In his excellent new book, Breakneck, Dan Wang tells the story of the high-speed rail links which started to be constructed in 2008 between San Francisco and Los Angeles and between Beijing and Shanghai respectively. Both routes would be around 800 miles long when finished. The Beijing-Shanghai line opened in 2011 at a cost of $36 billion. To date, California has built only a small stretch of their line, as yet nowhere near either Los Angeles or San Francisco, and the latest estimate of the completed bill is $128 billion. Wang uses this, amongst other examples to draw a distinction between the engineering state of China “building big at breakneck speed” and the lawyerly society of the United States “blocking everything it can, good and bad”.

Europe doesn’t get much of a mention, other than to be described as a “mausoleum”, which sounds rather JD Vance and there is quite a lot about this book that I disagree with strongly, which I will return to. However there is also much to agree with in this book, and none more so than when Wang talks about process knowledge.

Wang tells another story, of Ise Jingu in Japan. Every 20 years exact copies of Naiku, Geku, and 14 other shrines here are built on vacant adjacent sites, after which the old shrines are demolished. Altogether 65 buildings, bridges, fences, and other structures are rebuilt this way. They were first built in 690. In 2033, they will be rebuilt for the 63rd time. The structures are built each time with the original 7th century techniques which involve no nails, just dowels and wood joints. Staff have a 200 year tree planting plan to ensure enough cypress trees are planted to make the surrounding forest self-sufficient. The 20 year intervals between rebuilding are the length of the generations, the older passing on the techniques to the younger.

This, rather like the oral tradition of folk stories and songs, which were passed on by each generation as contemporary narratives until they were all written down and fixed in time so that they quickly appeared old-fashioned thereafter, is an extreme example of process knowledge. What is being preserved is not the Trigger’s Broom of temples at Ise Jingu, but the practical knowledge of how to rebuild them as they were originally built.

Process knowledge is the know-how of your experienced workforce that cannot easily be written down. It can develop where such a workforce work closely with researchers and engineers to create feedback loops which can also accelerate innovation. Wang contrasts Shenzhen in China where such a community exists, with Silicon Valley where it doesn’t, forcing the United States to have such technological wonders as the iPhone manufactured in China.

What happens when you don’t have process knowledge? Well one example would be our nuclear industry, where lack of experience of pressurised water reactors has slowed down the development of new power stations and required us to rely considerably on French expertise. There are many other technical skill shortages.

China has recognised the supreme importance of process knowledge as compared to the American concern with intellectual property (IP). IP can of course be bought and sold as a commodity and owned as capital, whereas process knowledge tends to rest within a skilled workforce.

This may then be the path to resilience for the skilled workers of the future in the face of the AI-ification of their professions. Companies are being sold AI systems for many things at the moment, some of which will clearly not work with few enough errors, or without so much “human validation” (a lovely phrase a good friend of mine actively involved in integrating AI systems into his manufacturing processes used recently) that they are not deemed practical. For early career workers entering these fields the demonstration of appropriate process knowledge, or the ability to develop it very quickly, may be the key to surviving the AI roller coaster they face over the next few years. Actionable skills and knowledge which allow them to manage such systems rather than being managed by them. To be a centaur rather than a reverse-centaur.

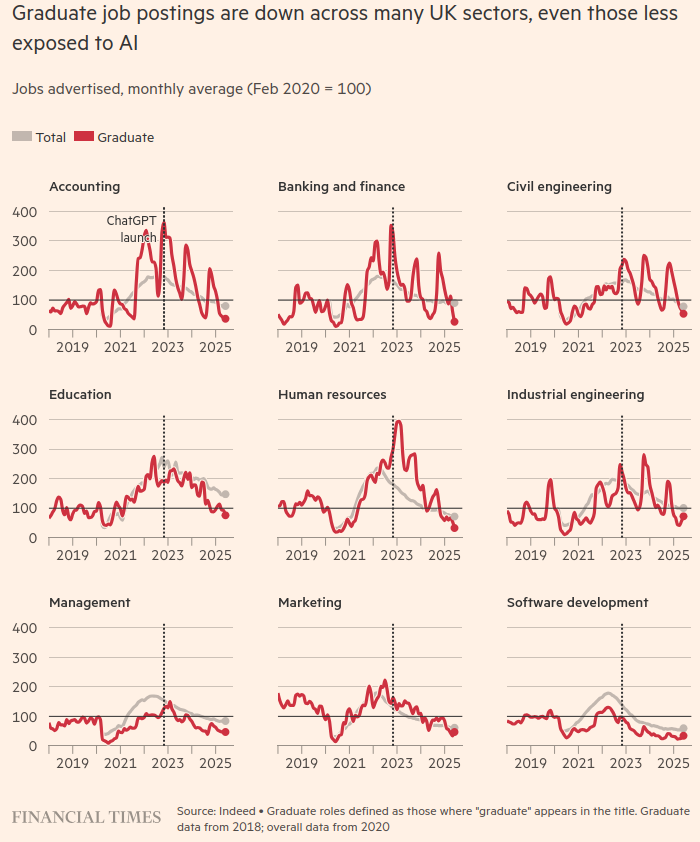

Not only will such skills make you less likely to lose your job to an AI system, they will also increase your value on the employment market: the harder these skills and knowledge are to acquire, the more valuable they are likely to be. But whereas in the past, in a more static market, merely passing your exams and learning coding might have been enough for an actuarial student for instance, the dynamic situation which sees everything that can be written down disappearing into prompts in some AI system will make such roles unprotected.

Instead it will be the knowledge about how people are likely to respond to what you say in a meeting or write in an email or report, and the skill to strategise around those things, knowing what to do when the rules run out, when situations are genuinely novel, ie putting yourself in someone else’s shoes and being prepared to make judgements. It will be the knowledge about what matters in a body of data, putting the pieces together in meaningful ways, and the skills to make that obvious to your audience. It will be the knowledge about what makes everyone in your team tick and the skills to use that knowledge to motivate them to do their best work. It will ultimately be about maintaining independent thought: the knowledge of why you are where you are and the skill to recognise what you can do for the people around you.

These have not always been seen as entry level skills and knowledge for graduates, but they are increasingly going to need to be as the requirement grows to plug you in further up an organisation if at all as that organisation pursues its diamond strategy or something similar. And alongside all this you will need a continuing professional self-development programme on steroids going on to fully understand the systems you are working with as quickly as possible and then understand them all over again when they get updated, demanding evidence and transparency and maintaining appropriate uncertainty when certainty would be more comfortable for the people around you, so that you can manage these systems into the areas where they can actually add value and out of the areas where they can cause devastation. It will be more challenging than transmitting the knowledge to build a temple out of hay and wood 20 years into the future, and will be continuous. Think of it as the Trigger’s Broom Process of Career Management if you like.

These will be essential roles for our economic future: to save these organisations from both themselves and their very expensive systems. It will be both enthralling and rewarding for those up to the challenge.