legislation passed; the latter requires us to believe that our governments are economically ignorant, dogmatic and spiteful. All our current problems and our solutions to them: from the economic crisis, to the ecological crisis and the increasing political crises globally (what Adam Tooze calls the polycrisis) – depend on what we decide to believe.

“What’s that?” some of you may say. After all I have certainly banged on about climate change quite a bit in the past. Some of you might assume that “Swampy Dave”, as my wife sometimes refers to me in conversation, would be installing a heat pump or solar panels or wind turbines or perhaps all three. Am I not a total hypocrite?

To which the answer is yes. I am a total hypocrite. And I must say the episode has left me chastened and a little bit reluctant to discuss it. It is, as Stephen Fry describes it very well here, one of the strongest reasons that people amongst the 1% like myself do not campaign more about the climate emergency.

But I have begun to think that this is all a massive piece of self-indulgence on my part (and of course, by making it all about me, it is). So, instead, I have decided to make it all about me, by talking you through the Gas Decision or GD for short, because it has certainly clarified for me why we are not transitioning from fossil fuels more quickly.

Our gas boiler has been on the blink for a bit, but coaxed along by our local gas engineer who, I think out of concern for minimising costs to us, was reluctant to suggest any major action if it could be delayed. Then it started to leak water, slowly at first, and then faster, before giving up the ghost altogether in early November. I had during the boiler’s demise had one or two conversations about what we might replace it with. Raising the idea of heat pumps got me puffed out cheeks and rolling of eyes and the opinion that it was very complicated.

I looked online. There is a page called “Find a heat pump installer” on the gov.uk website, with long lists which you can search by distance from your postcode. I chose a couple of nearish ones and contacted them. No response. I then tried Octopus (our supplier, OVO, were not offering heat pump installation), who said they were run off their feet trying to install heat pumps and had a 6 month waiting list. However they did have a referral system, where you could enter your details and installers on their list would contact you.

I tried this and got a couple of calls. Neither local. We chose one who sounded particularly helpful on the phone and made an appointment for their sales person to come round. They were very persuasive, and we subsequently arranged to have the energy performance survey necessary to proceed. This established that about half of our radiators would need replacing, but that our piping was fine. We had had quite a bit of discussion about where the heat pump should go, and were thinking possibly between the first floor windows so that it wouldn’t be humming (or whatever noise heat pumps make) whenever we went out in the garden. We even had the National Grid come round to check that our connection could cope with the additional electricity demand (they had assumed at first that this was for an electric vehicle charging point, as this is apparently the most common reason for calling them round).

The cost of installation, even with the £5,000 Government grant, is at least £5,000 more than a gas boiler. We had been told that we would save money on energy once it was installed, but the savings turned out not to be significant (if there were any at all) once the full calculations had been done. The reason for this is how much more you pay for each kWh of electricity compared to gas. OVO currently charge us 9.83p per kWh for gas (with a standing charge of 27.12p per day) and 32.11p per kWh for electricity (with a standing charge of 46.8p per day). So, despite the heat pump being massively more efficient than the gas boiler alternative, it would really have to be going it some to overturn these price differences.

But, at that stage, we were still prepared to go ahead with the installation (I refer you to the “Swampy” comments above), we just needed to speak to some previous customers to reassure ourselves about their overall experience, perhaps see (and hear) it in situ, etc. And then it unfortunately started to unravel. Despite describing themselves as the number one heat pump installer in the UK, the company we had engaged were unable to provide us with anyone in or near Birmingham willing to tell us about their experiences (they eventually produced one name, but we couldn’t get a reply from them). So we started looking at the reviews on Trustpilot, etc, which were decidedly mixed and talked a lot about poor after sales service, and which seemed to be very dependent on the particular engineer doing the work. And the ones for the heat pump they were planning to install were full of stories involving the installers and the manufacturer pointing the finger at each other when things went wrong. Suddenly it seemed like too big a risk to take.

Meanwhile, the unseasonably warm autumn had slid into a very seasonably freezing December and we needed to get working radiators again. And so we decided we didn’t have time to go out to the heat pump market again, with more surveys etc, and plumped for a replacement gas boiler for our existing system. I am not particularly proud of the decision, and perhaps we were just unlucky with our experience, but it does seem to me that we are not making it easy for people to choose heat pumps in the UK currently. This appears to be borne out by the Department for Business Energy & Industrial Strategy’s UK Energy in Brief 2022 report (p13), which shows that, of the 19.4% of energy supplied from low carbon sources in 2021, only 0.7% was from heat pumps. As Chris Stark, Chief Executive of the UK’s Climate Change Committee, has tweeted recently: “THE MOST IMPORTANT THING is to make electricity cheaper than gas for consumers. It should be a key objective for Treasury’s tax policies and BEIS energy market reforms. It will transform the economics of low-carbon heat.” I certainly think it would have transformed our decision.

And today is the day! The weather outside is frightful (it hit minus 6 as the installation vans arrived and needed the doors thrown open to let in all the gear), but our new piece of fossil fuel infrastructure is being installed as I type. I will at least be a warm hypocrite.

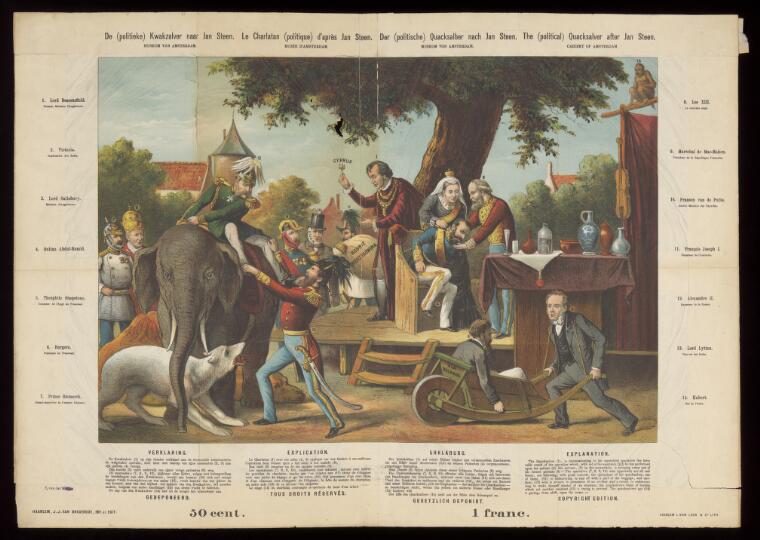

The Congress of Berlin: Disraeli as a tooth-drawer, assisted by Queen Victoria, operates on Sultan Abdul Hamid II of the Ottoman Empire, surrounded by political figures from France, Germany etc. Coloured lithograph by J.J. van Brederode after Jan Steen, 1878. (Steen, Jan, 1626-1679 Reference: 778482i)

If you think COP27 is just a virtue-signalling tree-hugging “gathering of people in Egypt” then Rishi Sunak’s decision not to attend it will make a lot of sense as he tries to grapple with his domestic economic agenda ahead of the autumn statement next month. The Treasury has said that the aim of the statement will be to “to put public spending on a sustainable footing, get debt falling and restore stability.” If you remember, the cause of the “instability” was the foreign exchange and gilt markets, and the lack of confidence in the UK’s economic management internationally. One of the causes of the problems with the UK’s economic management was a failure to think internationally.

COP27 is, in reality, an important international economic conference. This conference is going to be focused on, amongst other things, food security, water security and investing in the future of energy. The support with energy bills is, of course, a major element in the debt levels Sunak is worrying about and, as the cost of living crisis worsens (exacerbated by the Monetary Policy Committee’s expected further increase in interest rates on 3 November), food security is going to rapidly move up his agenda in the coming months. The only difference between the most important concerns of the autumn statement and COP27 are therefore timeframes. COP27 is about medium to long-term thinking. Sunak has indicated, by not attending, that he is only concerned with short-term thinking.

Then there is the agenda around providing a just transition to a net-zero world (ie not skewed in favour of the already wealthy countries) and the sustainability of communities made vulnerable by climate change. This is where the conference starts to resemble other famous international conferences of the past which made the reputations of British statesmen. The illustration above is from the Congress of Berlin in 1878, when the then Tory Prime Minister, Benjamin Disraeli, “acquired” Cyprus in a great powers carve up of the globe. In 1944, towards the end of the second world war, John Maynard Keynes famously sparred with Harry Dexter White from the US Treasury at Bretton Woods as the post-war economic consensus was thrashed out at an international economic conference. They matter.

Of course we don’t carve up the globe any more, you may think, but yes we do. As George Monbiot has pointed out in his excellent Regenesis, the ghost acres (ie the the area, outside their own land, that farms need to operate) of UK agriculture can be as much as 2-3 times as many as the acres we farm domestically. A WWF report from 2020 suggested that the UK’s overseas land footprint has increased by 15% on average compared to their 2011-15 analysis. Between 2016 and 2018, an area equivalent to 88% of the total UK land area was required to supply the UK’s demand for just seven agricultural and forest commodities – beef and leather, cocoa, palm oil, pulp and paper, rubber, soy, and timber. Every time we insist on domestic economic growth as a non-negotiable element of our economic policy, we are effectively exercising a land grab in the global south to achieve it. If Sunak was interested in establishing himself as an international statesman, he would be at COP27.

And finally, of course, there is the terrible human rights record of the Egyptian state, which needs to be called out and challenged to avoid COP27 being just a public relations victory for the military regime led by General Abdel Fatah al-Sisi.

But Sunak has turned his back on all of that, so that he can spend a bit more time with the spreadsheets and economic forecasts in his bunker in Downing Street. It suggests a small-minded, short-term thinker, lacking in vision and ambition. Copping out should not be an option for any Prime Minister, even during a crisis.

We do it all the time. We assume that the animals around us experience the world as we do, with our obsession with the visual sense. We are used to anthropomorphising animals in our cartoons, but it goes much further than that: for instance if, like a dog, your sensory world or Umwelt is primarily based on smell rather than sight, then that daily walk you take with your dog has very different highlights and notable features (amazingly the slits on the side of a dog’s nostrils allow it to smell on out-breaths as well as in-breaths). We have sayings based on these anthropomorphisms: for example, the “unconcerned” frog in the water as it is heated to boiling (cited by Emily Maitlis in her recent speech in Edinburgh) may not be unconcerned at all, merely showing its distress by filling the air with smells like peanut butter, cashew nuts or curry rather than via the reactions we would expect from a human.

Our vision is not even all that extraordinary compared to some other animals. Mantis shrimps have more classes of photoreceptors covering the ultraviolet spectrum than we have in total. They are the only animals who can detect circular polarization, where the plane in which the light is polarized also rotates. However they are much worse than us at telling our visual range of colours apart and may not even have a conception of colour as we know it at all. We don’t know.

We are not even sure how many senses there are. Aristotle said there were five (sight, hearing, smell, taste and touch), but missed our senses of proprioception (ie awareness of your own body) and equilibrioception (ie sense of balance). There are also animals who have a secondary system for detecting odours, or who detect the body heat of their prey via their brain’s visual centre or have sensors which both detect electric fields and pressure. How should we categorise these and does a clear division between senses make any sense? We don’t know.

Elephants can hear each other several miles apart just after sunset, but we don’t know what they are listening for. Beaked whales have a range of crests, ridges and bumps on their skulls which are not outwardly visible other than via the echolocation they use, but we don’t know why.

And finally, for now, the cuttlefish of the title. When cuttlefish sense sharks, who have passive electroreception (ie the ability to detect electric fields in other animals), they stop moving, hold their breath and cover their gill cavities to reduce the voltage of their electric fields by up to 90%. I could go on, but all of this and so much more is contained in Ed Yong’s masterful An Immense World, which I could not recommend more highly, not only for the content but also for the wonderful joyful writing throughout (AC/DC’s Rock and Roll Ain’t Noise Pollution even gets a mention!).

The recurring theme for me is how much we still don’t know about all of these animals, and the amazing new discoveries which are being made every year. Every animal perceives a different world from the one we think we are living in, many of these perceptions currently (and in some cases perhaps permanently) impossible for us to understand. It takes an extraordinary level of anthropomorphic arrogance for us to convert all of those strange and wonderful lives into the concept of natural capital.

The Institute and Faculty of Actuaries’ Biodiversity and Natural Capital Working Party defined natural capital in their paper from April 2021 (which acknowledges the concerns I am raising here and those raised by others) as follows:

The concept of ‘natural capital’ therefore aims to recognise nature as an asset and aims to ensure that the goods and services offered by nature become a part of decision making by governments, businesses, and individuals regarding resource allocation, growth and development.

The Dasgupta Review has gone further, focusing on the economics of diversity. As it acknowledges:

The Review has developed the economics of biodiversity by viewing Nature in anthropocentric terms. That is an altogether narrow viewpoint, but it has a justification. If, as we have shown in Part I, Nature should be protected and promoted even when valued solely for its uses to us, we would have even stronger reasons to protect and promote it if we were to acknowledge that it has intrinsic value.

I strongly disagree. As George Monbiot pointed out several years ago, markets change the meaning of the things we discuss, replacing moral obligations with commercial relationships. The latest article in The Actuary magazine on natural capital discusses ecosystem collapse in its final paragraph in terms of how it would “negatively impact GDP” and “economic value”.

Once the diversity of nature can be reduced to a monetary amount or metric value, it can obviously be modelled much more easily but, as we have seen again and again within the finance sector and elsewhere, that is at the expense of consideration of any other aspect of our relationship with it.

Perhaps cuttlefish do dream of the passive electroreception of sharks. If they only knew what we were up to, they might instead have nightmares about their balance sheet entries in our spreadsheets.

Side by side images en:User:Ittiz created to show what Mars might look like at various stages while being terraformed in vertical alignment. The horizontal alignment is here: en:Image:MarsTransition.jpg http://commons.wikimedia.org/w/index.php?title=Image:MarsTransitionV.jpg&oldid=11571800. This file is licensed under the Creative Commons Attribution-Share Alike 3.0 Unported license.

Terraforming was a concept I first remember coming across in Star Trek 2: The Wrath of Khan in 1982 when “The Genesis Device”, and its effect on a dead planet, was described as “matter is reorganised with life-generating results”. The astronomer Carl Sagan had previously proposed the planetary engineering of Venus in 1961 and Mars in 1973. Martyn J. Fogg subsequently started publishing articles on terraforming in 1985 before publishing Terraforming: Engineering Planetary Environments in 1995. Fogg defined planetary engineering as using technology to change the global properties of a planet (he called this geoengineering if Earth was the planet in question). Terraforming he defined as planetary engineering which was specifically directed at enhancing the capacity of a planet to support life as we know it.

There are still advocates of terraforming as a project that humans should be actively working towards. Others suggest, that unless Earth is going to be unavoidably uninhabitable, it is likely to be our best bet as a future home for all but a relatively tiny number (Kim Stanley Robinson’s novel Aurora is the most memorable advocate for this position in my view, which takes us on a gruelling exploration of a terraforming expedition over several generations which then allows us to view Earth afresh with alien eyes).

What is clear is that we are not currently terraforming Earth in Fogg’s sense, as most of our planetary engineering (what we call the global economy) appears to be specifically directed at reducing the capacity of Earth to support life as we know it. We are terraforming in reverse.

Terraforming is an example of an idea you might get to as a result of very long-term thinking (there is a nice article about this in Vox, with views from Roman Kznaric, Nick Beckstead, Hilary Greaves and William MacAskill included) – I tend towards the Kznaric view that we cannot predict the knock-on effects of technological shifts in 200 or 300 years, but we know we’ll still need to breathe air and drink water, so working to prevent climate change and pandemics is very likely to be really good for us today, the near future and the long-run future too.

The danger of discussion of the very long-term is that it can create the idea that nothing we do over the next few years matters. However as we have pushed up to and beyond planetary capacity in so many areas now and have developed a global economy with planetary engineering capabilities of unprecedented power, this is no longer true if it ever was. What seems obvious to me is that we mustn’t make decisions now which lock in damage to planetary life-supporting capacity for generations to come, such as the “carbon bombs” described by George Monbiot here.

Terraforming in reverse is not the direction to choose, whichever generation we belong to.

Imagine all of the fossil fuel energy available to the Earth and its inhabitants before our emissions from using that energy mean that we will have, on average, a climate 1.5oC warmer than pre-industrial levels. Imagine it as a big black ball located, for convenience, in China, as we have exported many of the most carbon-intensive manufacturing processes we all need there, and that we are all sucking the energy we need from this black ball 24/7 until it is exhausted.

The last estimate of the size of the ball came from the IPCC AR6 Report of 2021, which indicated that the remaining carbon budget to remain with a 50% chance of staying at or below 1.5°C of global warming is 580 billion tonnes CO2 and about 420 billion tonnes CO2 for a two-thirds chance of limiting warming to 1.5°C, all as at 2018. Annual global CO2 emissions in 2019 were 36.7 billion tonnes, in 2020 they were 34.8 billion tonnes and in 2021 they rebounded to 36.4 billion tonnes. So that ball is shrinking very fast.

Why the obsession with 1.5°C? Well, it is what we and most other countries signed up to in Paris in 2015. 2°C was agreed to be a much worse outcome than 1.5°C – we can already see the results of current warming where 20% of the global population lives with 1.5°C warming in at least one season of the year, but a global average of 2°C compared to 1.5°C would increase the proportion of the population exposed to severe heatwaves at least once every 5 years from 14% to 37%. NASA have an article on this here.

Can we make the ball bigger, by removing some of the carbon dioxide? If you look at the pathways that the IPCC discuss, you will see that they are split between those where temperatures are stabilised at or below 1.5°C warming and those which go above but are then brought back down later in the century. In its most recent report published in April, the IPCC said the use of CO2 removal is now “unavoidable”, if the world is to reach net-zero greenhouse gas emissions. Where the UK is in its programme of carbon removal is discussed here. However, to get it into perspective, global carbon removal to date is still in the experimental stage, and there are many problems remaining to be overcome with most of the proposed methods, so such efforts must be additional rather than in anyway an alternative to drastically cutting our emissions.

Back to the ball. If this represented all of the remaining water in the world (the scientific consensus at 3°C warming has Indian monsoon rains failing, the Himalayan glaciers supplying the Indus, Ganges and Brahmaputra, the Mekong, Yangtze and Yellow rivers decreasing by up to 90% and the Amazonian rain forest basin drying out completely), would you think about it differently? Would you continue washing your car every weekend, watering your lawn, and power-washing your drives and patios on the assumption that we would invent a new way of making water? Simon Brodkin has done a good bit in answer to this, which is both very funny and terrifyingly plausible.

{kind=link}