This is a quote attributed to Lenin (courtsey of Branko Milanovic’s X account, where a gentle exchange about whether it was genuine ensued), which seems perfect for the moment we are in.

It was back in 1998 that George Monbiot first pointed out that no sector was as wedded to PFI deals as health. The famous example in Captive State of the Walsgrave hospital in Coventry, knocked down and replaced by a smaller hospital at much greater cost, was just one of many. It didn’t occur to me at the time, but the wider lesson from these early examples, borne out by everything we have seen since, is that privatisation, in whatever form (and, after all, what is PFI but the privatisation of a funding source), always solves a smaller problem than the one you have. The history of privatisation in the NHS has been a series of smaller easier problems dealt with in some cases very efficiently by the private sector (although the efficiency only ever seems to increase the profits of the private companies concerned rather than reduce their price). As it has been in transport (with rail franchises yo-yoing in and out of state control whenever the ask becomes too complex for the train operators taking them on), and utilities, mail services, etc etc.

And the size of the problems that the private sector can take on would appear to be getting smaller.

Take insurance. Ann Pettifor highlights this week what Petra Hielkema, chair of the European Insurance and Occupational Pensions Authority, has to say about the future of the sector in the FT. Apparently he told them that governments and banks will struggle to cope with the soaring costs of natural catastrophes such as floods and wildfires. More households will be unable to insure their homes and the mounting losses from natural disasters could destabilise banks. Two things he said were particularly striking:

“I think it is the biggest risk facing society, frankly” and “Member states — they can’t cope with this.”

There is now talk of an “insurance death spiral“, where insurance premiums shoot up, those least likely to claim drop out, and insurers are left with exclusively “sub-prime” risks on their books (should sound familiar to anyone who has read about the causes of the 2008 crash). In the US, there are obviously problems in the Californian insurance industry which look like causing some degree of financial contagion, but also a particular focus on the health insurance industry as a result of the way Obamacare was implemented.

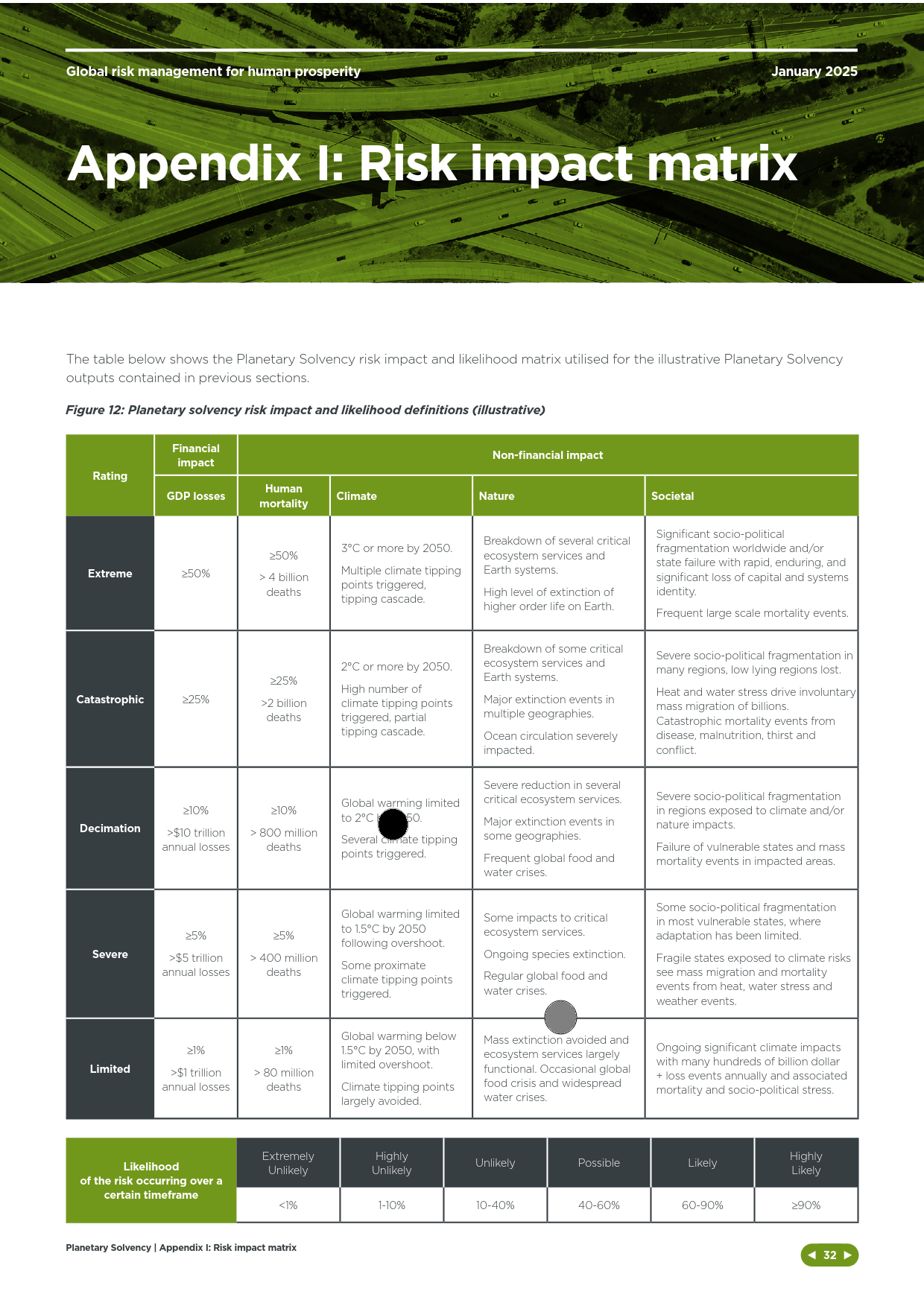

This contrast between public and private ownership of problems struck me while I was reading the excellent report from the Institute and Faculty of Actuaries and the University of Exeter on climate change: Planetary Solvency. By taking the approach that an insurance company would take in determining its risk appetite and then seeing if its risk exposure matched up to it, it occurred to me that the reason this had never been done before for global climate change was that any insurer would have left such a market years ago on the basis of a brief initial analysis of the problem. Something that a private insurer can always do with any problem.

What if, instead of the NHS being threatened by covert privatisation, the threat is that even the smaller problems private health is currently solving within the system get handed back to the NHS? Because that is the difference. During the pandemic, the threat was that the NHS might not be able to cope with the surge in very ill people and that many would die without care as a result. The reason large parts of NHS operations were repurposed and we were all urged to “flatten the curve” was because, ultimately, there is noone the NHS can hand the responsibility back to and their resources are measured in hours of the right people available to work for them rather than pounds spent and so have a hard physical limit. Although there were significant failures as the Covid Inquiry is currently exploring, the NHS as a whole did not fall over.

However, neither did the US system, because an insurer merely withdraws from a market which might cause it to. It has no responsibility to the system as a whole.

As one MIT researcher responded to being asked about the lessons for the US system of the pandemic:

“The pandemic has revealed the American health care system to be a non-system.”

So it seems to me that arguments about privatisation and nationalisation are a bit beside the point. We have big problems, getting bigger every day, which absolutely have to be solved and limited physical resources with which to do so. Unfortunately His Majesty’s Opposition are still trying to disentangle themselves from the wreckage of Tufton Street’s “thought leadership”, risking a Trumpian climate change denying, health service privatising Reform Party replacing them, and His Majesty’s Government appear to have no idea what they are doing.

So reality does feel pretty radical at the moment. We need to be equally radical in our response to it.