My evidence to the House of Lords Economic Affairs committee on the sustainability of the UK’s national debt is now available on the parliamentary website.

I was rather surprised to see that only 37 people submitted written evidence. My evidence was as follows (with the hyperlinks which got removed restored and the addition of the graph of the history of public sector net debt):

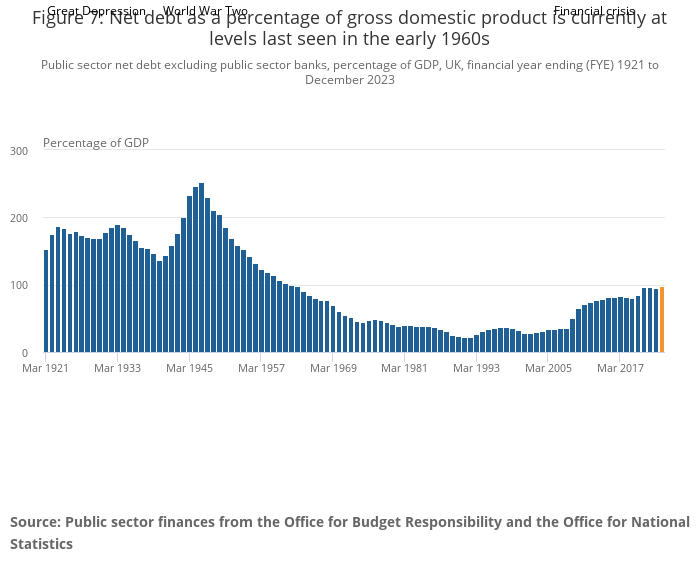

The “incredible” £2.6 trillion mentioned by Lord Bridges of Headley in the call for evidence suggests that you are using the public sector net debt excluding public sector banks figure, which is £2.671 trillion or 97.5% of GDP as at November 2023 according to the Public Sector Finances bulletin on the ONS website. You could more reasonably use the public sector net debt excluding public sector banks and the Bank of England figure, which recognises that otherwise you are notionally including a debt attributed to an organisation which has no debt, which therefore reduces this debt to £2.419 trillion or 88.3% of GDP. Or even better, you could also deduct the Bank of England Asset Purchase facility, which was used for QE and is held by a subsidiary company of the Bank of England controlled by the Treasury and therefore also not a debt in the commonly accepted sense of the word. This stands at £0.597 trillion in Q2 2023 according to the latest quarterly report from the DMO and would further reduce the debt to hopefully a slightly less incredible £1.822 trillion or 66.5% of GDP.

Even if you want to stick with your original number, despite a large part of it not being owed to anyone with any interest in being paid back, the public sector net debt according to the ONS following a global pandemic and Brexit as a percentage of GDP is lower in the UK than at any time between 1916-17 and 1960-61.

Our latest general government debt available on the IMF Datamapper, which is from 2022, of 101.4% of GDP also compares favourably with the United States (121.4%), Japan (261.3%) and France (111.7%), with only Germany (66.5%), China (77.1%) and India (83.1%) of our major partners or rivals with lower debt.

With this perspective in mind, my responses to a selection of the questions set out for the call for evidence would be as follows:

What is meant by a “sustainable” national debt? Does the metric of debt as a percentage of GDP adequately capture sustainability?

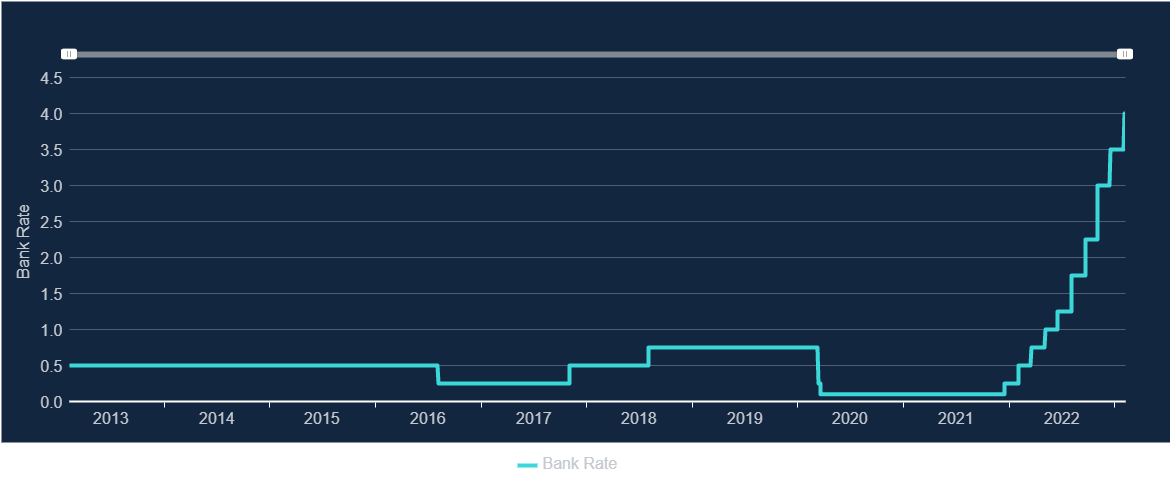

I think this means affordable, both currently and in the future. The only reason our current level of debt (which, as I have shown, is not particularly high either by international or historical comparison) is felt by some to be unaffordable is the sharp increases in interest rates by the Bank of England over the last two years. Central government debt interest, net of the Asset Purchase Facility was £112.1 billion in 2022-23, compared to £60.9 billion in 2021-22 and £26.7 billion in 2020-21.

According to the World Economic Outlook from the IMF in April 2023:

Overall, the analysis suggests that once the current inflationary episode has passed, interest rates are likely to revert toward pre-pandemic levels in advanced economies.

This is therefore a temporary problem and does not suggest that the level of debt is unsustainable at all. Interest rates should be brought down as quickly as possible, and the rate of interest on the Asset Purchase Facility should be reduced immediately to very low levels, as is already the case in many other countries including the Eurozone and Japan (the case for this was made in June 2022 in the New Economics Foundations’ report Between A Rock And A Hard Place).

The Government’s target is for public sector net debt (excluding the Bank of England) to be falling, as a percentage of GDP, by the fifth year of the OBR’s forecast. How meaningful is this target; and how does it inform an evaluation of the sustainability of our national debt?

I think this target is essentially meaningless given the high likelihood of a change of Government within the next year. In my opinion Government spending needs to be set according to need rather than by setting an arbitrary target for the level of debt as a percentage of GDP.

What are the market risks created by high levels of public debt; and what factors will influence the market’s appetite for this debt?

As the DMO Annual review for 2022-23 states: “The average cover ratio at gilt auctions in 2022-23 was 2.39, in line with 2.41, in 2021-22”, ie there are consistently nearly two and a half times as many bids for gilts as gilts being offered for sale. This indicates a continued strong demand for gilts.

What levels of productivity and growth are required to ensure our national debt is sustainable?

Our national debt is already sustainable.

If we are to ensure our national debt is sustainable, what might this mean for fiscal policy?

Our national debt is already sustainable.

Should the definition of the national debt differentiate between debt incurred for investments (which generate revenue for the Government), and other areas of spending?

Yes. One example would be where nationalised entities such as Network Rail are included as a liability but the corresponding revenue-producing asset is not set against this when included in the national debt figures.

It is striking to me what questions you are not asking, eg:

If we are to ensure our national debt is sustainable, what might this mean for monetary policy?

This seems to me to be a much more relevant question, as it would appear that the sole reason the unsustainability of the national debt has become an issue is due to the monetary policy of the Bank of England. Japan has negative interest rates, the Eurozone’s rate is 0.75% below ours. The high level of interest rates in the UK is having a negative impact on economic growth, investment and unemployment, as well as sharply increasing the cost of the national debt. The independence of the Bank of England and the nature of the targets it is set would both be more interesting subjects for a call for evidence than the sustainability of the national debt.