I thought it was about time I collected together some of my cartoons from the last 11 years in one place, so have created a page for them which you can see here. Not sure if I am getting any better as the years go by, but rest assured that I have no intention of stopping any time soon!

Posted on LinkedIn on 4 June 2024

This is just a quick personal note to explain the imminent end of my LinkedIn account.

LinkedIn became an important tool for me in 2014 when I became a Lecturer at the University of Leicester and Programme Director for the BSc Mathematics and Actuarial Science there: to connect with potential students and guests to the university, to link up with former students, to publicise the activities of the Leicester Actuarial Science Society and to facilitate a professional network which would be useful to our current and former students. I also posted a few articles here along the way. However I will be leaving the University of Leicester on 30 June and moving to retired status with the Institute and Faculty of Actuaries soon afterwards. Therefore the description I have given myself here (Actuary, Lecturer and Writer at the University of Leicester) will at that point become almost entirely untrue! It therefore seems like an appropriate time to wind up my account here.

According to the latest analytics, I have around 1,400 connections on LinkedIn. Thank you to everyone who has connected with me over the years, particularly if we worked together in some capacity. I have managed to work with some wonderful people over the last 10 years. A particularly big thank you to all of the students who have made the job so enjoyable during that time.

Of those 1,400 connections, over 400 of you list the University of Leicester in your profiles. If you are a current or former student, or indeed anyone who needs to be in contact with a member of the Leicester actuarial team and are currently only connected to me, you should ensure that you are connected to at least one of the following excellent colleagues of mine: Leena Sodha, Paul King or Nigel Sell. You should, in addition, as a current Leicester student, join the LinkedIn group Leicester Actuarial Science Society. If you are a former Leicester student, the group you want is Leicester Actuarial Science Society – Alumni.

I will continue to be in various actuarial WhatsApp groups for the time being and on X (@weknow0). And, if you like any part of what I write, you can always subscribe (for free!) at weknow0.co.uk. For those of you who still want to keep in touch with me by email once I have left here and my Leicester email address has been discontinued, and we have not already shared alternative contact details, please send me a message on LinkedIn (or weknow0.co.uk) and I will be in touch.

With my best wishes for the future to you all.

The Telegraph thinks the shareholders are to blame. The Guardian has the Australian investment bank Macquarie in its sights. Martin Bradley’s (the European Head of Infrastructure at Macquarie Asset Management) attempts in Infrastructure Investor at justifying their actions only seem to be making things worse. The FT is using it as an excuse to have a go at the Capital Asset Pricing Model. Count Binface has included in his manifesto for the London Mayoral election a requirement for the company’s management to “take a dip in the Thames, to see how they like it”.

I am talking of course about Thames Water, which really does appear to be everywhere at the moment. But how did we get here?

The management of water works by private companies was originally a legacy of the Victorians – most of the water supply and all waste water services moved into local government control from the late 19th and early 20th centuries. Control then passed from 165 different water supply bodies to 10 regional water authorities in 1974 before these were sold back to private companies in 1989.

Water is obviously a resource vital to all of us, as well as being what economists call a natural monopoly. There have been debates for quite some time now about renationalising the water industry – some arguing that it is too expensive and that a Welsh Water not-for-profit model is the answer, others saying that water, electricity and Royal Mail together would cost less than £50 billion to nationalise and would pay for themselves within 7 years if investors were just repaid what they had invested in the businesses, others saying that water is a failed business and could be acquired without compensation for shareholders as happened with Northern Rock.

What none of these appear to be arguing is that private monopolies should not exist as a reason for renationalising water. We have become so used to monopoly or oligopoly profits in everything from utilities to transport to mobile phones to supermarkets, that we sometimes forget that it has not always been like this.

This point was made to me powerfully in Cory Doctorow’s excellent The Internet Con – How to Seize the Means of Computation. The 19th century debate in the US Senate about monopolies was impassioned. Senator John Sherman of the 1890 Sherman Act effectively put the war against monopolies on an equivalent footing with the War of Independence from the British Crown:

If we will not endure a King as a political power we should not endure a King over the production, transportation, and sale of the necessaries of life. If we would not submit to an emperor we should not submit to an autocrat of trade with power to prevent competition and to fix the price of any commodity.

It’s stirring stuff. The “harmful dominance” theory of antitrust (ie the idea that companies which dominate an industry are potentially harmful just because they are dominant, before they even start to abuse their dominant positions) led to the dismantling of several “empires”, including that of Rockefeller’s Standard Oil Company in the early 20th century.

But then enter Robert Bork. Famous amongst other things for having an extremely dull taste in video rentals, Bork was Solicitor General of the US between 1973 and 1977, under Presidents Nixon and Ford, and Acting US Attorney General from 1982 to 1988 under President Reagan. Bork developed what he called a “consumer welfare” theory of antitrust. This allowed mergers and monopolies to proceed provided prices were lowered and/or quality improved, or even if they weren’t as long as some “exogenous factors” could be blamed for the price hikes or reduction in quality.

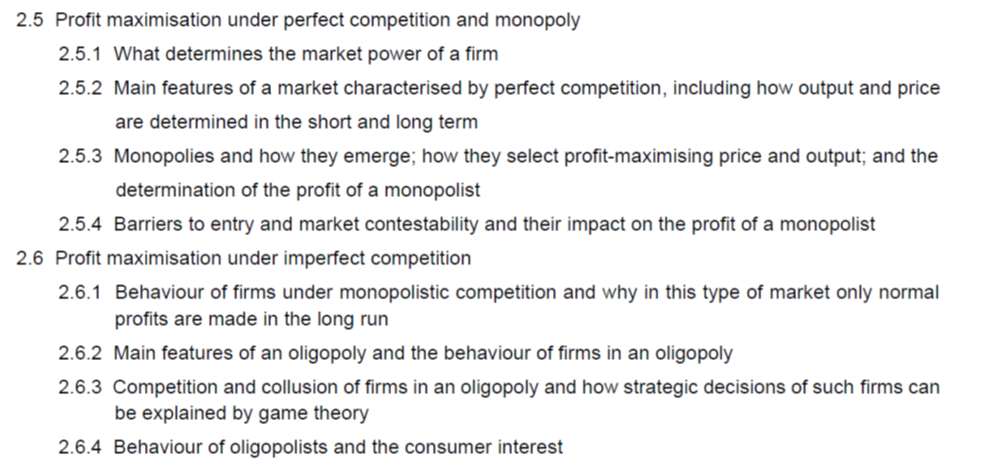

Sound familiar? It should, as we all still live in Bork’s world. For example, the microeconomics part of the Institute and Faculty of Actuaries’ Business Economics syllabus relating to imperfect markets reads as follows:

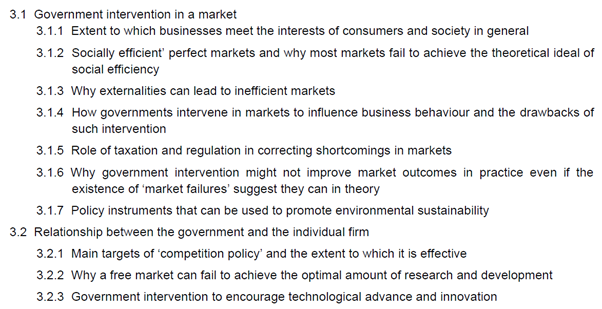

Note the focus on the different ways firms supposedly maximise profits (this approach is fairly thoroughly debunked by Steve Keen here) rather than on the market power they wield. The part which should include the regulation of monopolies reads as follows:

Note the lowering of expectations in 3.1.6: “Why government intervention might not improve market outcomes in practice even if the existence of ‘market failures’ suggest they can in theory”. However the real limitations are laid bare in 3.2. The main targets of “competition policy” in the text book (Economics by Sloman et al) you are pointed to by the core reading turn out to be what are referred to as “exclusionary abuses”, ie where businesses actively prevent effective competition from actual or potential competitors. As the preamble on competition policy in Sloman says:

Competition policy could ban various structures. For example, there could be restrictions on mergers leading to market share of more than a certain amount. (This is the harmful dominant approach, about which no more is said) Most countries, however, focus on whether the practices of particular monopolists or oligopolists are anti-competitive. Some practices may be made illegal, such as price fixing by oligopolists; others may be assessed on a case-by-case basis. Such an approach does not presume that the existence of power is against the public interest, but rather that certain uses of that power may be.

So, in other words, we will leave monopolistic businesses with the power and attempt to detect abuses of that power on a case-by case basis via overworked and under-resourced regulators. Sherman could have never cut Standard Oil down to size with this approach.

Yanis Varoufakis’ contention, in Technofeudalism, is that capitalism now only operates within the framework provided by the most extreme monopolists of Big Tech, with most of us either “cloud proles” (ie wage slaves working for Big Tech under feudal conditions) or “cloud serfs” (ie the rest of us working for Big Tech for free by creating content and sharing our data on their platforms). Big Tech’s size massively increased as a result of the bank bail out of 2008 and additional money pumped through them and the corporations working for them coupled with austerity for everyone else, which was therefore almost totally financialised – leading to the “everything rally” for asset owners.

As Varoufakis says:

When an activist state makes fabulously wealthier the same bankers whose quasi-criminal activities brought misery to the majority, while they are punished with self-defeating austerity, two new calamities beckon: poisoned politics and permanent stagnation.

Again, sound familiar?

It is not too late to push back against the monopolies which control our lives. Doctorow’s big idea in The Internet Con is interoperability, the ability of new technologies to plug into Big Tech’s services, systems and platforms, which Big Tech tends to resist with all of the power at its disposal. He makes a convincing case for how this simple change could reduce the size of Big Tech companies quickly and bring them within the scope of democratic control once more.

And for those businesses which need to be at monopoly scale to work at all? Water, for instance. That sounds like an unanswerable case for nationalisation to me. Perhaps assuming that dominant private companies are bound to be harmful needs to come back into fashion.

So the proposals which I wrote about last month have been reconsidered by the newly elected Institute and Faculty of Actuaries (IFoA) Council on 15 October, where they agreed some tweaks to the original proposals as follows:

Council devised and ultimately voted for revised measures based on the member feedback it had received on the previously approved reforms. You told us that you wanted the new President and Council (2023-2024) to reconsider the reforms and we agreed this at our meeting on 1 September 2023. You told us that you wanted better communication and more engagement and we have embarked on one of the biggest member engagement exercises in our history which will continue next year into the role of Council. You told us that you were uncomfortable with the idea that actuaries would be in the minority on the board. We have responded by changing the makeup of the new IFoA Board so that it will continue to have a majority of actuaries. You told us that you wanted safeguards to ensure the IFoA Board could be held to account and that a “bad board” could not self-perpetuate. We have responded by ensuring that appointments of members and independents to the IFoA Board will need to be ratified by Council on first appointment and every 3 years for the remainder of their term.

So am I happy now? The answer is no in some respects and I don’t know in others. No I am not happy that a member vote still seems to be proposed for 2026, giving this proposal the inside track to becoming the final permanent governance structure by only asking for a vote after most of us will have become quite hazy about what went before it.

I don’t know because we are still not going to be given sight of any part of the DAC Beachcroft report to which these proposals are supposed to be a response. We are therefore being asked to completely trust the description of what was in it by the very people trying to sell us their proposals. That is a big ask in my view.

However it is also difficult to raise any formal objections to the proposed amendment to Regulations 2, 3, 4, 5, 6, 10, 11, 12 and 13 in this state of enforced ignorance. I will therefore be raising the concerns I have set out here by contacting the Corporate Secretary at the IFoA. If you feel that you can go further and formally object on the basis of what you have or have not been told, then those objections should be raised by 30 January to be considered.

Perhaps I am making too much of what I don’t know, but I was struck by the references here to any future consultation being confined to the role of Council, with the rest of the governance structure seemingly regarded as done and dusted. Also if you watch to the end of the little video there, you are confronted with this message:

Is our ability to continue to self-regulate at all really under threat? I would have expected to be told rather more about why this is before being asked for my views in a member organisation such as the IFoA.

I accept that many of the IFoA’s functions may need a more streamlined system to run them effectively. There are many different alternative structures which we could consider to achieve this. But these proposals are about changing the very nature of the IFoA and that requires full disclosure to members about why we are doing this and a chance to vote before we do so in my view. More than a tweak, in other words.

We have been here many times before, even in recent memory. The 2008 banking crisis, memorably immortalised by the Steve Bell cartoon above; the MPs’ expenses scandal the following year; the successive disappointments of Brexit; and now the the Post Office Horizon scandal. All of these had in common an initial public expression of outrage, followed by loud condemnations of aspects of it from within the Establishment, followed by a series of measures which generally failed to change anything substantive. So the ring-fencing legislation brought in to isolate the risk taking within banking from retail customers has steadily been lobbied against and is now gradually being unravelled. MPs continue to have expenses scandals. I don’t know how to encapsulate in a sentence the Muppet Show of how the Establishment has been trying to deal with Brexit since 2016. And now this.

The Post Office scandal seems to be being discussed everywhere: beyond the TV, radio and social media, it is in the pub, the supermarket queue, in families and workplaces. The Establishment condemnation is already underway, as pithily summarised by Marina Hyde here. I do not really care about the implications for the honours lists, but very much hope that the sub-postmasters and sub-postmistresses get the compensation they are seeking. However this time the response cannot stop there.

As David Allen Green has written in Prospect today (with a great overview of what has happened from a legal point of view), the scandal also represents a failure of the legal system. This was partly caused by the repeal, in 1999, of the part of the Police and Criminal Evidence Act 1984 which presumed in favour of individuals rather than computer systems. This has been particularly unfair in these cases as the evidence defendants needed to show that Horizon was at fault often remained undisclosed by the Post Office. It was also caused by the Post Office’s eagerness to pursue private prosecutions.

Coincidentally, I came across the concept of private prosecutions a couple of weeks ago while reading the excellent Butler to the World: How Britain became the servant of tycoons, tax dodgers, kleptocrats and criminals by Oliver Bullough (which also suggested to me that I should revisit the issue of Scottish Limited Partnerships soon, but I digress). As Oliver points out:

Under measures introduced in the post-2010 austerity agenda, defendants…have no prospect of reclaiming their expenses from public funds if they are convicted. Even if they’re acquitted, they can only get their expenses back if a request for legal aid has previously been turned down…Meanwhile, private prosecutors – whether individual or companies – can claim back all reasonable expenses if they lose. Financially speaking, a private prosecution is a one-way bet. As long as you can afford the upfront cost of bankrolling the case, you’ll get your money back because under common law you are acting on behalf of the Crown.

David Allen Green has called for private prosecutions to be abolished, which I would agree with. But I also think the burden of proof needs to be returned to the operators of computer systems in what I predict will become increasingly frequent human-expert system disputes in the future. In fact we need to go further than that and have a full public consultation into what legal protections individual humans will need in a world increasingly driven by decisions and calculations made by non-human systems.

Over seven years ago I wrote an article in response to Cathy O’Neil’s excellent Weapons of Math Destruction, where she set out the case against devolving important decisions to mathematical models without adequate feedback loops. I said then (with an Oppenheimer reference too!) that:

If mathematical models are to be the dominant regulatory tool of a financial world, and of the consultancies and financial firms competing in that world, then the time will come when mankind will curse the names of the highly paid professionals who followed inappropriate rules rather than exercising their own expert judgement when it mattered.

It is starting to look like we may be there already unless we act fast.

When I was nearing qualification as an actuary at the turn of the century, one of the recommended texts for both the specialist pensions (the then equivalent of SP4 and SA4) exams was Alastair Jollans’ 1997 paper to the Staple Inn Actuarial Society (SIAS) entitled Pensions and the ageing population. At the time there was quite a lot of actuarial comment about how superior a funded pension system was to a pay-as-you-go system and the example of Chile in particular. The following sentence from Alastair’s paper stuck with me at the time:

It is also clear that the Chilean scheme made a huge psychological difference, and this may be one of the major advantages of funding.

Meanwhile the Labour Government had been moving to reform the State Earnings Related Pension (SERPS) with its Green paper of 1998 A new contract for welfare: partnership in pensions, and replace it with a new State Second Pension (S2P). It had two aims – giving more help to people for whom private pensions were not an option and helping moderate earners to build up better second pensions through the introduction of stakeholder pensions. The intention was that S2P would become flat-rate over time with the following reasons given for this (bold mine):

Although SERPS is an efficient second pension, it is earnings-related. It does least for those on low incomes who have most difficulty in building up a good second pension. Many people on modest incomes will also receive limited benefits from SERPS or from the private provision they may make instead.

So the limitations of the current system (where the new State Pension has replaced S2P and auto-enrolment has replaced stakeholder pensions), as previously discussed here, were recognised from the outset of the experiment of moving to funded pensions.

Fast forward to now and Chile’s system is tottering, leading to mass protests. It turns out that the psychological advantage of its funding approach was only an advantage for those that could afford it, whereas the 40% who gained no benefit from invested funds (a remarkably similar proportion to the UK statistics) preferred the psychological advantage of a guaranteed state pension. Even the FT admits it needs reform, although fairly technical in nature:

At the very least, a sensible reform now should be to eliminate the investment limits by asset class and introduce an investment policy based on risk metrics at the portfolio level. The government should also relax the restrictions on alternative investments and eliminate the ill-designed hedge requirements.

The Council on Foreign Relations was less restrained in 2022:

Pensions were never a good fit for strictly private management, as basic building blocks of the welfare state are definitive public goods. Yet the failure of the system has reverberated beyond the retirees trying to make ends meet. Pensions became a leading cause for the millions of Chileans who took to the streets in protest in 2019, spurring the formation of a Constituent Assembly to write a new Constitution that will be voted on in September.

The best path for pensions would be a reform that ensures adequate retirements for more Chileans. This requires a more robust public system with dedicated funding to sustain it. If legislators can make this happen, they can reduce the financial hardship too many of Chile’s elderly now face. And, to the benefit of democracy in both Chile and its neighbors, they could also thereby restore at least some of the political legitimacy that the old system helped to put in doubt.

In my first post in this series, I explained why the State Pension needs to be much bigger than the Triple Lock is ever going to get it to. The second post then moved on to discuss the leaky pensions budget and what to do about it. In this third and final post in the series, I focus on why increasing pensions should be a priority when there is so much destitution in all parts of our society.

We are living in anxious times, with discomfort about the state of the world now so extreme that many of us are disconnecting from it and, instead, treating it as a personal mental health challenge requiring breathing exercises and mindfulness and radio programmes like Radio 2 Unwinds with Angela Griffin and similar. This follows a pattern with other crises, where we have been encouraged to abandon collective action to protect our pay and conditions by ever more onerous anti-union legislation or to abandon collective action to combat climate change by ever more onerous anti-protest legislation. Instead we are constantly encouraged to look inward and focus on our own wants and the things about ourselves which are standing in the way of those wants, ie to approach the world solely as a consumer. It is much more convenient for the companies working in the retail markets if we all behave this way.

Moving away from the collective provision of state pensions for all to a reasonable level and instead towards the individual provision of funded occupational pensions follows this pattern. However, as we have seen, many have been left in poverty without any asset security as a result of this move. This leaves them more vulnerable to sickness, debt and generally less resilient to the uncertainties of the future.

Seth Godin recently blogged about the engineering philosophy essential to creating something both useful and fit for purpose. It involves asking who is it for and what is it for.

Increasingly I feel that we have lost sight of these two questions in how we provide pensions, my answers would be:

- Who is it for? Everyone.

- What is it for? To increase people’s resilience.

In the case of resilience, the discussion has been kept at a, in my view deliberately, high level of abstraction so that most people feel that it is not their concern. McKinsey produced a particularly incomprehensible example here, but it is probably unfair to pick on them as they are just one of many, and they did at least mention societal resilience. A great technique for excluding people from the discussion is to produce a proliferation of definitions which noone can agree on (five were identified in this article in Nature by Rockstrom et al, for instance). However, as Rockstrom identified, in essence a resilient system needs just five characteristics:

- Diversity, ie support comes in multiple forms and does not assume everyone is the same;

- Redundancy, ie if one part of the system fails, there is always a good Plan B and mechanisms available to replace system failures quickly and efficiently;

- Connectivity, ie our supply chains are diversified and the resources we need drawn from a wide range of sources, and our populations are kept well connected with each other and the services they need;

- Inclusivity and equity; and

- Adaptive learning, ie we review whether the system is working reasonably frequently and learn from experience.

So what would be gained from increasing the state pension for all?

- Marginalising older people when their bodies already feel less resilient and forcing them into the boxes required by our processes of means-testing are likely to extinguish many of these voices from the national discussions we need to have. A significant increase in pensions for all, instead of the ridiculous triple lock which is only tolerated as it slowly gets us to this goal without having to have the discussion about what a decent pension would be, is what is needed.

- A larger state pension would give us all more security through redundancy, ie a decent baseline underneath the other sources of income. Our invested pensions are not as diversified as they look and very vulnerable to a range of system-wide events and our means-tested benefits are very frequently prone to error and delay. The prospect of this greater level of security and certainty in retirement would also ease the burden of many working age families who are supporting older relatives, and the effects would therefore extend well beyond the retired population.

- Poverty crushes the diversity of a population, as the cartoon above from the UN Special Rapporteur on poverty Olivier de Schutter makes clear. We need diverse people with diverse thought and we need to include them in our society and listen to what they have to say.

- Focusing on those of retirement age to allow them to live better will save money in other areas. According to a Guardian study, an 85-year-old man costs the NHS about seven times more on average than a man in his late 30s. Health spending per person steeply increases after the age of 50. It would also reduce reliance on an inefficient and fragmented disability benefit system.

- Increasing the state pension would obviously have a much greater effect at the bottom half of the income deciles than at the top and would therefore have a big impact on inequality. As the Institute of Fiscal Studies said of increases to the minimum wage for working people between 2011 and 2021:

...inequality in male earnings rose between 1980 and the Great Recession, driven by rising wage inequality at the top and rising hours inequality at the bottom. This trend appears to have stopped in the last decade, as growth in the minimum wage outstripped wage growth further up the distribution, and hours worked stopped falling disproportionately for low-wage men.

Increases to the state pension would be likely to have just as dramatic an effect.

And we all gain from a more equal society, even those we redistribute away from. As the Equality Trust have shown in their research, high levels of income inequality are linked to economic instability, financial crisis, debt and inflation; less social mobility and lower scores in maths, reading and science; an increase in murder and robbery rates; reduced longevity, more mental illness and obesity, and higher rates of infant mortality. People in less equal societies are less likely to trust each other, less likely to engage in social or civic participation, and less likely to say they’re happy.

My view is that we need to start somewhere in creating a more equal, and therefore more resilient, society here in the UK. And I would start with pensions.

My favourite bit of Scrooged is when Bill Murray is told that the people working in a homeless shelter cannot be fired because they are volunteers. It appears that the Institute and Faculty of Actuaries (IFoA) is instead in danger of morphing into such a sleek, streamlined, efficient, simplified and clarified organisation that noone would want to volunteer for it any more.

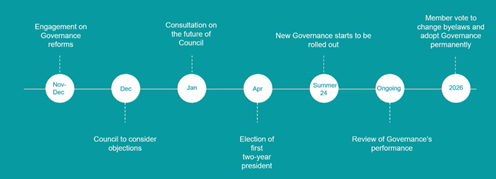

The long-running argument about the future governance of the IFoA grinds on. Four months after a small number of members alerted the rest of us to what was going on, and 194 members then objected in writing, the IFoA have now concluded a series of webinars explaining the proposals. I attended the final one on 28 November.

In a nutshell, the proposals are unchanged from those objected to, they are now being considered alongside the objections by the newly elected Council this month, which will be followed by a full consultation in January. The new governance structure will then be rolled out in the summer of 2024 and a member vote only allowed on the new structure two years later in 2026. Yes that’s right, not a typo: 2026!

The session I attended was all about how we needed to be more streamlined, more efficient, more credible in our governance. We needed to simplify our governance, clarify it. The recent embarrassments about outgoing CEOs was cited as an example of our poor governance without explanation. The independent report which they quoted from throughout to justify the proposals will not be provided to members as it includes contributions from people who only did so on the basis of anonymity.

There was a discussion about how the IFoA was both a business and a member organisation. But, in mentioning more than once how the proposals were only what any of the organisations members worked for would expect from their governance, the weighting given to these two roles was very clear. These were senior business leaders attempting to make the IFoA look more like the businesses they are more used to.

If you’re a senior business leader, then an organisation where any member can have some influence on its direction of travel must be incomprehensible. They are used to leading and being followed. Much was made of the waste of time that much Council business involved, and I am sure that is right. But that is just a motivation for change, as indeed was the entire presentation on 28 November. It was decidedly not a motivation for this change in particular.

We were told that other options had been considered, although bundling everything up into one board that did everything was the only one mentioned.

One of the other reasons given for the changes proposed was how much bigger the IFoA was now. Coincidentally, on 27 November, the Economic Affairs Committee of the House of Lords published its report ‘Making an independent Bank of England work better’. In it they made the following point:

The growth in the Bank’s remit has not been met with a commensurate increase in accountability and Parliamentary scrutiny. While an independent central bank reassures markets, critically important economic decisions are delegated to unelected officials. The Committee is concerned that a democratic deficit has emerged, which risks undermining confidence in the Bank and its operational independence.

We are being asked to quietly acquiesce to the creation of precisely this kind of democratic deficit in our own member organisation. Because, despite suggestions to the contrary in the webinar, we are primarily a member organisation and not like the organisations we all work for, something we have just been reminded of by being charged £750 for the privilege.

If we agree to this timetable, then by the time we get to 2026 I predict we will be assured that it would not be cost effective or a good use of the new unitary board’s time to uproot what will by then be the incumbent system. This would be giving these proposals an unfair advantage in deciding on the long-term governance of the IFoA.

My requests would be:

- Some summarised form of the independent report which protects people’s anonymity but allows us members to judge for ourselves the relative strengths and weaknesses of the analysis of our current governance and the options so far considered for change.

- An opportunity for a member vote on the structure adopted in 2024 alongside the consultation, rather than 2 years post adoption.

It is precisely at the stage of deciding that structure that all of the range of experience, talent and wisdom of the membership needs to be deployed, not at the point of rubber stamping a decision already made. If you agree with me that members are being sidelined in the decision-making process about the very nature of the IFoA’s future, then please send your feedback to governance@actuaries.org.uk.

In my previous post, I talked about out how dependent the bottom half of the income scale was on the state pension of £10,600 pa, and how an increase of at least 40% to the state pension was needed to reset the balance between a guaranteed income and that based on the markets to European levels.

However there was another aspect of the state pension which I did not mention last time and which also needs to be addressed.

Who gets it?

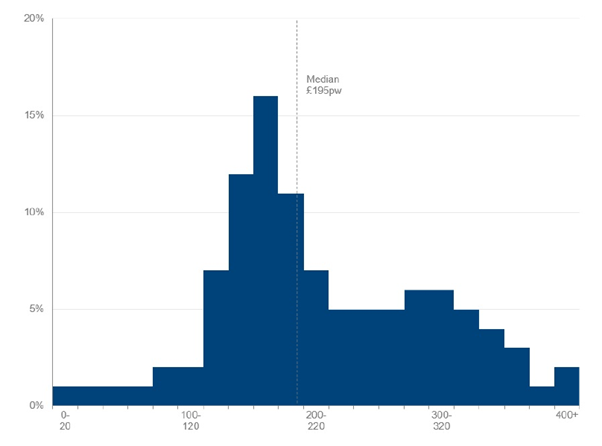

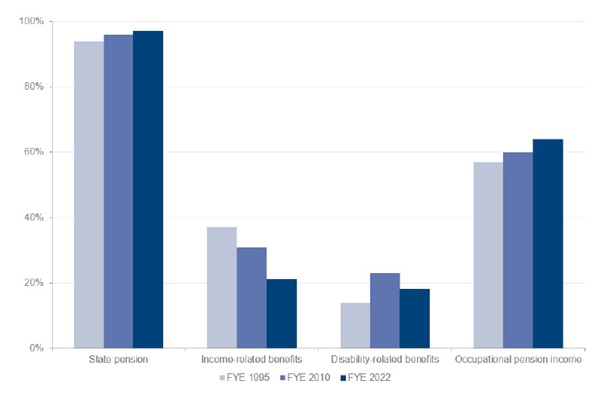

As the graph above shows, by no means does everyone get the full state pension (although legacy state benefits mean that some get considerably more).

As the Undefined Benefit: Fixing the UK Pensions System report mentioned in my previous post explains:

To qualify for this full state pension, an individual needs to have made 35 years of National Insurance contributions or have equivalent credits. To qualify for any fraction of the state pension, an individual must have made at least ten years of contributions or have equivalent credits. Thus, even the UK’s first pillar, the state pension, is to a degree contribution based. This stands in contrast with countries such as Canada, Mexico, the Netherlands and New Zealand, which have adopted a residence-based, non-contributory basic pension. Residency-based pensions increase coverage and seem to be effective in reducing poverty rates in old age.

How much?

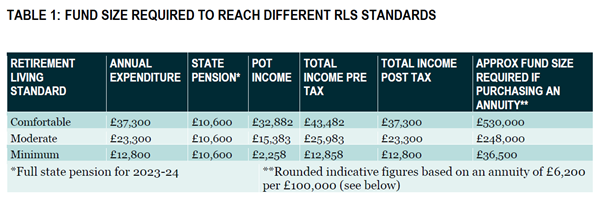

Returning to the PLSA’s retirement living standards again, we have the following:

You will note that the retirement living standards assume:

- income tax is payable;

- people are mortgage and rent free; and

- it also does not cover care costs.

The minimum level would then require a 21% uplift to the basic state pension, assuming no meaningful private or occupational pension assets (which we saw last time was a reasonable assumption for most of the bottom half of the income scale).

According to the Government’s figures, in 2020-21, 5% of all older households (ie where the household “reference” person was 65 or older) were mortgagors, 6% were private renters and 15% were social renters (down from 19% in 2010-2011). The remaining 75% of older households were outright owners (up from 71%). So we are going to need more for our minimum level to meet the needs of the 25% who are still paying rent or mortgages. The average household income spent on rent amongst older renters is 38% for private renters and 27% for social renters.

Assuming this household income is the basic state pension and the average housing costs of the group we are concerned about (ie totally or almost totally dependent upon the state pension) are in line with social housing rent, we would need an additional 37% uplift to the state pension (to mean that taking 27% of it would get you back to where you started) to 66% of state pension, ie a total of £17,600 pa before the latest state pension increase. If you are aiming for the moderate retirement living standard you would need over twice as big an overall state pension at £35,600 pa.

Means-tested benefits

At this point, if you are shouting at your phone or computer “but you are ignoring means-tested benefits!” you would be correct. Age UK give a handy guide to means tested benefits, but in a nutshell we have:

- Cold Weather Payment – £25 a week for each 7-day period of cold weather. This only applies between 1 November and 31 March each year.

- Council Tax Support – there is no set amount of Council Tax Support. What you get depends on your circumstances and where you live. Each local council is responsible for operating its own Council Tax Support scheme so the amounts of support given across the country may vary.

- Housing Benefit – Housing Benefit is money to help you cover your rent if you’re living on a low income.

- Income Support – this is going to be fully replaced by universal credit by the end of 2024. Universal Credit has come in for a lot of criticism – this is the Trussell Trust’s take on it.

- Pension Credit – the bit of this that we are interested in is the Guarantee Credit, which tops up your weekly income to a guaranteed minimum level. In 2023-24, this level is: £201.05 if you’re single and £306.85 if you’re a couple (note that these are still below the levels of the basic state pension).

- Universal Credit – for a single person over 25 this is currently £368.74 per month but there are many circumstances which can lead to deductions to this amount and the Trussell Trust (see above) has this to say about it:

These are at the lowest levels in 30 years and aren’t protecting people from destitution, meaning they are unable to afford the essentials we all need to eat, stay warm and dry and keep clean.

The trouble with means-tested benefits are:

- Not everyone claims them. An FT article from April 2022 claimed that there were £15 billion of unclaimed means-tested benefits – for a variety of reasons, but with lack of internet access (18% of older households) being a major one. This compares with £5 billion currently spent on Pension Credit and £6 billion spent on Housing Benefit for over 65s, so you can see the size of the problem here;

- They create, in some cases, high effective marginal tax rates for people who want to earn a little extra income, by removing benefit as income increases;

- If a benefit is not universal, there is a danger that the recipients will become so marginalised that their voice is no longer strong enough to defend it, and people might not feel like full citizens of the society they live in. Applying for benefits requires admitting poverty which can be humiliating;

- Means-tested benefits are often poorly targeted. The Report of the UN’s Special Rapporteur from 2019 on extreme poverty and human rights, whose recent comments gave me the title for this post, included the following amongst its 11 recommendations: Initiate an independent review of the efficacy of changes to welfare conditionality and sanctions introduced since 2012 by the Department of Work and Pensions;

- There are good reasons for people not to want to claim means tested benefits, as the UN report says: The basic message, delivered in the language of managerial efficiency and automation, is that almost any alternative will be more tolerable than seeking to obtain government benefits.

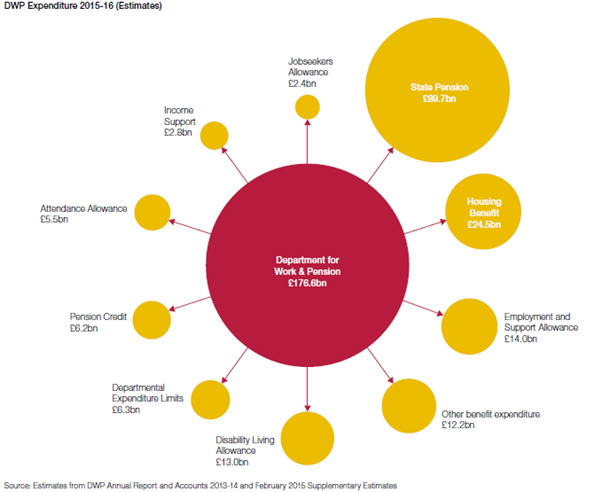

- Means-tested benefits cost a lot to administer. The latest National Audit Office guide to the Department of Work and Pensions (DWP) for instance (from 2015-16) indicates the following split:

Of a total budget of £176.6 billion, departmental expenditure in addition to benefit expenditure was £6.3 billion. Attempts to reduce this figure since 2016 appear to have resulted in big increases to under and over payments. Simon Duffy of Citizen Network, who has looked at this extensively and attempted to compare the net benefit to recipients to the total administrative costs including those of the tax system, estimates that, to make people £1 better off, the DWP spends £0.22.

It therefore seems to me that, in order to provide a guaranteed minimum level of living standards in retirement, not dependent upon pensioners being invested in the right way, or filling in the right forms or their employment history, and not vulnerable to the punitive sanctions currently applied to conditional benefits like Universal Credit, we are going to need a state pension somewhere north of 66% above its current level. So how do we pay for it?

How do we pay for it?

My very rough estimate of the amount required to top up everyone below the full state pension in the graph at the top of this post is around an additional 23%.

The current state pension cost around £110 billion pa in 2022-23 or 4.4% of GDP. Allowing for the Pension Credit, Housing Credit and Winter Fuel Allowance at half their current levels following the increase to state pension proposed (a very conservative estimate I believe, which also does not include the smaller increase that those on legacy benefits will need) brings it up to 4.75% of GDP. So what I am proposing would cost up to an additional £73 billion pa in state pension or an additional 2.9% of GDP, or a total of 7.65% of GDP plus the 23% uplift required to top everyone up to the full state pension bringing it to 9.4%, which would put us above the current OECD average of 8% of GDP, although still less than is currently paid by Italy, Greece, France, Austria, Portugal, Finland, Spain, Poland, Belgium, Slovenia and Germany. It is therefore something that we can afford to do in the world’s 5th largest economy if we make this a priority.

These additional payments of around £125 billion would result in immediate increased income tax payments (assuming all at the 20% rate) of £25 billion plus the ONS estimate between 18% and 28% of the poorest 40% of households’ income is spent on indirect taxation, averaging 23% or £29 billion. However, as Richard Murphy has pointed out, there is currently a risk that millions of pensioners will have to complete tax returns (in many cases for the first time) next year due to the triple lock bringing pension levels above the frozen personal allowance. HMRC will therefore need to be reformed so as to be able to collect tax on pensions via PAYE and allow pensioners to receive net pensions in future.

My view is that raising the guaranteed state pension to a level which will be sufficient post tax is preferable to just lifting the personal allowance above the new state pension level. Why? Because:

- Everyone would get the new personal allowance, reducing taxation of the wealthiest as well as the poorest, with no particular benefit to the poorest; and

- One of my problems with means tested benefits is that they marginalise people so that they do not feel like full members of society. The same applies to not paying tax. If you pay tax, you are more likely to want a say in how that society is organised.

Some options for funding more than the remaining balance of £71 billion, picked out from Richard Murphy’s very conservative estimates here, are as follows:

- Ending higher rates of tax relief on pension contributions. This would raise £14.5 billion in tax a year;

- Abolishing the VAT exemption for financial services within the UK might raise £8.7 billion of additional tax revenue pa;

- Reforming national insurance charges on higher levels of earned income in the UK might raise an additional £12.5 billion of tax revenue pa;

- Aligning capital gains tax and income tax rates in the UK might raise more than £12 billion in additional tax a year;

- Reforming the administration of corporation tax in the UK might raise at least £6 billion of tax a year;

- Abolishing the inheritance tax exemption on some funds retained in pension arrangements at the time of a person’s death might raise £1.3 billion a year;

- Reforming inheritance tax business property relief might raise £3.2 billion of tax a year;

- Reforming inheritance tax agricultural property relief might raise £1.0 billion of tax a year;

- Reforming Companies House might raise £6 billion of tax a year;

- Reintroducing close company rules for income and corporation tax could raise at least £3 billion of tax a year; and

- Abolishing the domicile rule for tax purposes might raise £3.2 billion of tax revenue a year.

I am sure you would have your own list. And you may not agree with the size of guaranteed state pension increase I have suggested. And I fully admit that these are very approximate figures made to illustrate what might be possible. However I hope I have made a reasonable case for what would be required as a guaranteed income for all pensioners if it were a political priority.

Next month, I will be attempting to tackle the question of why it should be a priority or, in other words, what would be gained by increasing the state pension for all?

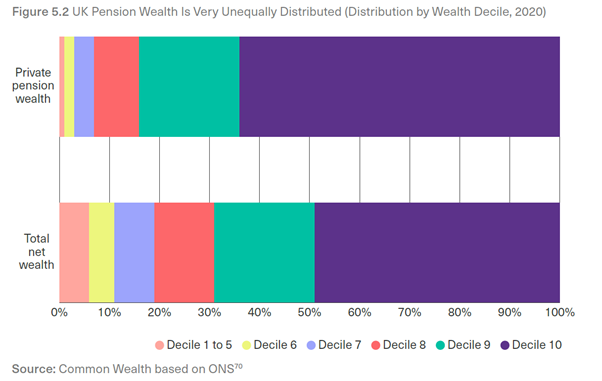

An excellent report came out in August this year from Common Wealth entitled Undefined Benefit: Fixing the UK Pensions System on the problems and potential alternatives for the UK pension system. One of the most eye catching points made in the report was that, despite pension gains since 2010 in terms of average pensions, the overall coverage of pensions remains very patchy and uneven, particularly towards the bottom end. This graph in particular caught my eye:

The bottom half have very little total net wealth and virtually no private pension wealth at all. This makes them almost entirely dependant on the State Pension and any other income-related (in the absence of a full pension) or other benefits they may be entitled to.

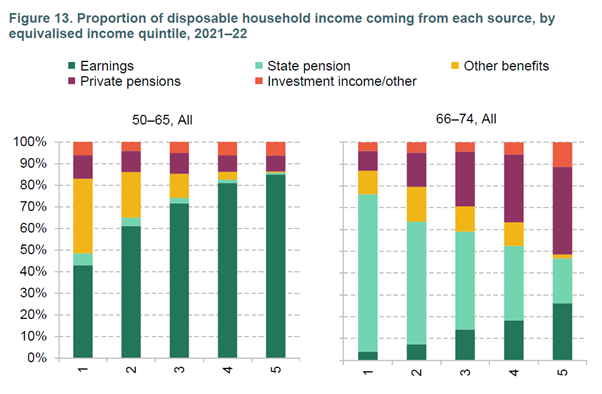

Coincidentally, the IFS have also produced a paper on pensions recently, including this graph (note the cut off at age 74):

The new State Pension (nSP as the Government refer to it) came into effect in April 2016 and currently stands at £203.85 per week or £10,600 pa. This compares with the Pensions and Lifetime Savings Association’s (PLSA) moderate level of retirement living standards which require £23,300 for a single pensioner and £34,000 for a couple. The moderate level includes such things as:

- Some help with maintenance and decorating each year.

- £74 a week on food (including food away from the home).

- 3-year old car replaced every 10 years.

- 2 weeks in Europe and a long weekend in the UK every year.

- Up to £791 for clothing and footwear each year.

- £34 for each birthday present.

The plan for closing the gap between these two levels of income has historically relied on occupational pensions in the UK, to a much greater extent than in most countries. However there are problems with this approach. First of all, not everyone has an occupational pension:

This is the current situation with pensions in payment, which is supposed to be being addressed by automatically enrolling employees into workplace pensions. However, the TUC noted as recently as 2020 that, due to the way the rules operated around low-paid and young workers, 6.3 million employees were still without a workplace pension. A survey of 2,000 employees by Unbiased and Opinium, also in 2020, similarly concluded that 17% of over 55s were still without any pension savings.

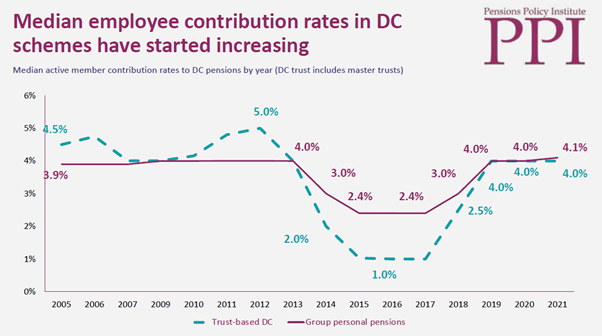

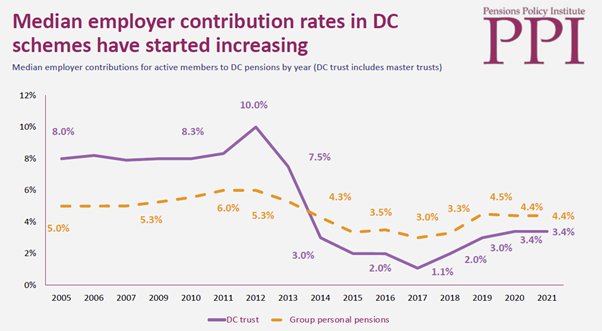

Secondly, as defined benefit occupational pension membership has fallen, the amounts which will be provided by the defined contribution arrangements which have replaced them are comparatively uncertain. The Pensions Policy Institute’s (PPI) DC Future Book 2023 has looked at the average employee and employer contribution rates under auto-enrolment:

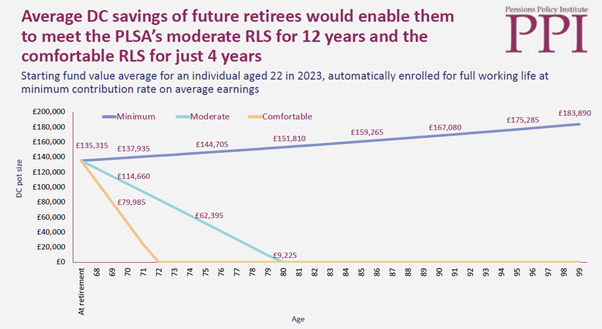

They then projected whether this combined minimum contribution of 8% (on top of the full new State Pension) would be sufficient to meet any of the PLSA’s retirement living standards:

The combination of pension freedoms and not enough in your pot does of course allow crash paths like these, and perhaps explains the slightly more positive pension position shown in the chart from the IFS report compared to the first chart. By cutting off at 74, the IFS could well be surveying people on the steep descents above while they are still depleting their pots to maintain a slightly higher income.

Of course many other models are available – these projections used the PPI economic scenario generator developed by King’s College with many of the economic assumptions taken from the OBR and there are further details at the end of the report – but that seems beside the key point to me here.

Irina Dunn famously daubed the phrase “a woman needs a man like a fish needs a bicycle” on the back of a toilet door in the University of Sydney in 1970. The pension industry has been very successful in attracting funds and innovative in developing products, and occupational pensions coverage overall at some level has clearly increased substantially as a result of auto-enrolment. But none of the bells, gear arrangements, lightweight alloys or any of the other innovations can change the fact that a state-of-the-art defined contribution investment bicycle can never guarantee to float a goldfish to the water level it needs to thrive. You need the state to fill the tank.

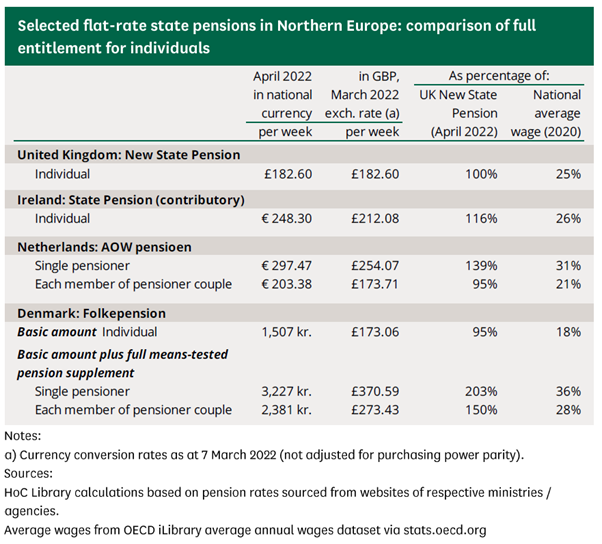

This means raising the State Pension, not by some arbitrary formula involving price inflation, earnings inflation and the number you first thought of, but to what we regard as a reasonable level to live on and which we want to be able to guarantee noone falls below. Comparing the UK with other comparable flat rate state pension pillars in Europe we find the following (from March 2022):

This would suggest an increase of somewhere between 40% and 100% to the current State Pension level to reset the balance between a guaranteed income and that based on the lottery of the markets to European levels.

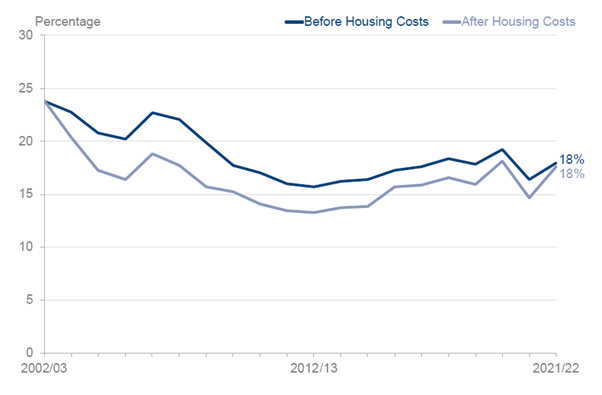

Many people talked about the need to increase societal resilience as we emerged from the pandemic, instead we appear to be moving in the opposite direction, with no clear idea yet about how to deal with NHS waiting lists, even less idea of how to deal with rough sleepers. And on pensioner poverty we have this:

After a concerted attempt to reduce the percentage of pensioners in relative low income during the pandemic, the curve is upwards again, as it has been since at least 2012.

Things have got so bad that Olivier De Schutter, the UN’s special rapporteur on extreme poverty and human rights, has described the UK’s main welfare system as “a leaking bucket” and said that our poverty levels violate international law.

This cannot go on. We can certainly afford to have a welfare system which does not violate international law. And we can afford a much less leaky bucket when it comes to pensions too. I will provide some ideas on how in my next post.

The latest publication from the Institute and Faculty of Actuaries (IFoA) is called Beyond the next Parliament: The case for long-term policymaking. It refers to a number of previous reports, such as the Great Risk Transfer report from April 2021 and the two more recent climate papers (here and here), all of which contained much thoughtful analysis even if I did not always agree with all of the recommendations.

The case for long-term policymaking is certainly something that needs to be made loudly and often, although I was perhaps expecting some discussion of concepts like cathedral thinking, ie a capacity to plan and implement projects over multiple generations, or intergenerational justice, an issue of particular importance when discussing responses to climate change, in tying these various reports together within a long-term narrative. The Good Ancestor by Roman Krzanic is a great starting point for considering such questions.

Instead the IFoA have chosen to go in a different direction entirely in linking this previous work together, displaying imprisonment by current short-term political thinking in a paper supposedly focused on the long-term to such an extent that I am now left feeling that I disagree with them about nearly everything.

Take pensions, for instance (bold type is mine):

With the decline of defined benefit (DB) pension schemes, the responsibility for investment and longevity risk is increasingly being placed on the individual.

In a world where responsibility for funding retirement is increasingly being placed on the individual, there is remarkably little consistent consumer information about how much someone should save into their pension, or what a ‘good’ pension pot constitutes.

The IFoA remains concerned that many UK households are not saving enough for later life, are not accessing free guidance or paid-for financial advice, and remain ill-equipped to deal with the risk of running out of money in retirement.

It is almost as if the transfer of risk to individuals is something inevitable, or beyond the ability of mere humans to control. In the words of the late great John Sullivan, in the theme song from Only Fools and Horses:

Cause where it all comes from is a mystery. It’s like the changing of the seasons and the tides of the sea.

Why Only Fools and Horses you ask? Well have you ever heard a better description of defined contribution pensions than:

No income tax, no VAT. No money back, no guarantee

The IFoA’s main concern is that UK households are not doing enough about this new “responsibility” to provide for their own retirement. And the state? The state pension is mentioned only once here:

Naturally, the next UK Government will need to address the adequacy question as part of a wider pensions strategy for the UK that also considers big questions such as the sustainability of the State Pension and the triple lock.

This of course is so-called “positive economics” in action, which makes much of only relying on objective data analysis, but within a policy framework which is not up for discussion. Increased state provision, which one would have thought would at least need to be considered in the mix in this case, is reduced to obsessive focus on tiny questions like the triple lock while being kept generally outside this policy framework. Instead we get this:

We recommend that the government should reinvigorate its public messaging around minimum pension saving levels – particularly through workplace auto-enrolment pension schemes – to ensure that consumers are not lulled into a false sense of security as to whether their pension saving will be adequate to achieve their retirement income goals.

In doing so, government should use expertise and evidence on testing behavioural responses to different messages and channels, to identify those that are most effective in impacting saving behaviour.

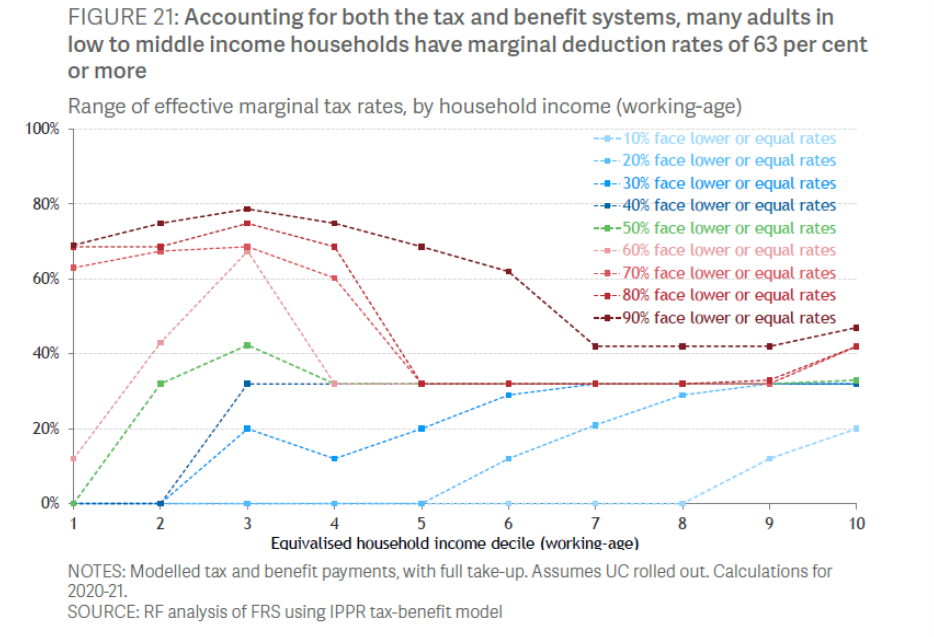

So at a time when, according to the Resolution Foundation, the marginal rate for low to middle income households have an effective marginal rate of tax of 63%, the IFoA apparently think it is acceptable to push the cost onto them even more in order to achieve a sufficient pension at retirement. A certain cost and uncertain benefit. It is not a basis for a minimum income guarantee.

The second section sets out the problems associated with long-term care, again asking for a greater contribution by individuals via an expansion of insurance and savings-based financial products.

We are back to the changing of the seasons and the tides of the sea in the next section on keeping pace with rapid digital transformation, which states that:

there has been a trend away from broad risk pools and toward more granular pricing based on an individual’s specific rating factors (i.e. their risk characteristics)

Note the use of the passive tense there – it implies that noone is responsible and there is no way we can swim against this current back up to those old broad risk pools however hard we try. And so we shouldn’t try. The only option is to instead try and lower the premiums at the bottom end a bit – which is explained in their other report, The hidden risks of being poor: the poverty premium in insurance. The model for this is Flood Re, which is explained here. Of course this probably won’t work if you are underinsured as, it seems, 80% of us are.

Section 3 remains one I can cheer about, laying out more clearly than I have seen before to the financial community the risks of climate change, with the work on biodiversity at a somewhat earlier stage. However a framework is immediately assembled in the next section, Going for growth to build a better Britain (a slogan which I am sure Liz Truss would have been quite happy with), to limit the options for tackling these risks. An example:

Even though there is evidence that infrastructure development can promote growth and job creation, governments may be forced to defer such funding until the national balance sheet looks healthier. Although governments may be partially able to finance infrastructure projects, given their capital constraints they also need to attract investment from the private sector.

Unbelievably, the rest of this section then focuses almost entirely on what can be done to lure the private sector into investing in preventing their own doom (not framed in those terms of course, but in terms of boosting growth rather than curbing emissions) along with everybody else’s. As long as private investors are looked after, everything else seems to be a secondary consideration. John Sullivan again:

C’est magnifique, Hooky Street.

Of course I am just having a bit of fun here with the Only Fools and Horses references and I am certainly not suggesting that everyone involved in financial markets is a Del Boy looking to take advantage of every punter or government that comes their way. That would be a caricature as gross as referring to the “dead hand of the state” or talking about public servants as “The Blob”. What I am saying is that the jostle of the market place cannot be the primary solution to many of the problems so accurately analysed here.

I realise I have been very slow to fully appreciate the IFoA’s general direction of travel, but by putting all of these reports together in one place they have clarified this for me. I believe that the overall programme of recommendations here would condemn the poor to further immiseration and uncertainty while letting government largely off the hook for solutions and companies largely off the hook in terms of further regulation. It would further accelerate the financialisation of our economy with the promise of additional financial markets to be exploited by the already wealthy.

This is not acting in the public interest but as a cheerleader for protecting the long-term profits of fund managers. And I despair that, three years on from the IFoA’s Economics Member Interest Group coming into existence, there should still be so little pluralism on display here in economic thinking that this is regarded as a balanced narrative.

It is clear to me that views outside the IFoA’s current policy framework will need to come from elsewhere. I am currently researching a paper on alternative approaches to pensions provision with Alan Swallow which I hope we will be able to publish something about soon.