You will have all seen the work mug staple: “The Difficult We Do Immediately. The Impossible Takes a Little Longer”. The original quotation in the title, originally attributed to Charles Alexandre de Calonne, the Finance Minister for Louis XVI, in response to a request for money from his Queen, Marie Antoinette, appeared in a collection from 1794, this was a year after Louis and Marie Antoinette (but not Charles, who survived another nine years) died on the guillotine and five since George Washington had been inaugurated as the first President of the United States. It seems as if the seemingly impossible may need to be attempted once again.

So let’s start by expanding on the problem which I brought up in my last post. The problem goes much wider than Donald Trump. He is assembling a court of loyalists around him, in the style of a mob boss, which as has been observed by others, has been the prelude to fascism in the past. As Jason Stanley, Professor of Philosophy at Yale and author of Erasing History: how fascists rewrite the past to control the future, puts it: “the United States is your enemy”. There is also considerable circumstantial evidence to suggest that Trump is considered an agent of influence by Putin’s regime in Russia.

The difficulty of what I am about to suggest is also the reason why it is so urgent: our relationship with the United States (the one we keep needing reassurance by successive US Presidents of its special nature) is positively symbiotic. George Monbiot lists some of our vulnerabilities here:

- Through the “Five Eyes” partnership, the UK automatically shares signals intelligence, human intelligence and defence intelligence with the US government. The two governments, with other western nations, run a wide range of joint intelligence programmes, such as Prism, Echelon, Tempora and XKeyscore. The US National Security Agency (NSA) uses the UK agency GCHQ as a subcontractor.

- Depending on whose definitions you accept, the US has either 11 or 13 military bases and listening stations in the UK. They include RAF Lakenheath in Suffolk, from which it deploys F-35 jets; RAF Menwith Hill in North Yorkshire, which carries out military espionage and operational support for the NSA in the US; RAF Croughton, part-operated by the CIA, which allegedly used the base to spy on Angela Merkel among many others; and RAF Fylingdales, part of the US Space Surveillance Network. If the US now sides with Russia against the UK and Europe, these could just as well be Russian bases and listening stations.

- Then we come to our weapon systems… among the crucial components of our defence are F-35 stealth jets, designed and patented in the US.

- Many of our weapons systems might be dependent on US CPUs and other digital technologies, or on US systems such as Starlink, owned by Musk, or GPS, owned by the US Space Force. Which of our weapons systems could achieve battle-readiness without US involvement and consent? Which could be remotely disabled by the US military?

- Then there is our independent nuclear deterrent, which is “neither British nor independent” according to Professor Norman Dombey, Emeritus Professor of Physics and Astronomy at the University of Sussex.

Then there is the sheer cost of rearming with Europe to the extent necessary in the absence of the United States’ support, suggesting 3.5% rather than 2.5% of GDP is what will be required, suggesting the UK Government, with its WCAIWCDI approach described here, will need to find something in addition to the foreign aid budget to ransack. I will be talking more about defence spending in a future post.

It is small wonder that some commentators, such as Arthur Snell, former Assistant Director for Counter-Terrorism at the Foreign and Commonwealth Office, conclude that disentangling ourselves from the United States may be impossible. And that is just considering defence and security considerations.

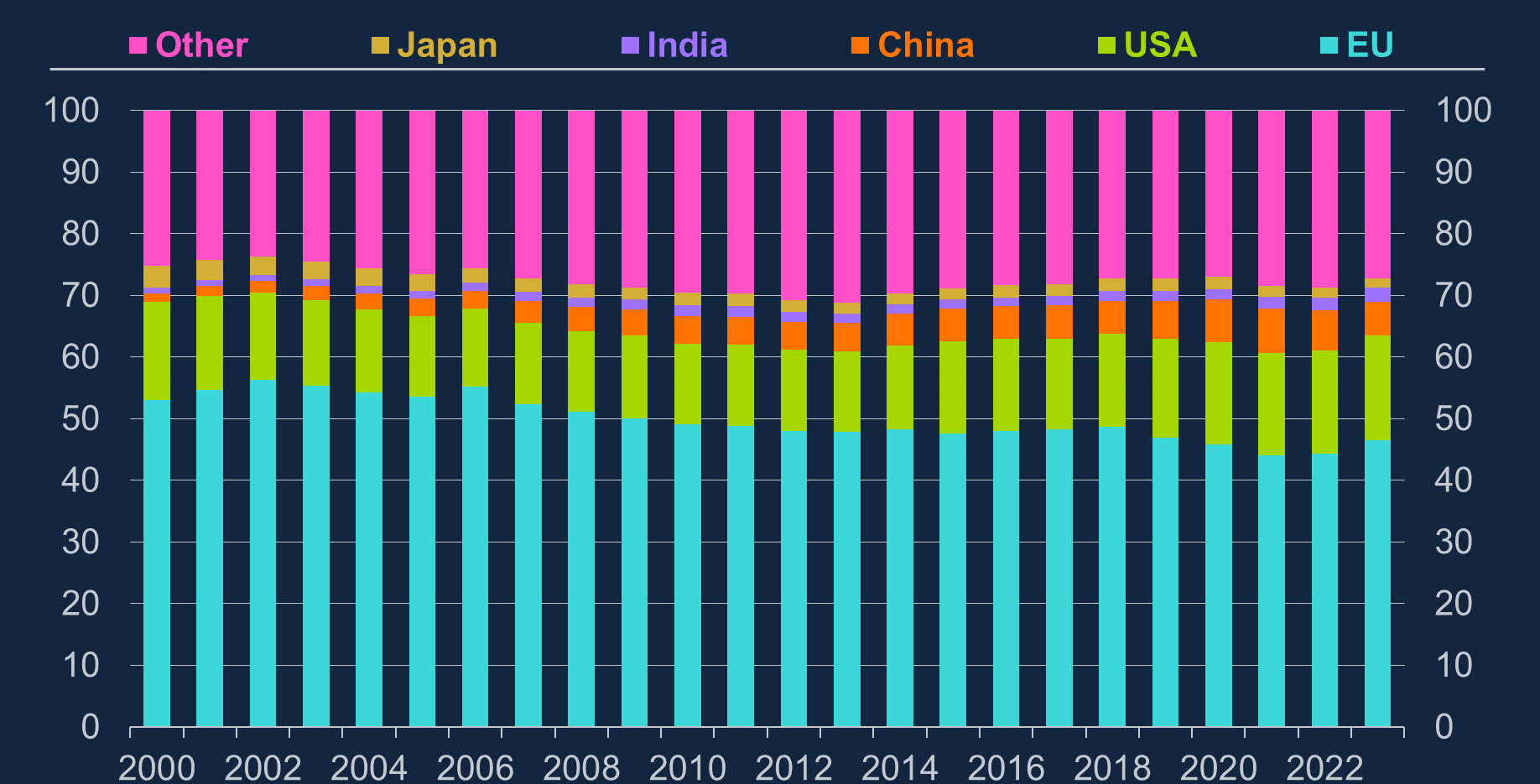

On the economy the symbiosis is just as evident. First of all there is the sizeable proportion of our imports and exports of both goods and services which are with the United States. Only in June 2023, we were trying hard to develop these further with something called the Atlantic Declaration. Although, as a recent speech by Megan Greene of the Bank of England’s Monetary Policy Committee shows, our trade with the US as a proportion has remained remarkably stable since 2000 at least.

Culturally, the United States is embedded in our laptops and mobile phones, our television programmes and movies, and our social media. Its concerns have permeated our language and our politics. A reasonable proportion of our political and financial elite have been to their universities and theirs to ours. Many of our employers have US parents: just in the actuarial world, two of the three biggest consultancies (Aon and Willis Towers Watson) are described as British-American firms, with the other one (Mercer) headquartered in New York. It has Apple. It has Amazon. It has Google. It has Meta and, of course, X.

And perhaps the greatest entanglement of our two countries is political, to the extent that we routinely send our politicians to each other countries to support election campaigns and our media breathlessly report every in and out of the US Presidential elections. We are lucky if a French or German one is mentioned more than a couple of weeks before it takes place. Whether it is the language thing (we are still VERY resistant to learning other languages) or the post imperial thing (feeling like we have a special understanding of the problems the United States face as a self-appointed global police force) or the degree of financialisation of our economy or for some other reason, it is very hard to avoid a sense of being conjoined with the United States of America.

But it is precisely because our relationship is so close in so many important areas that we are particularly vulnerable to US pressure – the harder it will be to disentangle ourselves, the more urgent it is that we do.

As David Allen Green puts it this week, the US is currently undergoing a diplomatic revolution. Originally applied to France’s realignment of all of its alliances away from Prussia and towards Austria, which ultimately led to the work mug motto at the start of this piece, the US appears to be realigning itself towards Russia and away from the UK and the EU. As Green goes on to say:

Other countries would now be prudent to regulate their affairs so as to minimise or eliminate their dependency on the United States – it is no longer a question of waiting out until the next United States elections.

And other political systems would be wise to limit what can be done within their own constitutions by executive order, and to strengthen the roles of the legislature and the judiciary (and also of internal independent legal advice within government).

The last seems key to me. We cannot, particularly now we are outside the EU, afford for our main ally to be capable of being so capricious. This applies whether the US are allowed to and do elect a President in 2028 who is respectful of its institutions and constitution. We always felt Americans were very respectful of their constitution because they never stopped talking about it, but it turns out to have been a thin veneer with little meaning. Much like our discussion of sovereignty in the UK.

The first thing we need to do is to stop obsessing about what John Mulaney memorably referred to as a “horse in a hospital” in 2019. Despite the fact that was five years ago and we have now seen a horse in the hospital before, many have been turned off news coverage altogether by the anxiety caused as a result of the constant media narration of what Trump and Musk have done next each day. The dangers of treating the Trump and Musk chaos as a TV show are potentially existential in the US but grave for us in the UK too.

While we may have deep sympathy for the people in the US and other countries caught up in the chaos, our priority has to be to get our own house in order. Otherwise we won’t be any help to anyone.

My priorities would be the ones I set out in October 2022, only now with much greater urgency.

- We can’t have parties with only 20% of the popular vote (34% of a 60% turnout) having an absolute majority of 174 seats. We need proportional representation, so that every vote counts equally and perhaps we might get somewhere near the turnout of Germany’s last election of 82.5%.

- Reform media ownership and promote plurality in support of a more democratic and accountable media system. The Media Reform Coalition has produced a manifesto for a people’s media which I support: it includes proposals for an Independent Media Commons – with participatory newsrooms, community radio stations, digital innovators and cultural producers, supported by democratically-controlled public resources to tell the stories of all the UK’s communities. As we know, our social media is controlled by Meta (with Facebook, WhatsApp and Instagram), all of which have more than 2 billion active users and Google with YouTube, also with more than 2 billion active users. X still has over half a billion, despite what Musk has done with it. In newspapers, 90% of daily circulation is controlled by three firms: News UK, Daily Mail Group and Reach plc (which has most of the local titles you’ve ever heard of, including the Birmingham Mail and Birmingham Live, as well as The Daily Express and the Daily Star).

- Reform election finance. Recommendations for doing this were provided in the July 2021 report by the Committee on Standards in Public Life. There was an eye-watering amount of money spent in the US Presidential Election this time: The Democrats spent $1.8 billion and the Republicans $1.4 billion, with $2.6 billion and $1.7 billion respectively being spent by the two parties on the Senate and House races. In the UK, paradoxically, the relatively small amount of money donated to parties mean that they are potentially more vulnerable to well organised lobbying operations. This is why the offer of $100 million by Musk to Reform led for calls to restrict foreign political donations to profits generated within the UK.

This way we would be more resilient to the many ways that the current chaotic United States establishment can reach into our own politics and governance, and start to develop policies with broad support which can reduce our dependency on the United States.