I wanted to share this lovely account of Vonnegut’s story shapes because it is one very powerful way to categorise different outcomes and, as such, potentially a very interesting way of illustrating them and their implications. I feel sure I will be returning to this theme soon.

The Treasury is consulting on the tax relief that should be available in future for pension schemes and their members. The principles for any reform that it has set out are:

- it should be simple and transparent;

- it should allow individuals to take personal responsibility;

- it should build on the success of automatic enrolment; and

- it should be sustainable.

Simplicity, transparency, personal responsibility and sustainability mean different things to different people, which means that the precise meaning of these principles will depend on the politics of the people proposing them. However the words themselves are difficult to argue with, which is presumably why they have been chosen.

It has then set out 8 questions that it would like answered in response to its consultation. The consultation ends on 30 September. I have set out my responses below. I hope that they will sufficiently incense one or two more people into making their views heard, before the chance disappears.

1. To what extent does the complexity of the current system undermine the incentive for individuals to save into a pension?

On this question I think I agree with Henry Tapper at the Pension PlayPen. He says the following:

In summary, millions of pounds of tax relief is wasted by the Treasury helping wealthy people avoid tax…Incentives are available to those on low earnings who pay no tax, but this message is not getting through, we need a system that resonates with all workers, not just those with the means to take tax advice.

I then think I agree with the following:

The incentive should be linked to the payment of contributions and not be dependent on the tax or NI status of the contributor – if people are in – they get incentivised.

That would certainly make the incentive to the pension scheme member clearer and potentially easier to understand. The other simplification I would support would be the merging of income tax and national insurance contributions – many of the sources I have referenced below are trying to solve problems caused by the different ways these two taxes are collected. This simplification would be an essential part of any pension reforms in my view.

2. Do respondents believe that a simpler system is likely to result in greater engagement with pension saving? If so, how could the system be simplified to strengthen the incentive for individuals to save into a pension?

This is the invitation to support TEE (ie taxed-taxed-exempt, the same tax treatment as for ISAs). I have up until now been persuaded by Andrew Dilnot and Paul Johnson’s paper from over 20 years ago that this was not a good idea. This pointed out that the current EET system:

- Avoids problems with working out what level of contributions are attributable to individuals in a DB system

- Does not discourage consumption in the future relative to consumption now

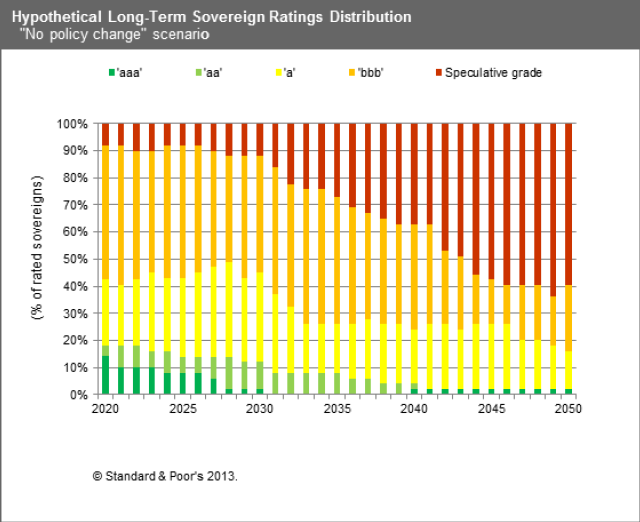

I have changed my mind. The first point has already been addressed in order to assess people against the annual allowance, although this may need to be further refined. The second point is more interesting. As Paul Mason has pointed out in Postcapitalism, the OECD 2010 report on policy challenges, coupled with S&P’s report from the same year on the global economic impacts of ageing populations point to the scenario pensions actuaries tend to refer to when challenged on the safety of Government bonds, ie if they fail then the least of your problems will be your pension scheme. The projections from S&P (see bar chart above) are that 60% of government bonds across all countries will have a credit rating below what is currently called investment grade – in other words they will be junk bonds. In this scenario private defined benefit schemes become meaningless and the returns from defined contribution schemes very uncertain indeed. A taxation system which seeks to extract tax on the way in rather than on the way out then looks increasingly sensible.

I think that both the popularity of ISAs and the consistently high take up of the tax free cash option by pensioners, however poor the conversion terms are in terms of pension given up, suggest that tax exemptions on the way out rather than on the way in would be massively popular.

3 Would an alternative system allow individuals to take greater personal responsibility for saving an adequate amount for retirement, particularly in the context of the shift to defined contribution pensions?

Based on my comments above, I think the whole idea of personal responsibility for saving adding up to more than a hill of beans for people currently in their 20s may be illusory. People do take responsibility for things they can have some control over. Pension savings in the late twenty-first century are unlikely to be in that category.

4 Would an alternative system allow individuals to plan better for how they use their savings in retirement?

As I have said I favour a TEE system like ISAs. I think some form of incentive will be required to replace tax exemption, such as “for every two pounds you put in a pension, the Government will put in one” with tight upper limits. The previous pensions minister Steve Webb appears to broadly support this idea. Exemption from tax on the way out (including abolition of the tax charges for exceeding the Lifetime Allowance) would also aid planning.

5 Should the government consider differential treatment for defined benefit and defined contribution pensions? If so, how should each be treated?

I think this is inevitable due to the fact that defined contribution (DC) schemes receive cash whereas defined benefit (DB) schemes accrue promises with often a fairly indirect link to the contributions paid in a given year. In my view taxation will need to be based on the current Annual Allowance methodology, perhaps refined as suggested by David Robbins and Dave Roberts at Towers Watson. The problem with just taxing contributions in DB is that you end up taxing deficit contributions which would effectively amount to retrospective taxation.

A further option discussed in Robbins and Roberts is making all contributions into DB schemes into employee contributions. I would go further and apply this to both DC and DB schemes – a sort of “reverse salary sacrifice” which could be encouraged by making the incentives on contributions only available on employee contributions, which would then be paid out of net pay. Any remaining accrual contributions made by employers in a DB scheme would be taxed by an adjustment to the following year’s tax code.

6 What administrative barriers exist to reforming the system of pensions tax, particularly in the context of automatic enrolment? How could these best be overcome?

I think everything points to the need for the retirement of DB for all but the very largest schemes. It would be better to do this gradually starting soon through an accelerated Pension Protection Fund (PPF) process rather than having it forced upon us in a hurry later in the century when PPF deficits may well be considerably higher than the current £292.1 billion.

7 How should employer pension contributions be treated under any reform of pensions tax relief?

As I have said, I think they should be converted into employee contributions based on higher employee salaries. This would make it clearer to people how much was being invested on their behalf into pension schemes.

8 How can the government make sure that any reform of pensions tax relief is sustainable for the future.

They can’t, and any change now will almost certainly be revisited several times over the next 50 years. However, systems where people feel they can see what is going on and which are tax free at the end are currently very popular and I would expect them to remain so for the foreseeable future. That takes care of political sustainability in the short term. What about longer-term economic sustainability? Faced by an uncertain and turbulent next 50 years where I have argued that personal responsibility (rather than communal responsibility) for pensions will seem increasingly irrelevant, I think what I have proposed will allow us to transition to a system which can be sustained to a greater degree.

We are entering what may prove to be a traumatic time for the world economy if Postcapitalism is even half right. Pensions taxation seems a good place to try and start to move our financial institutions in a more sustainable direction.

Nick Foster is a former pensions actuary who now lectures at the University of Leicester

I ask this question because:

- I have just read The Spirit Level by Richard Wilkinson and Kate Pickett, and am convinced by their arguments and evidence that inequality lies at the root of most of the social problems we have in the UK; and

- As a scheme actuary, I persuaded myself that I was facilitating a common good, namely the provision of good pensions to people who might not otherwise have them to as high a level and for as long as possible given the economic conditions of the sponsors. The introduction of the Pension Protection Fund reduced the importance of the scheme actuary role, by mitigating the impact of sponsors not meeting their obligations, but still left a job I felt was worth doing. However, it now seems to me that, if pensions are not tackling inequality or even exacerbating it, they might be doing more harm than good.

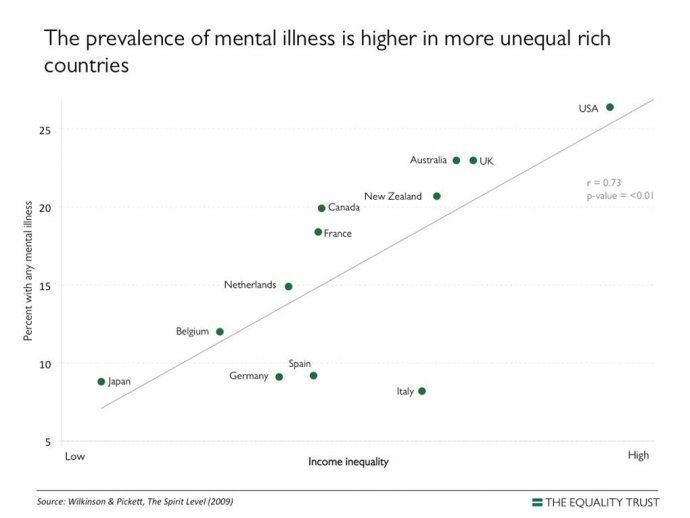

First of all, I strongly recommend the Equality Trust website, which has a number of graphs showing the links between inequality and various social ills. One example, showing the relationship between inequality and mental illness, is set out below.

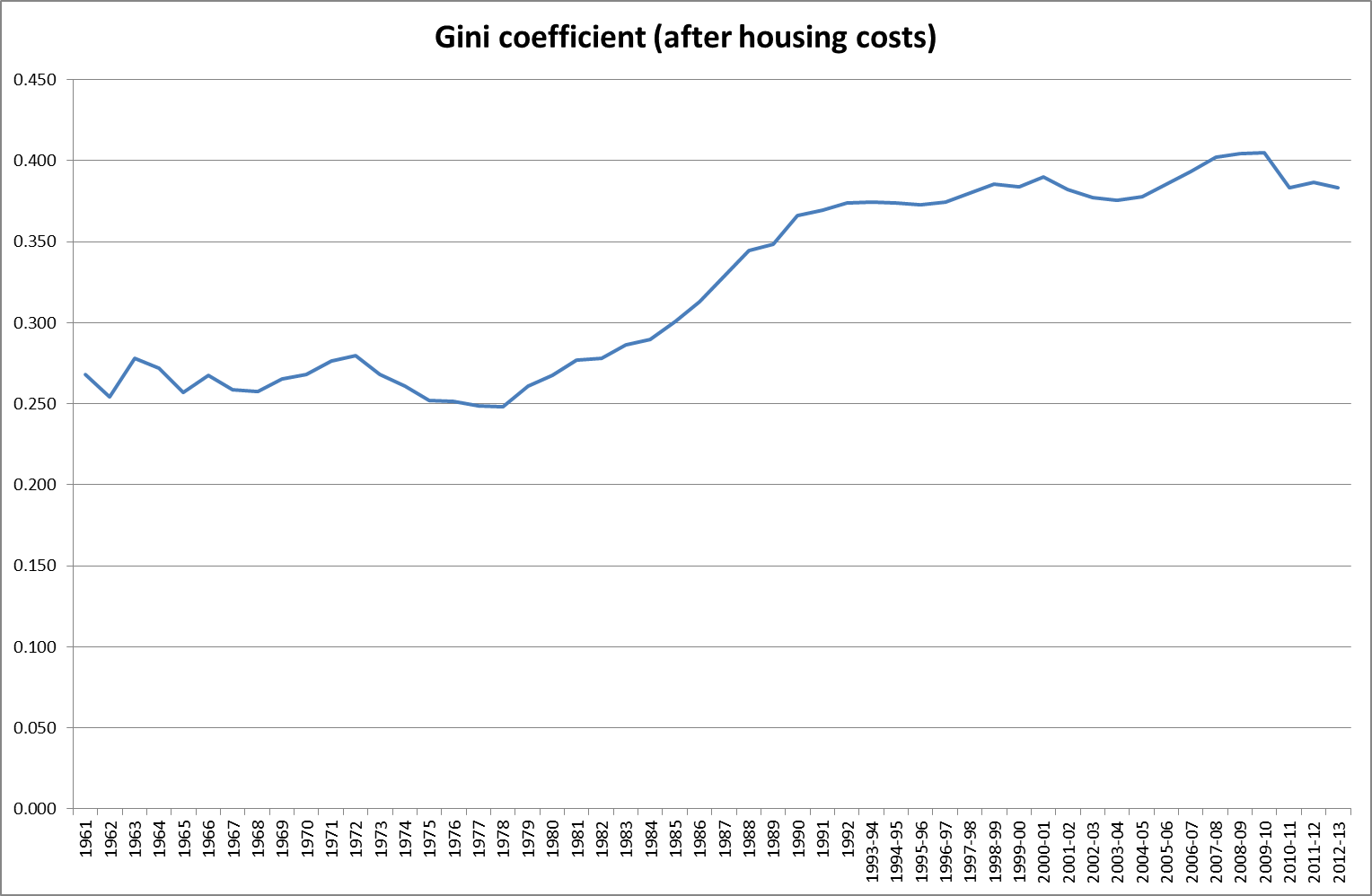

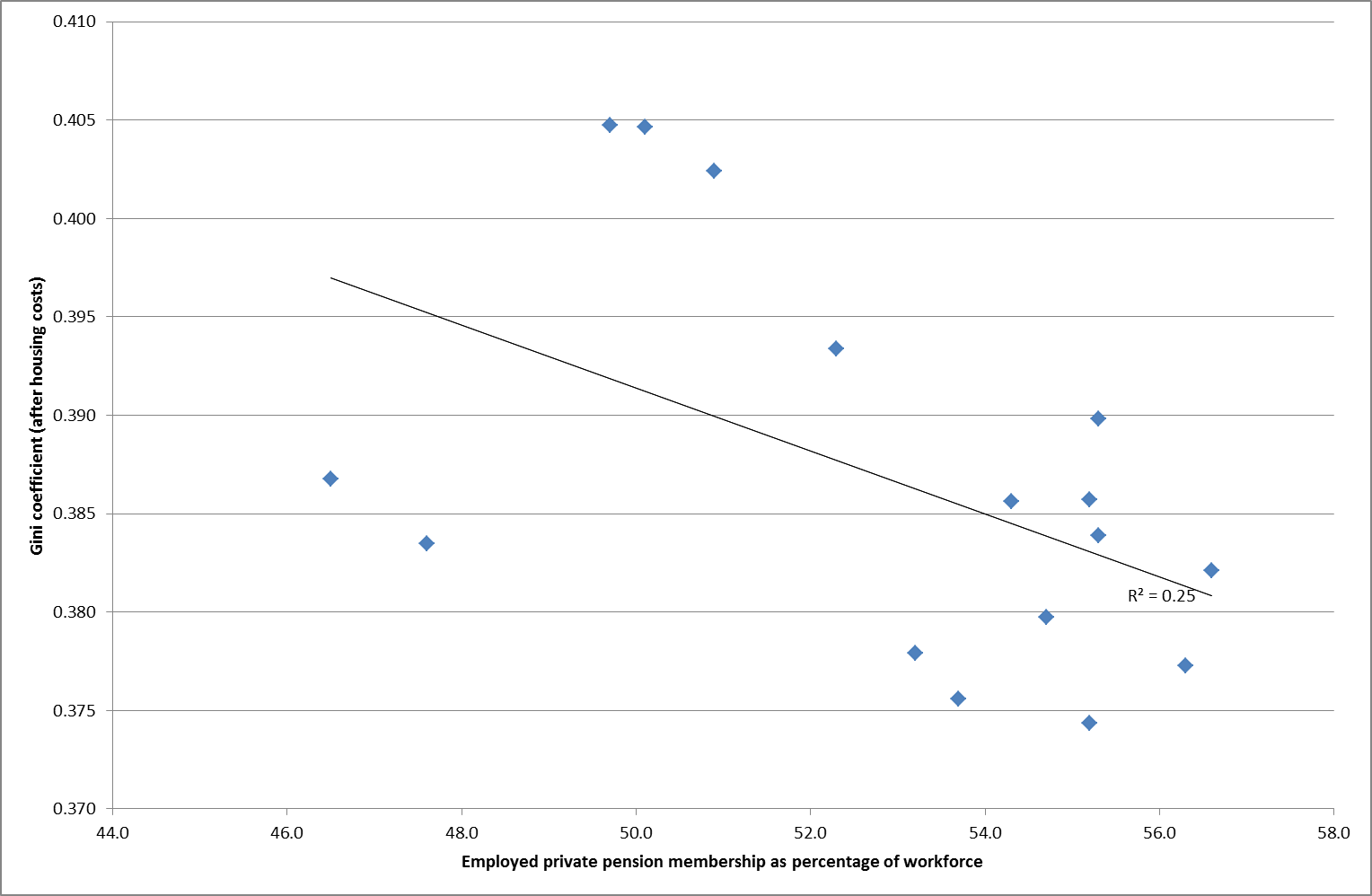

So what is the evidence on inequality and pensions? Certainly inequality, as measured by the Gini coefficient, in this case after a reduction for housing costs, has increased markedly in the UK since the 1960s.

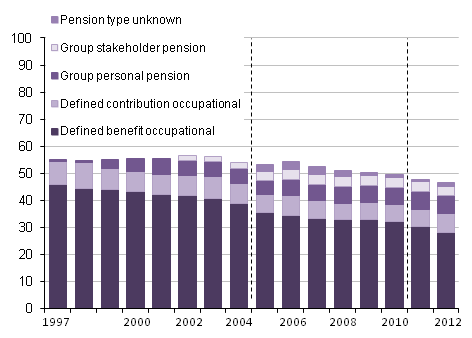

While the proportion of private pension provision since 1997 as a percentage of the workforce has fallen (courtesy of the Office for National Statistics).

But is there much of a correlation between them? Well there is a weak negative correlation between the Gini coefficient and the percentage in workplace pensions as a whole.

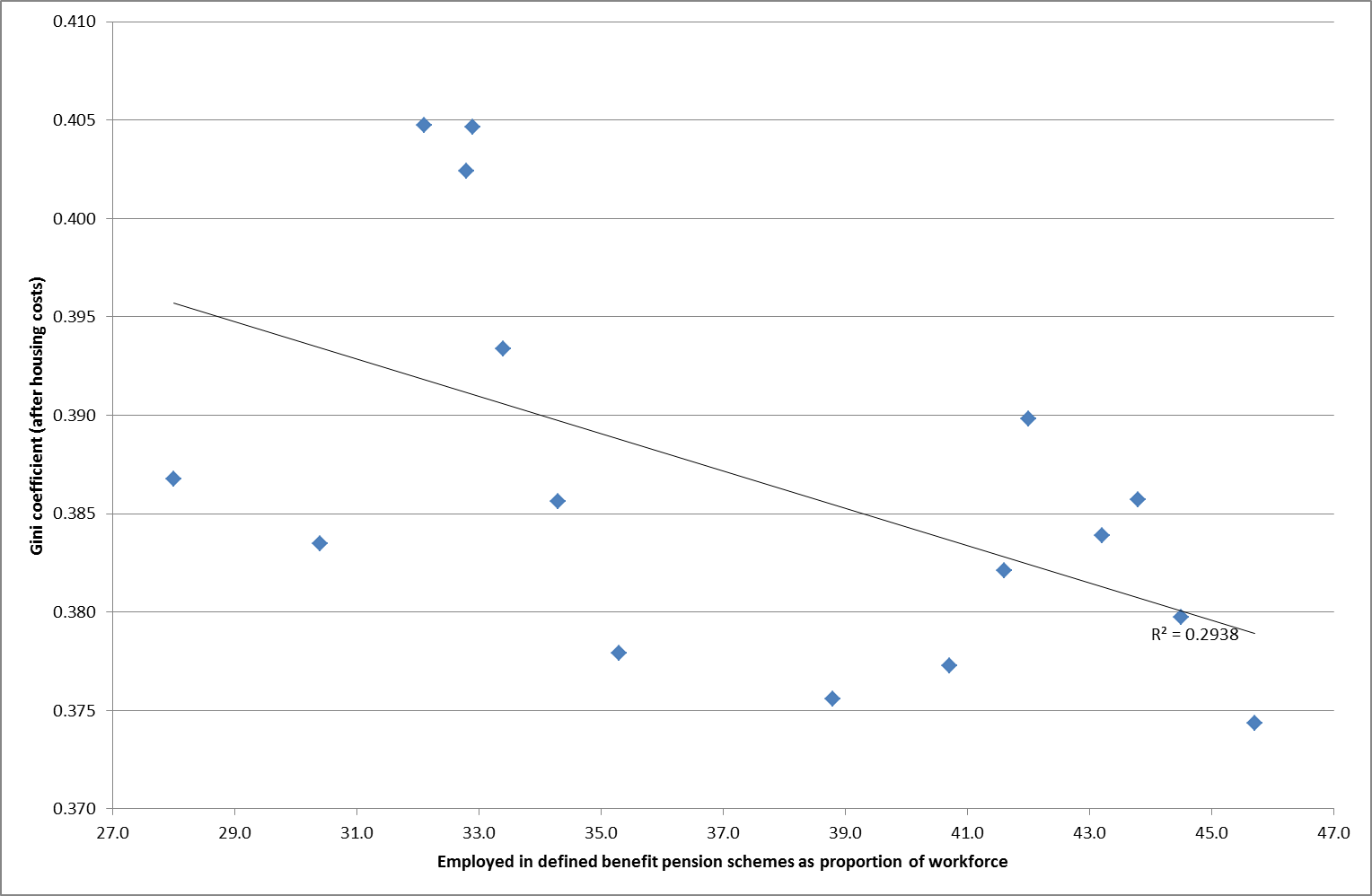

And a rather stronger one when we just look at defined benefit (DB) pension scheme membership.

Neither of these are particularly strong correlations. Any impact by workplace pensions on inequality is likely to be limited of course, because they are in general structured (via final salary formulae in the case of DB, and employer and employee contributions as a percentage of salary in the case of defined contribution (DC)) to preserve relative incomes in retirement, even if not absolute differentials. However, moving now to the OECD statistics website, we can look at the retirement age community as a whole and compare their relative inequality with that of the working age population.

Turning to the working age population first, we can see below that the UK is a very unequal society compared to a range of rich countries, although less so than the US.

data extracted on 15 Aug 2014 15:52 UTC (GMT) from OECD.Stat

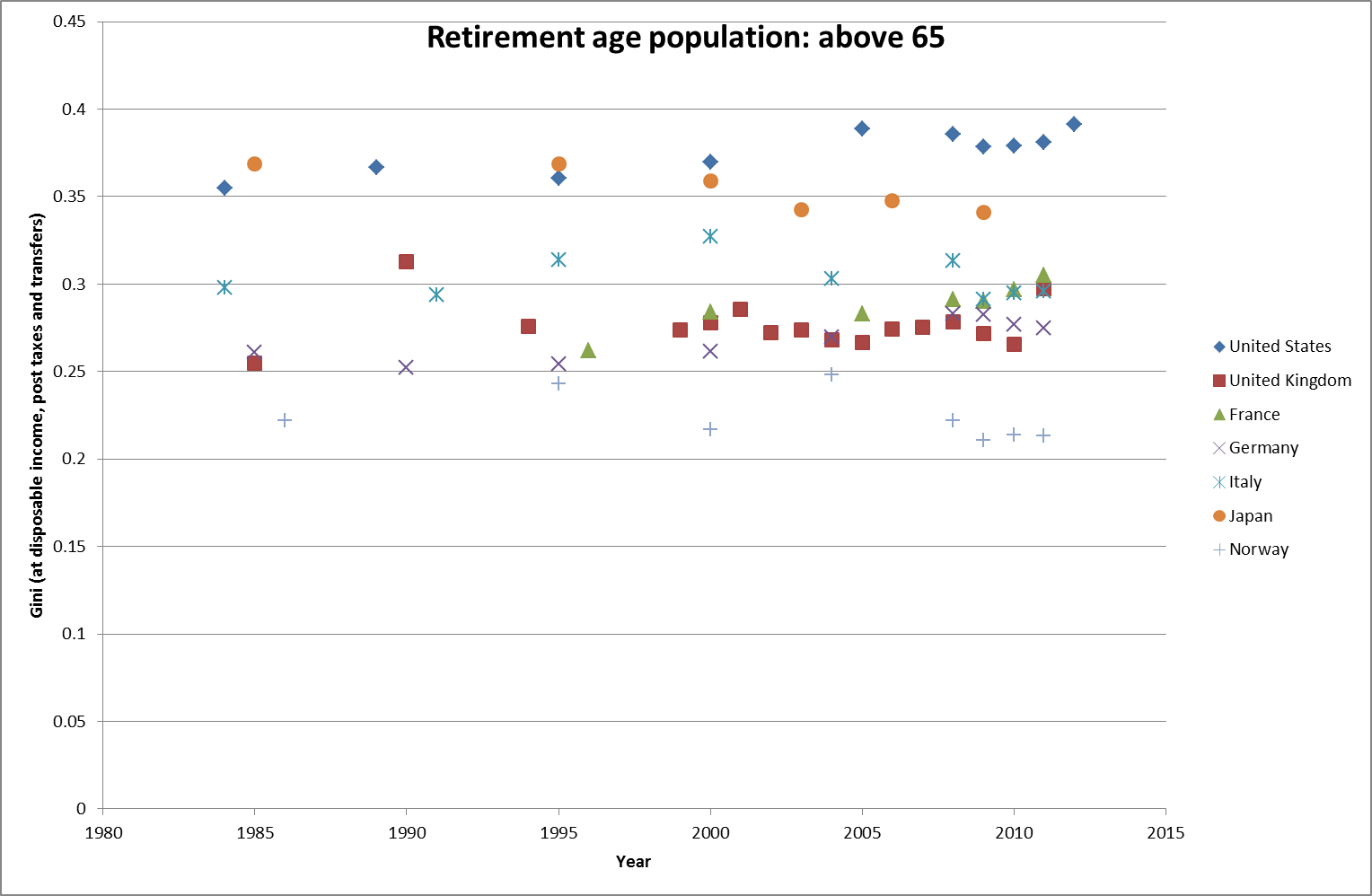

On the other hand, we get a very different picture if we consider the UK’s over 65 population, where the level of inequality is well below that of the US, and broadly comparable with the other major EU states.

data extracted on 15 Aug 2014 15:52 UTC (GMT) from OECD.Stat

Clearly this is not primarily down to private pension provision, but the more redistributive state pension and other benefits. However, at least the weak correlations we saw previously suggest that private pensions have not made inequality any worse and possibly slightly mitigated against it.

I think we can do better than this: after all we had inequality levels equivalent to current Norwegian levels back in the early 60s (which is why I included them in the international comparisons above). So the news that pensions tax relief is likely to be provided at a 30% rate for all after the election rather than reflecting the current tax bands is not, in my view, the cause for gnashing of teeth as the Telegraph and others believe but actually a good thing. After all, the Pensions Policy Institute have shown that 2/3rds of all tax relief is going to those earning over £45,000 pa.

One of the clear conclusions of the research carried out in The Spirit Level and elsewhere is that reducing inequality in society benefits every group in it, including those who are redistributed away from. Pension provision has its part to play in this.

And 30% tax relief does not seem like too high a price to me.

The response to the consultation on the Budget pension proposals has much to welcome in it. The Government appears to have listened to the arguments that their concerns about the impact on financial markets of the reforms bordered on paranoia, and have agreed to continue allowing private sector defined benefit schemes and funded public sector schemes to process transfers. They have committed to continuing to consult on the idea of extending the new freedoms to defined benefit schemes themselves, which would avoid the need for a lot of expensive fee-generating transfers into defined contribution arrangements.

And yet. The section on the guaranteed guidance suggests that, despite the opinions expressed in the consultation, the Government is still primarily focused on guidance “at the point of retirement” despite the probability that this is likely to become just one of the criticial retirement phases following these reforms. And the reform of pensions legislation seems overly concentrated on facilitating innovations in annuities rather than allowing the level legislative playing field between different forms of pension provision that would be required to prevent the death of defined ambition.

But the real problem I have with the consultation response concerns the minimum pension age. A point i have made before. Currently 55, the Government has decided to increase this to 57 by 2028. I think this is a mistake. Why promote freedom in the form you take your benefits but not when you take your benefits?

And the need for this freedom is evident. The latest Office of National Statistics (ONS) release on healthy life expectancy at birth by local authority suggests that, in many areas, this may condemn people to work until they are sick.

Here is the graph for males in local authorities where the healthy life expectancy (HLE) is less than the state pension age (SPA):

And the equivalent graph for females:

For each local authority area you need the red line to be above the minimum pension age to be 95% sure the average member of its population is able to retire, even if only partially, in good health. For the males, Blackburn, Blackpool, Islington and Tower Hamlets already have red lines below a minimum pension age of 55. Increase this to 57 and the number of red lines below multiplies alarmingly. And this is just an average – many will have life expectancies well below this.

Of course we assume life expectancy will increase between now and 2028, but healthy life expectancy? One of the problems is that it has not been measured for very long, and there have been disagreements about how it should be measured. As the King’s Fund shows, in 2005 a change to the methodology caused healthy life expectancy to plunge by 3 years, suggesting a rather optimistic approach previously. The ONS methodology is set out here.

It seems clear to me that there is sufficient doubt around how long people around the UK are expected to remain in good health for the Government to pause before raising the minimum pension age. After all we already know how those in ill health are likely to be treated if they try to claim they can’t work.

A flower for every person that died within 6 weeks of ATOS finding them fit for work

At times it all sounds like the joke about the visitor to Hell being shown by their PR department how the bad press had been much exaggerated. There were concerts on Wednesday afternoons and coffee mornings on Fridays, the manure was only ankle deep in many places and the eternal flames were optional. However, on accepting his place for eternal damnation, another senior devil he had never seen before walked in to announce “Ok, tea break’s over. Back on your heads!”

It would seem that tea break is over.

As Rowan Atkinson once said: “Life is one of those things that most of us find very difficult to avoid”. You would imagine that death would be similarly unavoidable, but not in all cases it would seem.

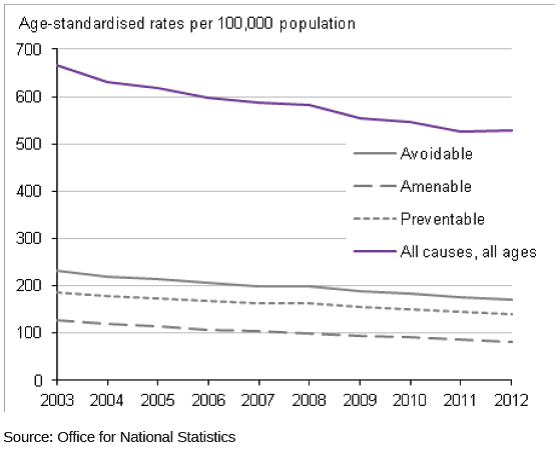

The Office of National Statistics (ONS) have just issued the latest figures (for 2012) on what they define as avoidable deaths (“mortality figures for causes of death that are considered avoidable in the presence of timely and effective healthcare or public health interventions”) and have concluded that these account for a staggering 23% of all deaths.

Avoidable deaths defined in this way can be further broken down into preventable deaths (ie those that can be avoided mostly or completely through public health interventions, eg traffic accidents) and amenable deaths (ie those that can be avoided mostly or completely through good quality healthcare, eg epilepsy). Some, eg ischaemic heart disease (22% of avoidable deaths in men), are seen as both.

Avoidable deaths defined in this way can be further broken down into preventable deaths (ie those that can be avoided mostly or completely through public health interventions, eg traffic accidents) and amenable deaths (ie those that can be avoided mostly or completely through good quality healthcare, eg epilepsy). Some, eg ischaemic heart disease (22% of avoidable deaths in men), are seen as both.

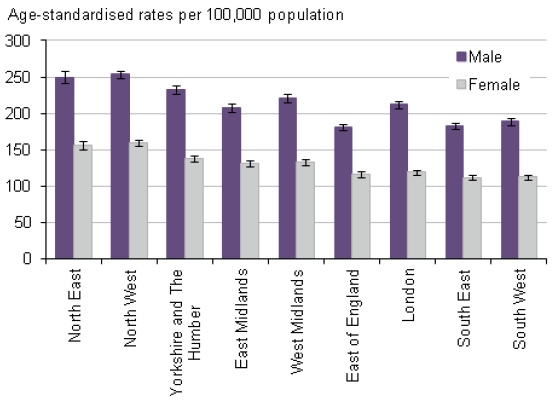

One interesting aspect of this release is the regional breakdown of avoidable deaths as a percentage. These vary from 15% in the South (outside London) to 20% in the North West for women and from 24% in the South West to 31% in London and the North for men.

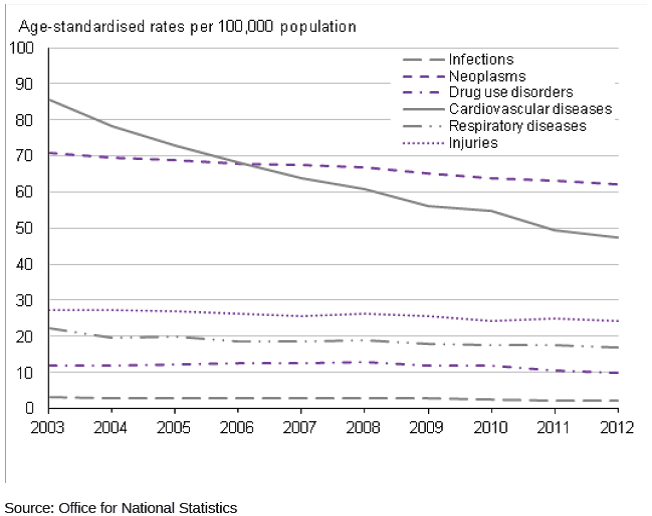

As we can see from the following graph, it is possible for the proportion of deaths by cause to change quite dramatically over time. Could this also be true for avoidable deaths by region?

The methodology for calculating the impact of improved survival rates of various conditions in terms of the number of deaths avoided is “age-standardised”, which means that we are all living in a population with the same structure as an average European population from 1976, when ABBA were in their pomp. The actual potential proportion of lives saved may therefore be more or less than 23%. This also means that some of the differences between regions could be due to how different their population structures are to ABBAland, eg there are a lot more over 65s as a proportion of the 2013 Standard Population (which the ONS should be moving to using soon) than there are in the 1976 version.

However, as David Spiegelhalter shows here, it is relatively straightforward to convert an improvement or deterioration in mortality rates into an increase or decrease in life expectancy. Making a few heroic assumptions (in this case: 1. that the most popular mortality table currently used by occupational pension schemes, but without any mortality improvements since 2002/03, is an appropriate way to estimate the effect of removing avoidable mortality on life expectancy; and 2. that the mortality is avoided equally at all ages from 65 onwards) we can therefore estimate the 7% difference for men and 5% difference for women in the degree of avoidable mortality to be equivalent to around 0.6 years for men and 0.4 years for women in the life expectancy at age 65.

If the mortality rates could therefore be improved in regions with currently the highest proportions of avoidable mortality, so that the avoidable mortality remaining was no higher than in those regions where it is currently at the lowest proportions, life expectancy at 65 would be increased in some regions by up to 0.6 years.

However, averaging by region smooths out much larger differences between postcodes (postcode mortality mapping is commonly used, eg by insurance companies in setting annuity rates). For instance, the current gap between the highest and lowest life expectancy at age 65 is 6 years for men (between Harrow and Glasgow City) and 5.5 years for women (between Camden and Glasgow City). So perhaps we should be shooting for the rather higher ambition of removing all of the avoidable mortality. If the overall average avoidable mortality of 23% could actually be avoided, this would lead to an average increase in life expectancy at age 65 of 2 years.

Finally, what about the differences between men and women? The ONS report states than “Men are more likely to die from potentially avoidable causes than women, with about 28% (67,548 out of 240,238) dying from avoidable conditions compared with 17% (44,945 out of 259,093) of women in 2012.” That 11% difference would equate to a life expectancy difference at 65 of around 1 year, which is about half of the current gap between men and women at 65. Women living longer than men? It would seem that it’s only half inevitable.

Sometimes the best explanations of things come when we are trying to explain them to outsiders, people not expected to understand our particular forest of acronyms, slangs and conventions which, while allowing speedier communication, can also channel thinking down the same tired old tracks time after time. Such an example I think is the UK Government Actuary’s Department (GAD) paper on Pensions for Public Service Employees in the UK, presented to the International Congress of Actuaries last month in Washington.

Not a lay audience admittedly, but one sufficiently removed from the UK for the paper’s writers to need to represent the bewildering complexity of UK public sector pension provision very clearly and concisely. The result is the best summary of the current position and the planned reforms that I have seen so far, and I would strongly recommend it to anyone interested in public sector pensions.

There are two points which struck me particularly about the summary of the reforms, designed to bring expenditure on public service pensions down from 2.1% of GDP in 2011-12 to 1.3% by 2061-62.

The first came while looking at the excellent summary of the factors contributing to the decline of private sector pension provision. Leaving aside the more general points about costs and risks, and those thought applicable to the (mainly) unfunded public service schemes which have been largely addressed by the planned reforms, I noticed two of the factors thought specific to funded defined benefits (DB) plans:

- A more onerous burden on trustees of plans, including member representation, and knowledge and understanding; and

- Company pension accounting rules requiring liabilities to be measured based on corporate bond yields.

As the GAD paper makes clear, the Public Service Pensions Act will result in a significant increase in interventions on governance in particular in some public sector schemes. The Pensions Regulator’s recent consultation on regulating public service pension schemes is also proposing a 60 page code of practice be adopted in respect of the governance and administration of these schemes. This looks like the “onerous burden” which has been visited on the private sector over the last 20 years all over again.

The other point is not directly comparable, as company pension accounting rules do not apply to the public sector. However, as pointed out by the Office for National Statistics (ONS) this week, supplementary tables to the National Accounts calculating public sector pensions liabilities will be required of all EU member states from September this year onwards, to comply with the European System of Accounts (ESA) 2010. These are carried out using best estimate assumptions (ie without margins for prudence) and a discount rate based on a long term estimate of GDP growth (as compared to the AA corporate bond yield required by accounting rules).

The ONS released the first such tables published by any EU member state, for 2010, in March 2012. This for the first time values the liabilities in respect of unfunded public sector pension entitlements, at £852 billion, down from £915 billion at the start of the year.

I think there is a real possibility that publication of this information, as it has for DB pension schemes, will result in pressure to reduce these liabilities where possible. An example would be one I mentioned in a previous post, where mass transfers to defined contribution (DC) arrangements from public sector schemes following the 2014 Budget have effectively been ruled out because of their potential impact on public finances. If such transfers reduced the liability figure under ESA 2010 (which they almost certainly would) the Government attitude to such transfers might be different in the future.

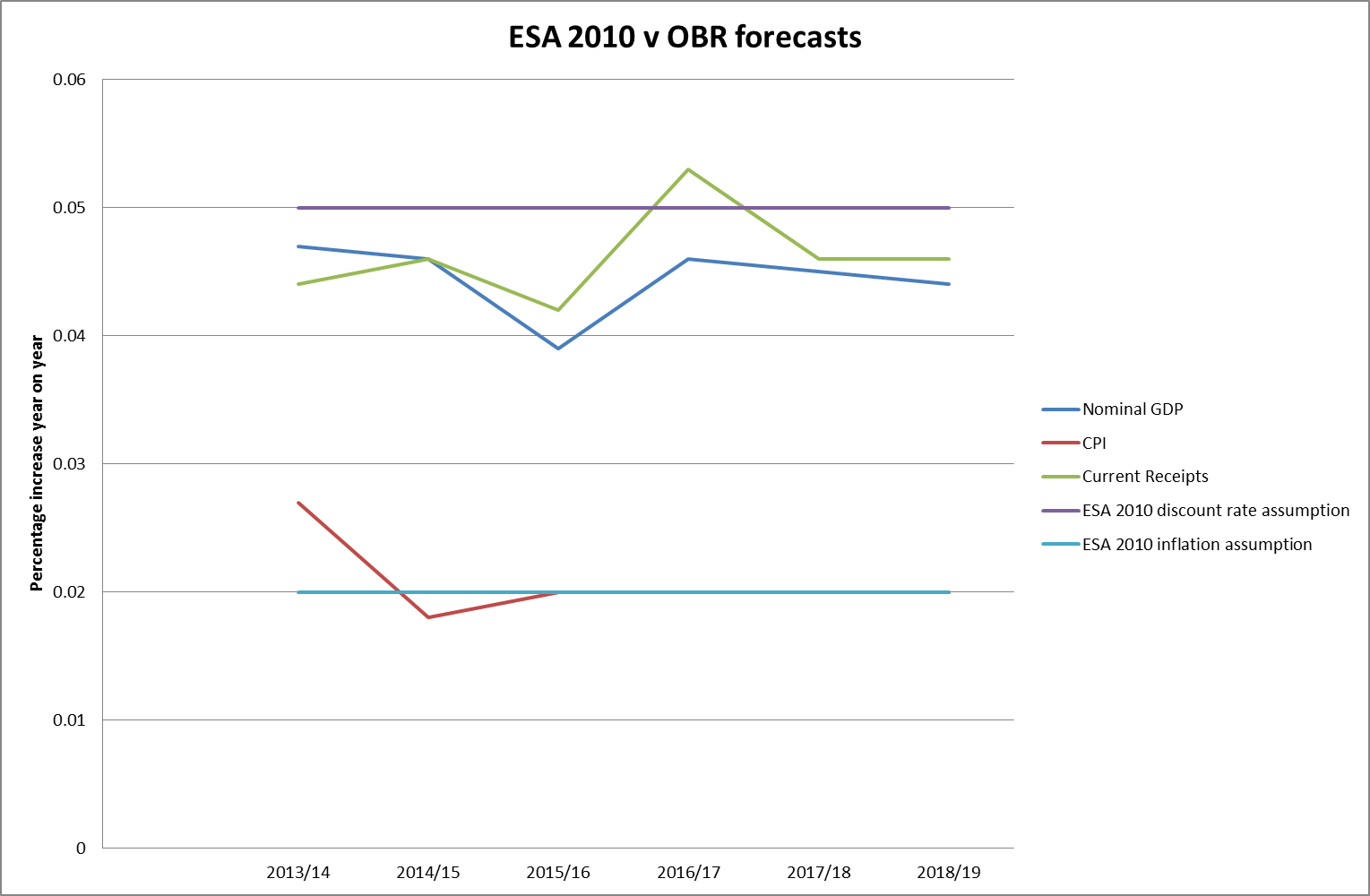

The second point concerned the ESA 2010 assumptions themselves. There was a previous consultation on the best discount rate used for these valuations, ie the percentage by which a payment required in one year’s time is more affordable than one required now, with GDP growth coming out as the preferred option. Leaving aside the many criticisms of GDP as an economic measure, one option which was not considered apparently was the growth in current Government receipts, although this would seem in many ways to be a better guide to the element of economic growth relevant to the affordability of public sector provision. Taking the Office for Budget Responsibility (OBR) forecasts from 2013-14 to 2018-19 with the fixed ESA 2010 assumptions for discount rate and inflation of 5% pa and 2% pa respectively gives us an interesting comparison.

The CPI assumption appears to be fairly much in line with forecasts, but the average nominal GDP and current receipt year on year increase over the next 6 years of forecasts are 4.47% pa and 4.61% pa (4.72% pa if National Accounts taxes are used rather than all current receipts) respectively. A 0.5% reduction in the discount rate to 4.5% pa would be expected to increase the liability by over 10%.

The CPI assumption appears to be fairly much in line with forecasts, but the average nominal GDP and current receipt year on year increase over the next 6 years of forecasts are 4.47% pa and 4.61% pa (4.72% pa if National Accounts taxes are used rather than all current receipts) respectively. A 0.5% reduction in the discount rate to 4.5% pa would be expected to increase the liability by over 10%.

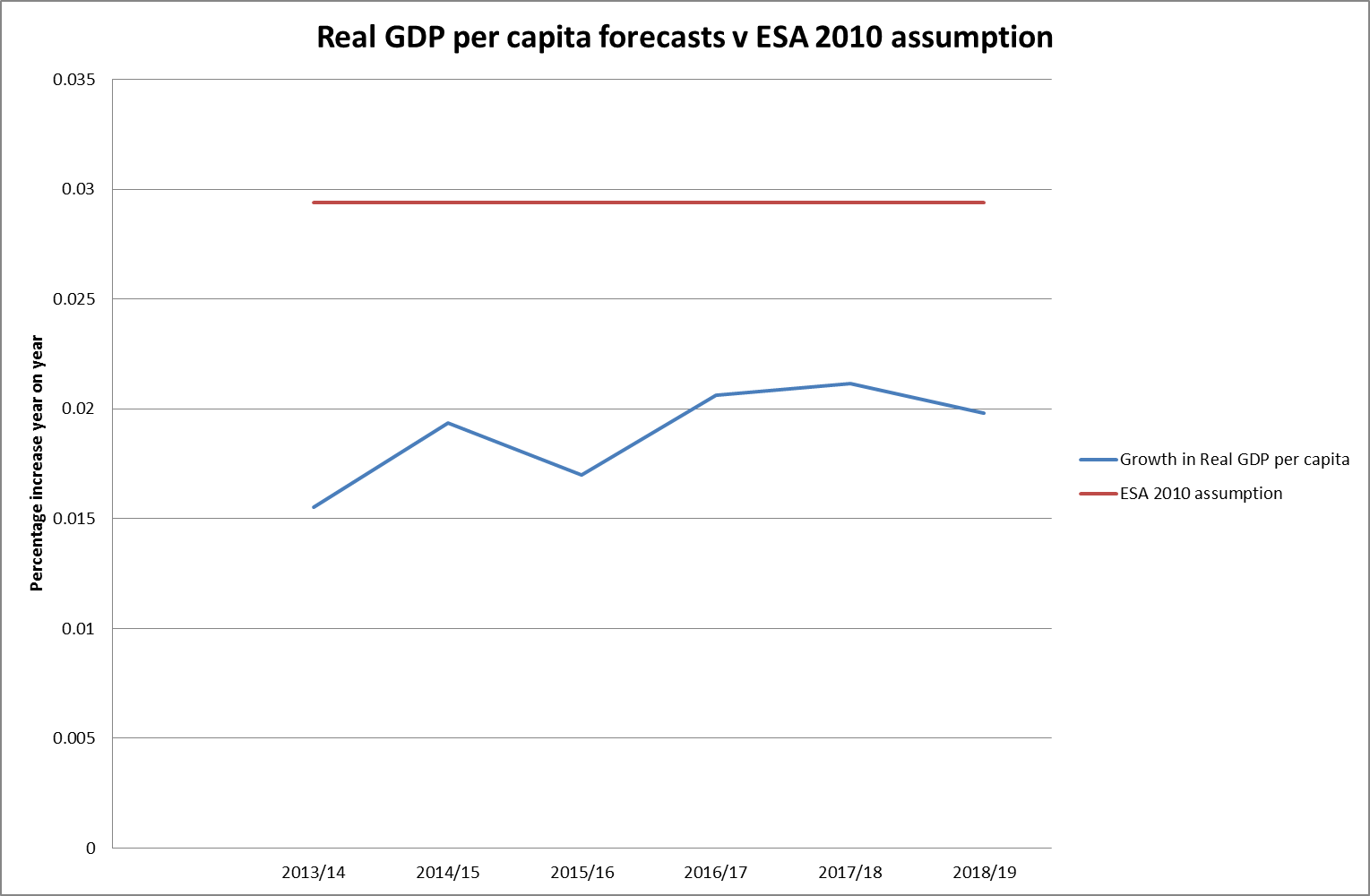

Another, possibly purer, measure of economic growth, removing as it does the distortions caused by net migration, would be the growth of GDP per capita. If we take the OBR forecasts for real GDP growth per capita and set it against the long term ESA 2010 assumption of 1.05/1.02 – 1 = 2.94% the comparison is even more interesting:

In this case the ESA assumption is around 1% pa greater than the forecasts would suggest, making the liability less than 80% of where it would be using the average forecast value.

In this case the ESA assumption is around 1% pa greater than the forecasts would suggest, making the liability less than 80% of where it would be using the average forecast value.

The ESA 2010 assumptions are intended to be fixed so that figures for different years can easily be compared. It would clearly be easy to argue for tougher assumptions from the OBR forecasts (although the accuracy of these has of course not got a great track record), but perhaps more difficult to find an argument for relaxing them further.

Whether the consensus holds over keeping them fixed when and if the liability figures start to get more prominence and a lower liability becomes an important economic target for some of the larger EU member states remains to be seen. However if the assumptions cannot be changed, since public sector benefits now have a 25 year guarantee in the UK (other than the normal pension age now equal to the state pension age being subject to review every 5 years), then the cost cap mechanism (ie higher member contributions) becomes the only available safety valve. So we can perhaps expect nurses’ and teachers’ pension contributions to become the battleground when public sector pension affordability becomes a hot political issue once more.

We can poke fun at the Government’s enthusiasm to take on the Royal Mail Pension Plan and its focus on annual cashflows which made it look beneficial for their finances over the short term, but we may also look back wistfully to the days before public sector pensions stopped being viewed as a necessary expense of delivering services and became instead a liability to be minimised.

As a quick illustration of the differences between how businesses in the UK and Germany approach change this chart from the recent Economist Intelligence Unit research carried out for Towers Watson takes some beating. To UK eyes, an insane proportion (45%) of German businesses are proposing to make physical changes to their workplaces by 2020 to accommodate a greying workforce. There is an even more dramatic contrast when the issue of flexible working hours is raised. Less than half of UK businesses intend to offer more flexible working hours by 2020, compared to over three quarters of German businesses.

As a quick illustration of the differences between how businesses in the UK and Germany approach change this chart from the recent Economist Intelligence Unit research carried out for Towers Watson takes some beating. To UK eyes, an insane proportion (45%) of German businesses are proposing to make physical changes to their workplaces by 2020 to accommodate a greying workforce. There is an even more dramatic contrast when the issue of flexible working hours is raised. Less than half of UK businesses intend to offer more flexible working hours by 2020, compared to over three quarters of German businesses.

Neither are we interested in training our older workers apparently. Only 28% of UK businesses intend to ensure that the skills of their older employees remain up to date, compared to 48% of German businesses.

So where are UK businesses preparing to manage change then? Giving employees more choice over their benefits is cited by 60% of UK businesses, compared to 45% in Germany and the European average of 48%.

But is this the positive step it is presented as? It seems unlikely to me that these UK businesses that don’t want to invest in older workers’ working environments or give them flexibility over hours or location or train them is interested in providing any choice over benefits that doesn’t also cut their costs. There are going to be some battles ahead over exactly how the pensions changes in the Budget are to be implemented. Judging from this survey, they are going to be hard fought.

One of the pensions announcements in the Budget last week which got less coverage amongst the talk about freedom and the death of the annuity was the one about the minimum age at which pension benefits will be able to be taken in the future. In this respect the Government appears to feel that less freedom is preferable.

Historically the minimum age was 50 except for a list of exempted professions kept by HMRC (or the Inland Revenue as they then were) which included professional footballers. However in 2010 it was increased to 55. From 2028 it is proposed that it is going to be increased again, to 57, thereafter linked to increases in the State Pension Age (SPA).

PwC have projected that, assuming the policy of linking SPA to life expectancy continues into the future, we can expect a SPA of 77 by 2089 and 84 by 2134. If this all sounds a little futuristic, it does highlight a concern about the Government proposal of using SPA minus 10 (or even SPA minus 5 which is also being consulted upon) as a national minimum pension age.

The Office of National Statistics (ONS) have produced an interesting split of both life expectancy at birth (LE) and healthy life expectancy at birth (HLE) by deciles of deprivation. Graphing these with the steadily increasing SPAs shown in black and the minimum pension ages in red we can see that the bottom male and female 10% by deprivation already have a healthy life expectancy below the current minimum pension age, with a further 10% being caught by the increase to 57.

Admittedly we might hope for an increase in both life expectancy and healthy life expectancy at all levels by 2028, but the differentials between the poorest and the richest in this respect have been widening for some time. Certainly if the SPA minus 5 idea is adopted, giving a minimum pension age of 62 by 2028, it is difficult to see the bottom deciles reaching that age in good health. And what about a minimum pension age of 67 by 2089 (72 if SPA minus 5)? Do we think that we have policies in place to increase the healthy life expectancy of the bottom decile by the 15 years (or 20 years if SPA minus 5) that would be required to allow them to retire in good health, even assuming they felt able to do so financially?

As I have mentioned before, I think the Government needs to consider ill health early retirement to a greater extent in its policies towards state pension benefits, but this may be particularly urgent with respect to minimum retirement ages. The main problem as I see it would be the assessment of ill health, bearing in mind the current ATOS fiasco.

One alternative approach might be to try and maintain the minimum pension age as a proportion of SPA rather than a fixed number of years earlier. So, for instance, the current proportion (55/65 or 85%) would give a minimum pension age when SPA reached 77 of around 65.5 rather than the 67 proposed.

Leaving the proposals as they stand, however, is likely to lead to an increasingly ill elderly workforce engaged in the lowest paying and most physically demanding occupations. Not free, and without choices. That doesn’t sound like an election winner to me.

Source: Wikimedia Commons. A shell of the sea snail species Cymbiola vespertilio, the bat volute.

Photo taken by User:Haplochromis

How long am I going to live is, of course, an impossible question to answer precisely in most cases. However estimates about how long people with certain characteristics in common (like age, sex, postcodes and smoking habits for instance) are going to live are used for a wide range of purposes from future population estimates to annuity pricing to pension scheme funding.

Central to making any kind of estimate is working out how you think rates of mortality are going to change in the future. Based on the historical evidence over the last 100 years or more, all the models people use to make projections of future mortality rates in the UK involve them improving, but the consensus tends to end there.

There are several ways in which these projections can go wrong:

- Process or idiosyncratic risk, ie the risk of random fluctuations in mortality experience. The fewer people you have in your pension scheme, the more likely this is to be a big issue.

- Level or mis-estimation risk, ie you start from the wrong current position.

- Trend risk, ie risk of underestimating how much longevity will increase in the future.

Some also include another one:

- Catastrophe risk, ie the occurrence of an unknowable event with large consequences.

But what do these projections look like? Well, the most popular family of projections of future mortality improvements are generated by the CMI Projection Models, a new one of which comes out every year. Giving the rates of mortality improvements for each age in each year a colour produces something called a “heat map”. The colours get progressively “hotter”, moving from yellow to orange to red and then black as the rates of improvement increase, and “cooler” from yellow to green to blue and then purple, as the rates of improvement decrease and ultimately turn negative (ie worsening mortality). One version of this is shown below:

![100%S1PMA CMI_2012_M[2.00%]](http://momentumpublishing.co.uk/weknow0.co.uk/wp/wp-content/uploads/2014/03/CMI-heat-map.png)

100%S1PMA CMI_2012_M[2.00%]

Which as you can see is a considerable improvement on this (“cohort” adjustments of this type were used by most pensions actuaries only five years ago):

Source: CMI working paper 39: Actual and projected annual rates of mortality improvement for males: 1991-2005 – estimated actual rates for population of England & Wales; 2006 onwards – projected rates using ‘Medium Cohort_1.0% minimum’

However, in my view there is scope to go further.

One criticism which has been made by actuaries when using the core version of the CMI Projection Model is that the initial rates of improvements do not necessarily start to converge to the long term rate of improvement straight away, often diverging initially before starting a convergent path: these are displayed as little islands in the CMI heat map above.

Another potential criticism is that there are obviously many ways of creating a smooth transition to long term rates, but until now within the CMI model this required selecting the advanced features of the model. This allows much more flexibility over choice of:

- Base rates of mortality

- Initial rates of mortality improvement

- Long term rates of improvement that differ by age and year of birth

- Convergence, again by age and year of birth

However, selection of the advanced features brings its own problems in that it requires a further set of assumptions to be made for which, certainly within the framework of advising a trustee board of a pension scheme and particularly for small schemes with less data, it might be difficult to identify a convincing rationale. There also remains the problem that, even if a large set of additional assumptions can be agreed, it is often difficult to relate these to views held about what will impact future longevity improvements.

This begs the question of how you do go about introducing alternative projections. I think one answer to this may lie in a series of questions posed by Peter S Stevens in his book Patterns in Nature:

Why does nature appear to use only a few fundamental forms in so many different contexts? Why does the branching of trees resemble that of arteries and rivers? Why do crystal grains look like soap bubbles and the plates of a tortoise shell? Why do some fronds and fern tips look like spiral galaxies and hurricanes? Why do meandering rivers and meandering snakes look like the loop patterns in cables? Why do cracks in mud and markings on a giraffe arrange themselves like films in a froth of bubbles?

Patterns turn up again and again in seemingly unrelated areas in the natural world because, as D’Arcy Thompson pointed out long ago, those patterns are as much to do with the physics and chemistry of the world with which organisms are interacting as they are with their biology. It therefore seems reasonable to look at the mathematics underlying patterns which already exist in nature when considering what patterns might develop in future in, for instance, human mortality improvements.

I have chosen the mathematics underlying sea shell patterns, as explored by Hans Meinhardt and others.

By focusing on a graphical approach to setting future mortality improvement projections via heat maps, I believe that the particular features of any specific projection can be more readily linked to views about the impact of specific factors on longevity improvements. The method set out in a very short paper (The misbehaviour of mortality) I have just produced can be used for instance to turn this:

100%S1PMA CMI_2012_M[2.00%]

![100%S1PMA SSA_2012_M[220,0.4,23,1.5]](http://momentumpublishing.co.uk/weknow0.co.uk/wp/wp-content/uploads/2014/03/Sea-shell-heat-map.jpg)

100%S1PMA SSA_2012_M[220,0.4,23,1.5]

We can compare shapes of mortality improvements projected for eg a man aged 63 this year like this:

As you can see a wide variety of shapes can be achieved using this method. It allows features of a given projection to be more easily related to views held about social change, medical advances, etc and their impact on longevity improvements in the short, medium and long term. In particular, it allows future projections to be discussed in more detail, but in a non-technical way. This differs from the current most common approach, which tends to focus solely on a long term rate.

I think this approach holds promise for generating patterns of future mortality projections. The advantages are:

- It avoids some of the problems associated with the CMI core projection model (eg “islands”).

- It also avoids the considerable number of additional assumptions which would need to be agreed before the advanced version of the CMI model could be applied. Instead there are only four additional assumptions, each of which has an easily communicated interpretation for a lay audience.

- It has an aesthetic appeal, building on a considerable body of work into patterns found elsewhere in nature, which have not, as far as I am aware, been exploited in any other area of actuarial science to date.

- It allows particular features of a given projection to be more easily related to views held about social change, medical advances etc and their impact on longevity improvements in the short, medium and long term.

There is a potential disadvantage in that the applicability of sea shell patterns to mortality improvements may well be questioned by some. However, mathematics has a long tradition of establishing links between areas where none seemed to exist previously. Perhaps this will be another one?

In all the talk about annuities and the poor value they currently offer, nearly all of it has been based on standard annuity rates, ie where there is nothing sufficiently medically wrong with you to affect your life expectancy. However this is almost certainly not the rate you should be looking at.

In all the talk about annuities and the poor value they currently offer, nearly all of it has been based on standard annuity rates, ie where there is nothing sufficiently medically wrong with you to affect your life expectancy. However this is almost certainly not the rate you should be looking at.

Go to any of the annuity provider or broker websites, sometimes buried away a little, and you will find a link explaining what they can offer in the way of “enhanced” or “impaired lives” annuities. Legal & General’s web page on this looks like the kind of warning notice you find on the wall of your doctor’s surgery waiting room, with headings like Smoking, Type 2 Diabetes and High Blood Pressure. But in the upside-down world of buying annuities these become good things to do or have.

Just Retirement give some handy illustrations of what various conditions could mean for your income: up 20% for minor conditions like obesity and hypertension, up 30% for “moderate” ones like being a heart attack survivor with a bypass and 40% for serious medical conditions like stage 2 bowel cancer one year in. However, you don’t need to get anywhere near the frankly frightening conditions in the moderate and serious boxes to make a big difference to the income you can receive. annuitydiscount.co.uk provide a very long list of medications (covering every letter in the alphabet except J and Y) which could lead to an impaired life annuity if disclosed to the annuity provider.

As the BBC article from 2012 posted by the Better Retirement Group on enhanced annuities says: “At its simplest an annuity is a bet with the insurance company about how long you will live.”

So on that basis, it makes sense to stack the odds in your favour as much as you can. Which makes the 2007 article in the New England Journal of Medicine entitled, rather dully, Incidental Findings on Brain MRI in the General Population, such an interesting read.

They studied 2,000 people (mean age 63.3 years, range 45.7 to 96.7) from the population-based Rotterdam Study in whom high-resolution, structural brain MRI scans had been carried out. Asymptomatic brain infarcts (more commonly known as strokes) were present in 145 people (7.2%). Among other findings, aneurysms (1.8%) were the most frequent. Benign brain tumors also turned up reasonably often (1.6%). The most extreme case was someone with a large, chronic subdural haematoma, who was subsequently found to have had a minor head trauma 4 weeks before the MRI scan. Some of the scans are shown below.

But the really amazing thing is this: only 2 of the 2,000 people scanned (the subdural haemotoma mentioned above and another who had a 12 mm aneurysm of the medial cerebral artery) had any idea that there was anything wrong with them!

But the really amazing thing is this: only 2 of the 2,000 people scanned (the subdural haemotoma mentioned above and another who had a 12 mm aneurysm of the medial cerebral artery) had any idea that there was anything wrong with them!

Another huge area of undiagnosed disease (and on the annuity.co.uk list for enhanced annuities) is prostate cancer. According to a systematic review of prostate cancer biopsy schemes by the University of York in 2005, where they quoted from the NHS Centre for Reviews and Dissemination publication on screening for prostate cancer, Effectiveness Matters:

Post mortem studies show that 30% of men over 50, who had no symptoms of prostate cancer whilst alive, had histological evidence of prostate cancer at the time of death. This percentage rises to 60-70% in men over 80 years of age. In other words, most men with prostate cancer die with, rather than from, the disease.

The main reason these studies have been carried out is to determine whether screening for prostate cancer, which kills 3.8% of men with the disease, has saved many lives. The Prostate Specific Antigen (PSA) test that is commonly used to detect prostate cancer in the absence of symptoms is not only prone to false positives and negatives (ie telling you you have it when you don’t and don’t have it when you do – something all screening suffers from to some extent), but can lead to you being offered treatment which may well be worse than the disease. This is discussed further in the excellent The Norm Chronicles, by Michael Blastland and David Spiegelhalter, which questions whether, overall, screening is particularly effective in saving lives.

Effective in preventing death? Perhaps not. But effective in increasing retirement income? Almost certainly.

The latest Association of British Insurers (ABI) facts and figures on the UK annuity market suggest that enhanced annuities have grown in popularity, to 24% in 2012 from 2% in 2003. There is scope to make further large increases in these figures if more people can be persuaded to have themselves screened for some of the most common undiagnosed conditions before they retire.

So don’t necessarily accept a standard annuity rate. And consider getting yourself tested first.